How Citigroup’s Profitability, AI, and Capital Plans At Investor Day Have Changed Its Investment Story (C)

Citigroup Inc. C | 0.00 |

- Citigroup is holding its first Investor Day in four years today, where senior leaders are expected to outline new profitability targets, AI deployment plans, and updates on risk-management remediation and capital returns.

- This rare investor forum offers a consolidated view of how management intends to balance technology investment, operational efficiency, and shareholder returns across the global franchise.

- We’ll now look at how the Investor Day focus on higher profitability targets and AI integration could reshape Citigroup’s investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Citigroup Investment Narrative Recap

To own Citigroup today, you need to believe its global scale, transaction banking strengths, and ongoing restructuring can translate into better profitability and capital returns. The key near term catalyst is management’s new profitability targets and AI plans from Investor Day, while the biggest current risk remains regulatory and transformation complexity. The latest leadership moves and financing activities do not materially change that balance, but they add context around execution.

Against this backdrop, Citi’s fresh round of senior appointments across growth regions and its active issuance and tendering of notes highlight how the bank is reshaping its international and funding footprint while fine tuning capital structure. These steps sit alongside the Investor Day focus on higher return targets and AI deployment, together forming an execution test for whether Citi can close the gap between its current returns and board level ambitions.

Yet behind the stronger targets and AI story, investors should also be aware of the risk that prolonged regulatory and transformation costs could still...

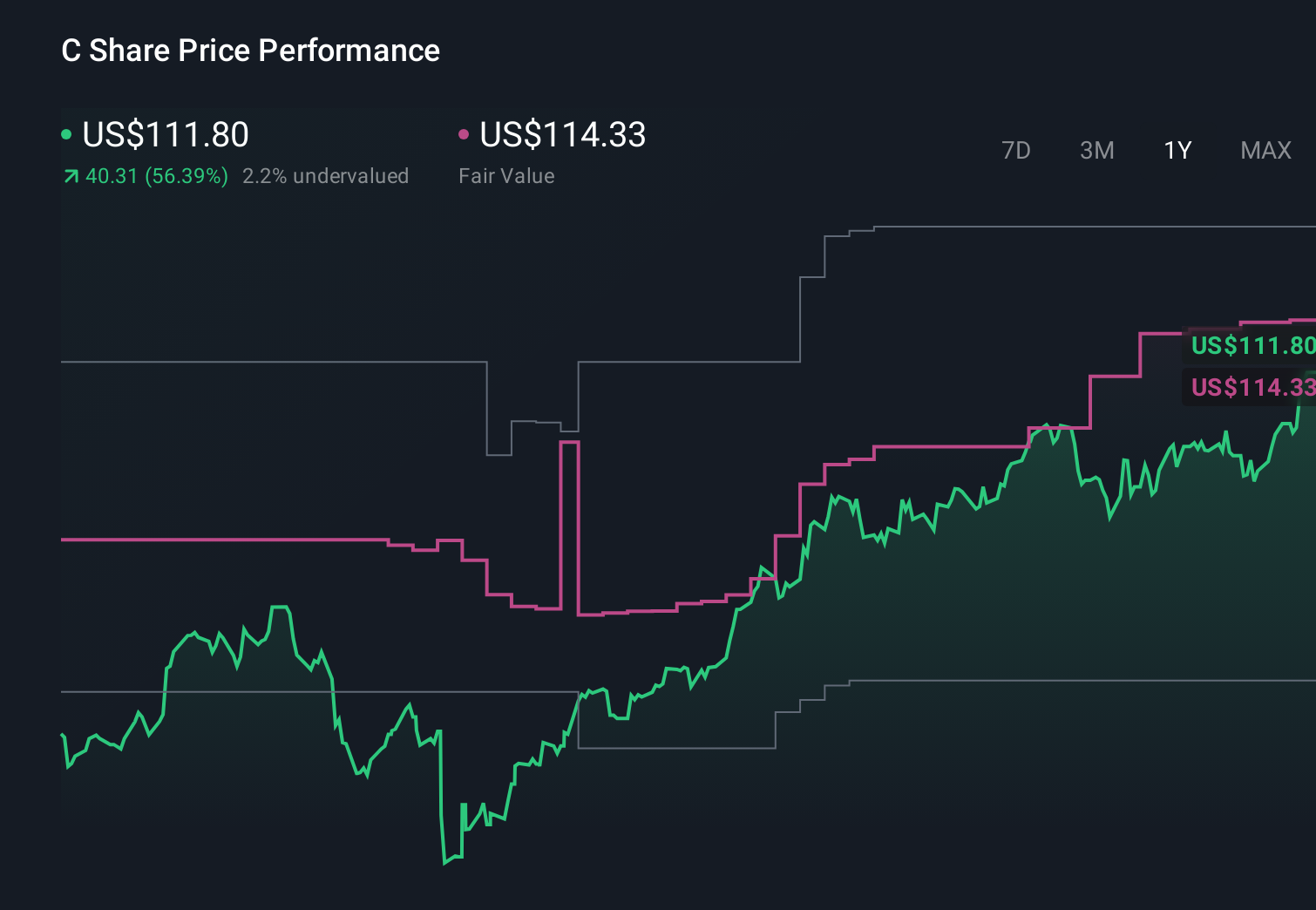

Citigroup's narrative projects $101.7 billion revenue and $21.2 billion earnings by 2029.

Uncover how Citigroup's forecasts yield a $142.50 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Citi could lift annual revenue to about US$91.3 billion and earnings to US$20.0 billion, yet today’s focus on AI driven efficiency and capital returns shows how differently you and other investors might weigh those upbeat assumptions against execution and macro risks, and why both the consensus and bullish narratives may evolve from here.

Explore 13 other fair value estimates on Citigroup - why the stock might be worth 12% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Citigroup research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.