How Crescent Energy’s ESOP Share Registration and Debt Moves Shape Its Capital Strategy Narrative (CRGY)

Crescent Energy CRGY | 0.00 |

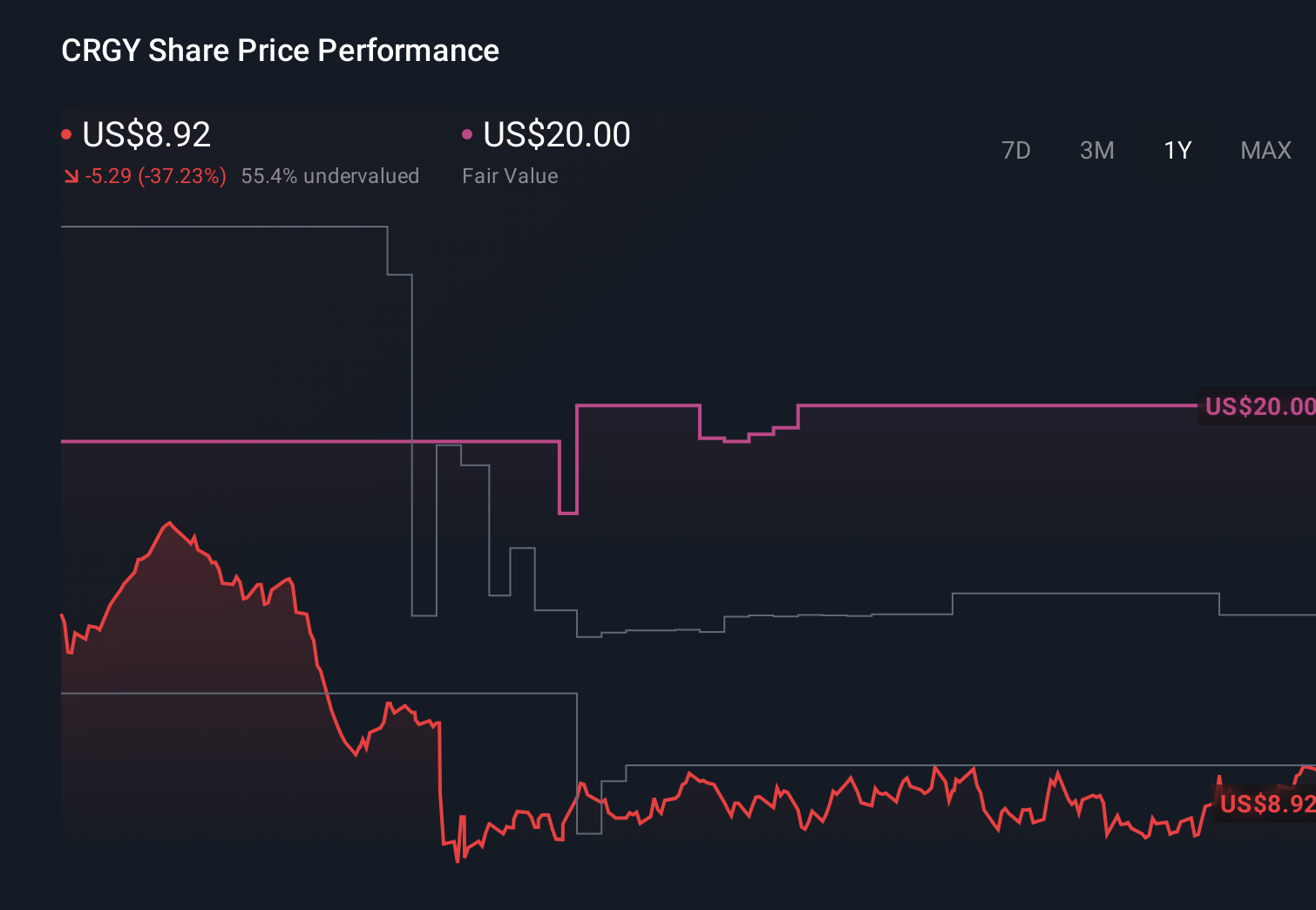

- Crescent Energy recently filed a US$12.12 million shelf registration for 1,035,228 shares of Class A common stock tied to an ESOP-related offering.

- This move, alongside efforts to lower funding costs and extend debt maturities, highlights management’s emphasis on balance sheet flexibility and employee ownership.

- We’ll now explore how Crescent Energy’s focus on balance sheet strengthening and capital flexibility could influence its broader investment narrative.

This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

Crescent Energy Investment Narrative Recap

To own Crescent Energy, you need to be comfortable with a acquisitive U.S. oil and gas producer that is prioritizing balance sheet strength, liquidity, and employee alignment. The new US$12.12 million ESOP related shelf registration is relatively small versus Crescent’s market value and does not materially change the near term focus on debt reduction as a key catalyst, or the ongoing risks tied to acquisition execution and capital intensity.

The recent upsized US$600 million convertible senior notes offering at a 2.75% rate is more directly connected to this story, since both actions speak to Crescent’s effort to secure flexible funding while it leans on free cash flow for deleveraging. That matters for how the company manages interest costs and refinancing risk, which sit alongside commodity volatility and acquisition outcomes as central moving pieces in the thesis.

Yet, behind Crescent’s push for balance sheet flexibility, there is still the question of what happens if acquisition driven growth collides with weaker commodity prices and constrained capital access for fossil fuel producers that investors should be aware of...

Crescent Energy's narrative projects $5.2 billion revenue and $672.6 million earnings by 2028.

Uncover how Crescent Energy's forecasts yield a $13.07 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already expecting Crescent to reach about US$5.3 billion in revenue and US$500 million in earnings, yet they still flagged high leverage and capital access as key worries, which may look quite different in light of the new ESOP shelf and debt moves.

Explore 5 other fair value estimates on Crescent Energy - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Crescent Energy research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crescent Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crescent Energy's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.