How Dividend Strength, Analyst Upgrades, and Technical Momentum At TFS Financial (TFSL) Have Changed Its Investment Story

TFS Financial Corporation TFSL | 14.30 | +0.49% |

- Recently, TFS Financial’s share price moved above its 200-day moving average, alongside the payment of a quarterly dividend and supportive analyst commentary, including upgrades and reiterated positive views on the stock.

- This combination of technical strength, income appeal via a high dividend yield, and improved analyst sentiment has sharpened investor focus on the bank’s consumer and community-oriented lending model.

- We’ll now examine how the healthier analyst sentiment around TFS Financial’s dividend profile shapes the company’s broader investment narrative.

Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

What Is TFS Financial's Investment Narrative?

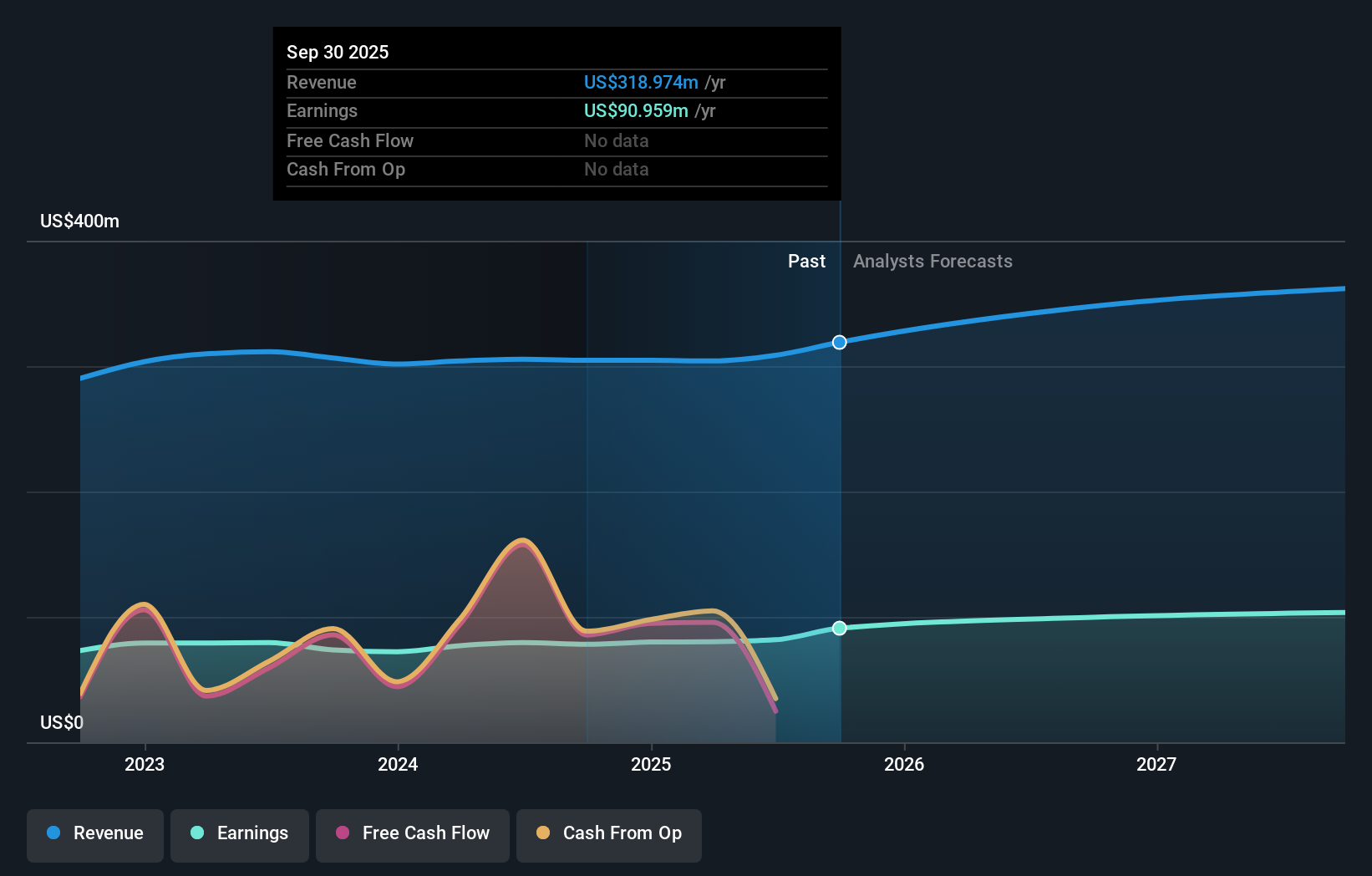

To own TFS Financial, you need to be comfortable backing a conservative, income-focused bank whose appeal rests heavily on its high dividend and community banking model, rather than fast growth. The recent move above the 200-day moving average, combined with an 8%-plus yield and friendlier analyst ratings, reinforces the stock’s income story and may support sentiment in the short term, but it does not remove the core tension: earnings growth is modest, returns on equity are low, the payout is not well covered, and the shares already trade on a rich earnings multiple. The steady dividend declarations and incremental buybacks underline management’s commitment to returning capital, yet they also heighten sensitivity to any pressure on profits, credit quality or funding costs. In that context, the latest positive news looks supportive, but not transformational for the key catalysts and risks.

However, one risk around the sustainability of that generous dividend profile deserves closer attention. TFS Financial's shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.Exploring Other Perspectives

Three Simply Wall St Community members place fair value for TFS Financial anywhere between about US$1.41 and US$13.59, highlighting widely different expectations. Set against the rich current valuation and dividend coverage concerns, this spread underlines why you may want to weigh several perspectives before deciding how the bank’s income story fits into your portfolio.

Explore 3 other fair value estimates on TFS Financial - why the stock might be worth less than half the current price!

Build Your Own TFS Financial Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TFS Financial research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free TFS Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TFS Financial's overall financial health at a glance.

Want Some Alternatives?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 18 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.