How Berenberg’s Coverage Initiation and Q1 Beat May Shape Vulcan Materials’ (VMC) Investment Case

Vulcan Materials Company VMC | 0.00 |

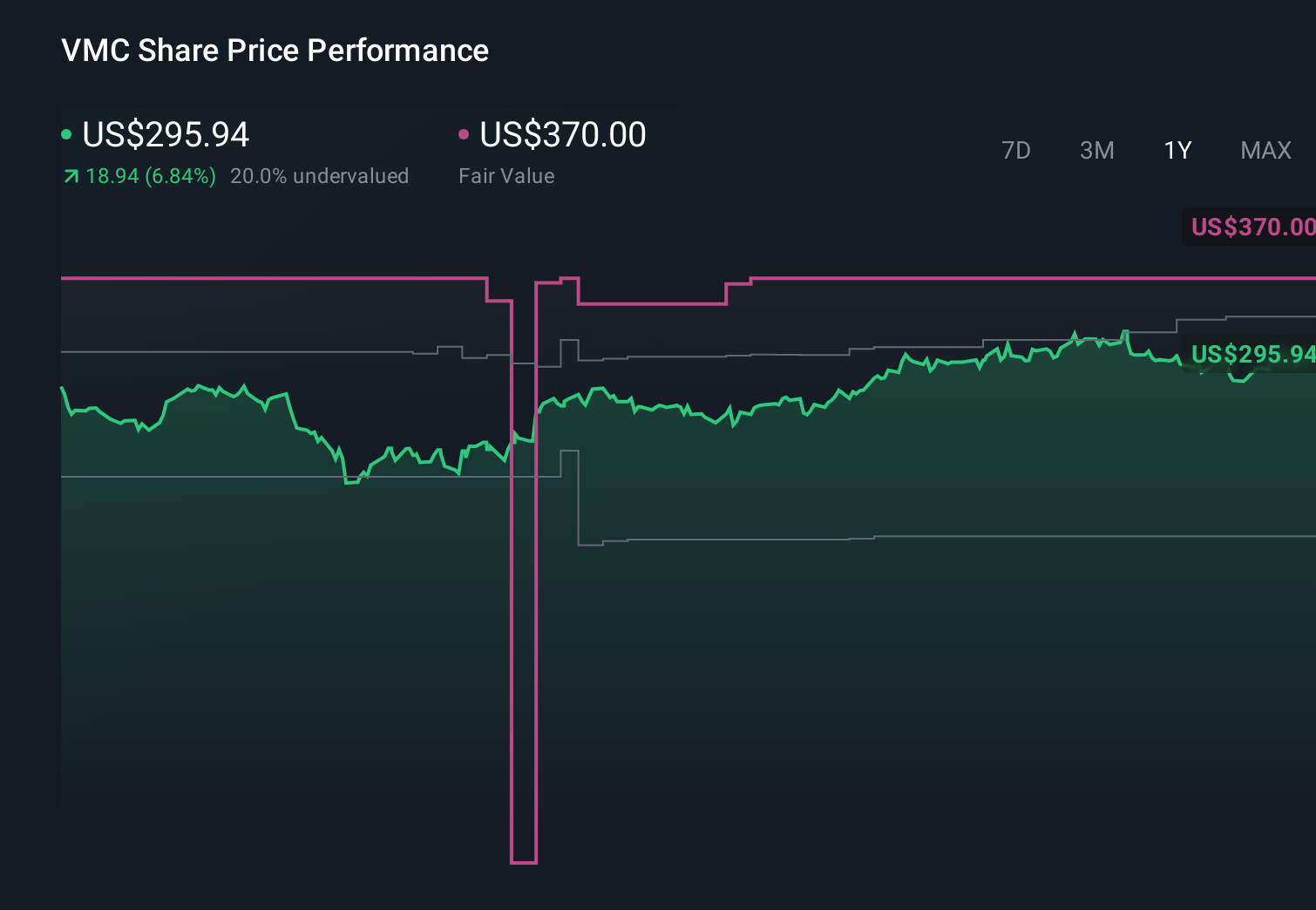

- Berenberg recently initiated coverage on Vulcan Materials with a Hold rating, following the company’s Q1 2026 results that exceeded earnings and revenue expectations and its declaration of a quarterly cash dividend payable in June 2026.

- This combination of positive analyst attention and stronger-than-expected operating performance highlights Vulcan’s position in a structurally supported US aggregates market, where construction demand is projected by Berenberg to grow steadily.

- We’ll now examine how Berenberg’s coverage initiation, emphasizing robust US aggregates fundamentals, may influence Vulcan Materials’ existing investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you generally have to believe in a long runway for US aggregates demand and the company’s ability to convert that into durable cash generation. Berenberg’s Hold initiation after better than expected Q1 2026 results supports the demand backdrop, but it does not materially change the near term picture: infrastructure funding momentum remains a key catalyst, while exposure to weather disrupted Southeast markets and permitting related CapEx delays stays a central risk.

The recent affirmation of the US$0.52 quarterly dividend, payable in June 2026, is the clearest tie to this news. It came alongside Q1 outperformance and suggests management’s confidence in ongoing cash flows even as they manage CapEx timing and weather related volatility. For investors focused on catalysts, that combination of dividend continuity and earnings strength will likely sit alongside IIJA driven project awards as they weigh the risk of regional disruptions and funding uncertainty.

Yet against this solid backdrop, the possibility of prolonged project delays and weather disruptions in Vulcan’s core Southeast markets is something investors should be aware of...

Vulcan Materials' narrative projects $9.6 billion revenue and $1.7 billion earnings by 2029. This requires 6.0% yearly revenue growth and roughly a $0.6 billion earnings increase from $1.1 billion today.

Uncover how Vulcan Materials' forecasts yield a $328.81 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling roughly US$10.0 billion of revenue and US$1.9 billion of earnings by 2029 before this update, so if you believe that kind of upside while also weighing the longer term threat from recycled aggregates and alternative materials, it highlights how differently you and other investors might view Vulcan’s prospects and why this latest news could still shift those expectations.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth as much as 28% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.