How Alnylam’s Swing to Quarterly Profitability Could Reshape the Outlook for Alnylam Pharmaceuticals (ALNY) Investors

Alnylam Pharmaceuticals, Inc ALNY | 0.00 |

- In the past quarter, Alnylam Pharmaceuticals reported first-quarter 2026 results showing revenue of US$1,167.18 million versus US$594.19 million a year earlier, with net income of US$205.99 million replacing a prior net loss and basic earnings per share rising to US$1.55 from a loss per share of US$0.14.

- This sharp move into profitability, alongside improved earnings per share metrics, signals a meaningful shift in Alnylam’s operating profile that could influence how investors assess its RNAi-focused business.

- Next, we’ll examine how Alnylam’s swing to quarterly profitability may affect its existing investment narrative around growth, risk, and RNAi leadership.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you essentially need to believe that RNAi therapies, led by the TTR franchise, can support sustained growth while the company keeps profitability intact. The sharp swing into profit in Q1 2026 helps near term confidence, but it does not remove key risks around pricing pressure, royalty drag on AMVUTTRA, or the need for continued pipeline success, which still look like the main near term swing factors for the story.

Among recent updates, the Q1 2026 earnings release is most relevant here, as it puts hard numbers behind the prior narrative of revenue acceleration and operating leverage. The move to US$205.99 million in quarterly net income and US$1,167.18 million in revenue frames how investors might weigh earlier concerns about margin compression and spending, and whether the current profitability level feels sustainable against AMVUTTRA pricing and royalty headwinds.

Yet beneath this profitability milestone, investors should still be aware of rising royalty obligations and payer driven pricing pressure that could...

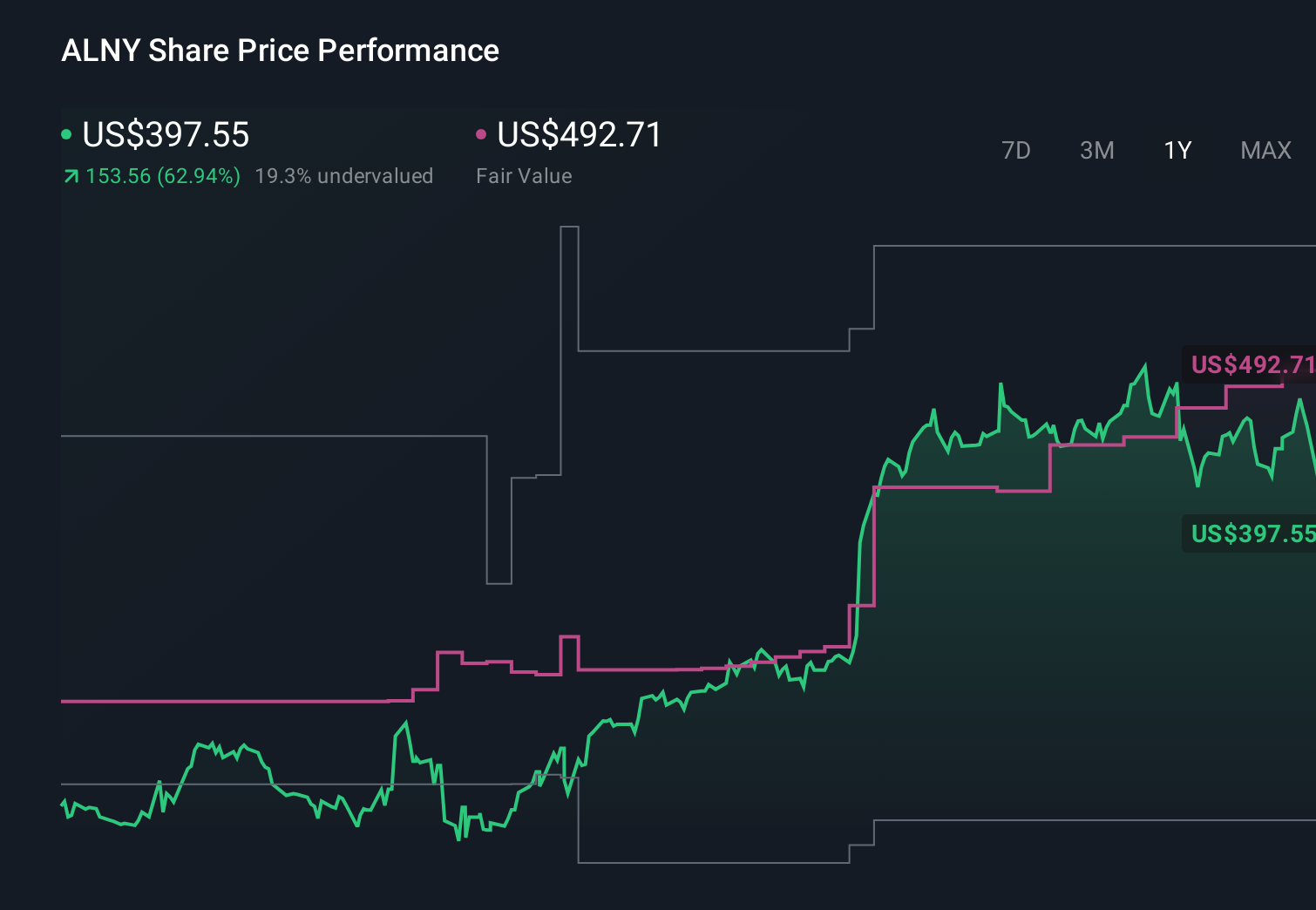

Alnylam Pharmaceuticals' narrative projects $7.0 billion revenue and $1.9 billion earnings by 2028. This requires 41.8% yearly revenue growth and roughly a $2.2 billion earnings increase from -$319.1 million today.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 67% upside to its current price.

Exploring Other Perspectives

Before this profit surprise, the most bullish analysts were already assuming revenue could compound about 45 percent a year to US$11.5 billion, but they also flagged the risk that intense pricing pressure on AMVUTTRA could erode the very margins those targets depend on. That is a much more optimistic narrative than consensus, and Q1’s results may either reinforce or challenge those high expectations, so it is worth weighing how your own view lines up with these very different assumptions.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.