How Higher Energy Costs And Europe Weakness At O-I Glass (OI) Have Changed Its Investment Story

O-I Glass Inc OI | 0.00 |

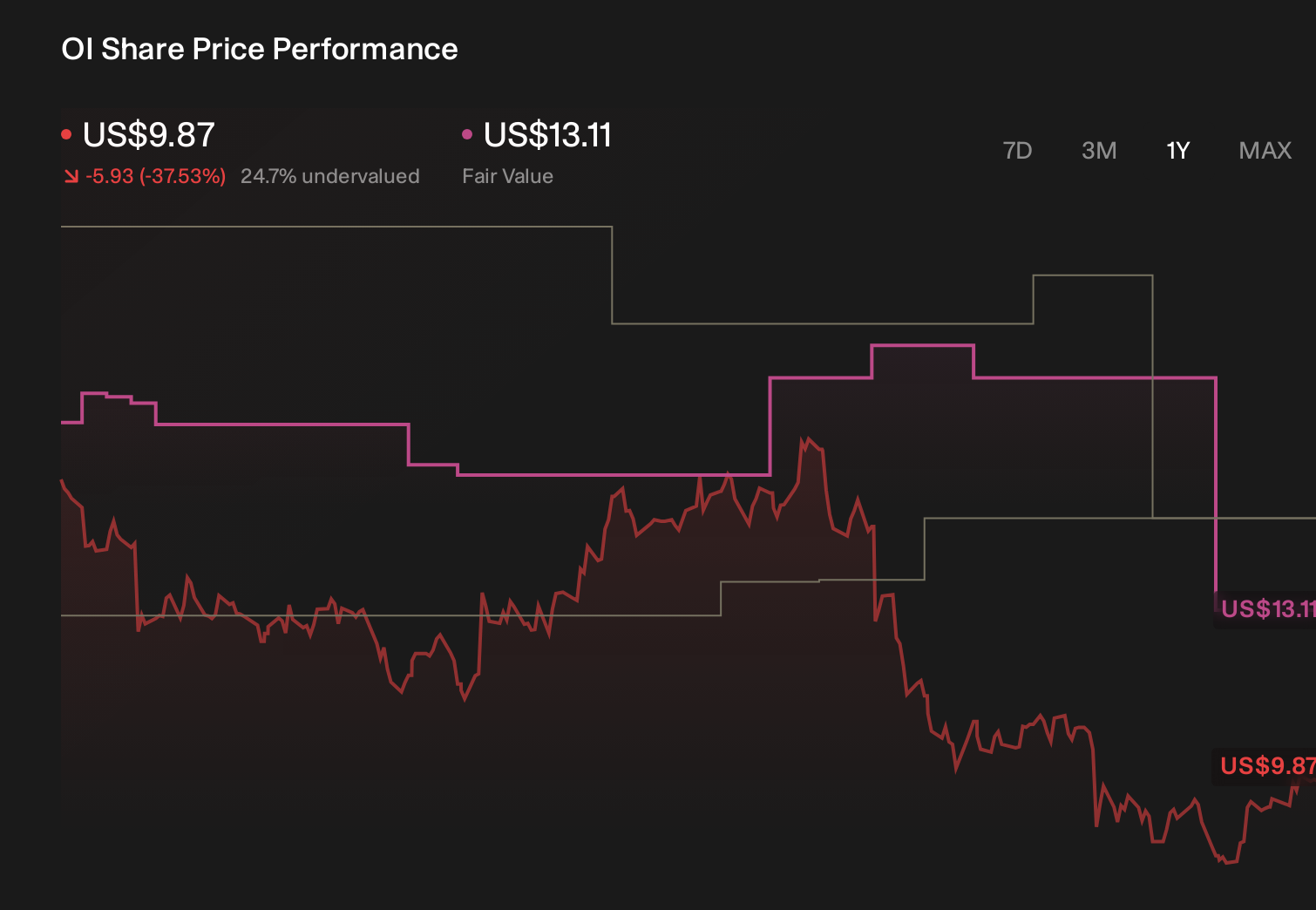

- Earlier in 2026, O-I Glass reported a first-quarter earnings miss and cut its full-year guidance, citing higher global energy costs and persistent weakness in its European operations.

- The guidance reset highlights how sensitive O-I Glass’s margins are to energy inflation and regional demand softness, especially in slower-growing European end markets.

- We’ll now examine how this guidance cut, driven by rising energy costs, may reshape O-I Glass’s existing investment narrative.

Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

O-I Glass Investment Narrative Recap

To own O-I Glass today, you need to believe glass packaging remains attractive enough for the company to turn its cost and efficiency work into consistent profits, even as volumes in Europe stay pressured. The Q1 2026 earnings miss and guidance cut directly affect the near term catalyst of margin improvement, because higher energy costs and weaker European demand squeeze profitability. They also sharpen the biggest current risk: that cost savings cannot fully offset persistent energy and regional headwinds.

Among recent announcements, the Q1 2026 results are most relevant here, with sales of US$1,540 million and a net loss of US$73 million. This step down from the prior year, together with lower full year guidance, sits awkwardly alongside earlier expectations that programs like Fit to Win and network optimization would steadily lift margins. It puts more weight on upcoming quarters, including Q2 2026, as key checkpoints on whether the cost actions can still act as a catalyst.

Yet even if you accept the long term case for glass, the way higher energy costs could compound existing volume weakness is something investors should be aware of...

O-I Glass' narrative projects $6.6 billion revenue and $380.4 million earnings by 2029.

Uncover how O-I Glass' forecasts yield a $17.89 fair value, a 104% upside to its current price.

Exploring Other Perspectives

Before this setback, the most optimistic analysts were assuming revenue of about US$6.9 billion and earnings of roughly US$502 million by 2029, which paints a far more upbeat picture than the current guidance reset suggests and contrasts with concerns about energy driven margin pressure; as a shareholder you should expect views like this to be challenged and updated over time, and be open to comparing several different scenarios for O-I’s future.

Explore 3 other fair value estimates on O-I Glass - why the stock might be worth just $15.00!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your O-I Glass research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free O-I Glass research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate O-I Glass' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.