How Grow Funds’ Exit and Weaker Earnings Recast Harrow’s (HROW) Growth Narrative and Governance Choices

Harrow, Inc. HROW | 0.00 |

- Harrow, Inc. recently held its 2026 Annual Meeting of Stockholders, where all director nominees and executive compensation were approved and Deloitte & Touche LLP was ratified as auditor.

- A separate update from Grow Funds drew attention to Harrow’s disappointing earnings and a slight reduction in hedge fund ownership, highlighting tension between prior growth expectations and actual performance.

- We’ll now examine how Grow Funds’ decision to exit its position and flag weaker earnings shapes Harrow’s existing investment narrative.

AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Harrow Investment Narrative Recap

To own Harrow, you have to believe its ophthalmic portfolio can grow enough to offset product concentration and pricing pressure risks, while management delivers on ambitious revenue guidance despite current losses. The recent shareholder meeting and board approvals do little to change that near term picture, whereas Grow Funds’ exit after weaker earnings spotlights the main short term risk: Harrow missing its own growth and margin targets.

The most relevant recent development here is Grow Funds’ decision to close its position after Harrow’s earnings miss, despite previously liking the company’s growth prospects. That reaction underscores how sensitive the story is to execution on launches like VERKAZIA and IHEEZO and to Harrow’s reaffirmed 2026 revenue guidance of US$350 million to US$365 million, which now sits under a brighter spotlight after a disappointing first quarter.

Yet behind the optimism around Harrow’s eye care portfolio, investors should be aware that heavy reliance on a few flagship products and any disconnect between guided and realized revenue growth could...

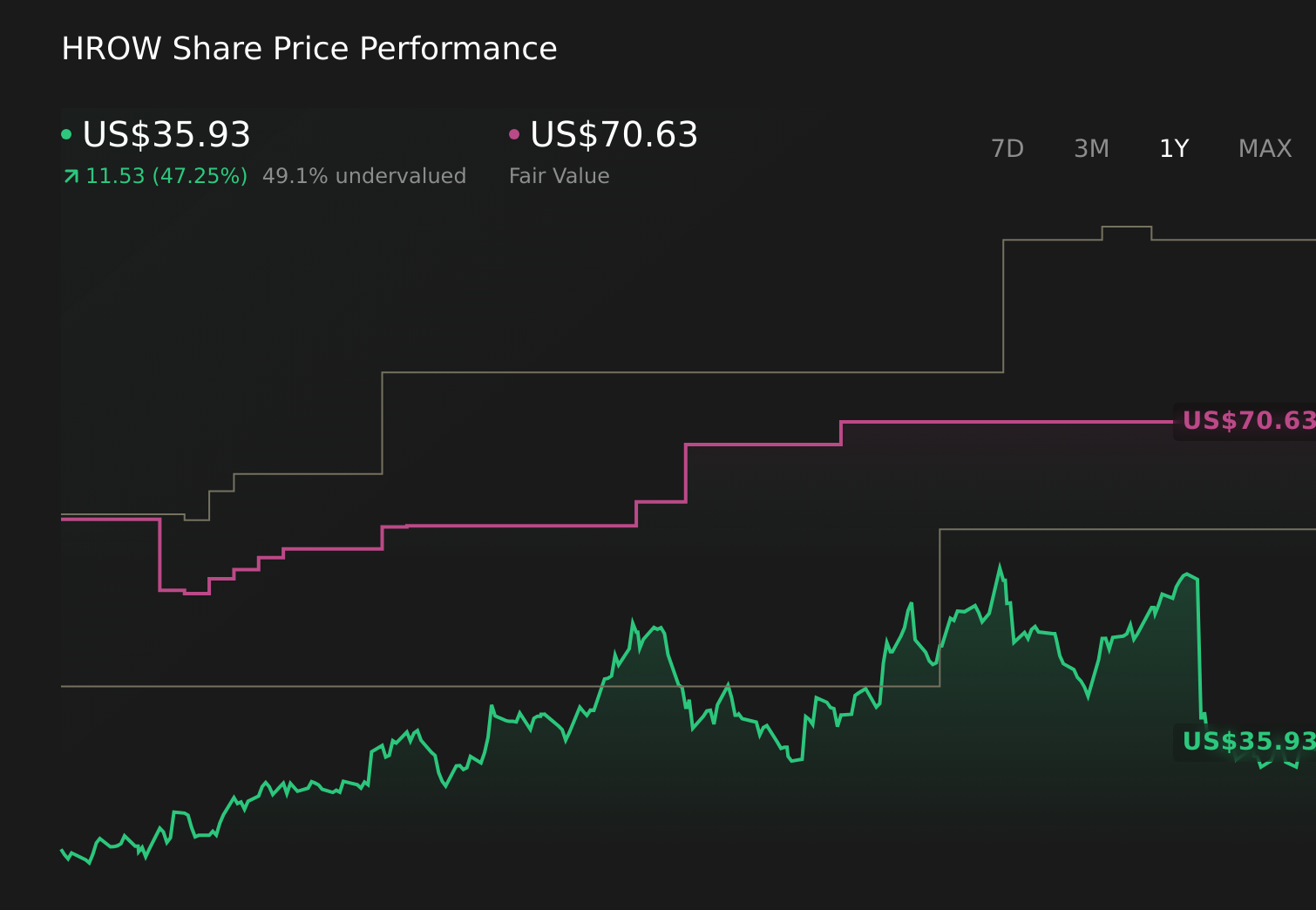

Harrow's narrative projects $784.8 million revenue and $246.0 million earnings by 2029. This requires 42.9% yearly revenue growth and a $261.0 million earnings increase from -$15.0 million today.

Uncover how Harrow's forecasts yield a $68.38 fair value, a 60% upside to its current price.

Exploring Other Perspectives

Before Grow Funds’ exit, the most optimistic analysts were assuming Harrow could lift annual revenue toward about US$866 million by 2029 and sharply expand margins, which is a much more bullish view than the more cautious concerns around concentration and earnings volatility highlighted by the recent earnings miss.

Explore 3 other fair value estimates on Harrow - why the stock might be worth just $59.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Harrow research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Harrow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harrow's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.