How Investors Are Reacting To Booz Allen (BAH) Balancing Lower Sales With Higher EPS And A Steady Dividend

Booz Allen Hamilton Holding Corporation Class A BAH | 0.00 |

- Booz Allen Hamilton Holding reported past fourth-quarter 2026 sales of US$2,783 million and net income of US$205 million, alongside full-year sales of US$11.22 billion and net income of US$851 million, and also affirmed a quarterly dividend of US$0.59 per share payable on June 26, 2026.

- The combination of lower annual sales but higher quarterly earnings per share, together with a maintained dividend, highlights management’s emphasis on profitability and ongoing cash returns to shareholders.

- Next, we’ll examine how the mixed revenue and earnings trends, paired with the continued dividend, influence Booz Allen’s investment narrative.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Booz Allen Hamilton Holding Investment Narrative Recap

To own Booz Allen Hamilton, you generally need to believe in steady demand for its government-focused technology and cyber services, supported by disciplined profitability and cash returns. The latest results show softer annual sales but better Q4 earnings per share and a maintained US$0.59 dividend, which does not fundamentally change the near term catalyst of converting backlog into revenue, or the key risk of contract timing and budget pressure from major federal clients.

The most relevant development here is Booz Allen’s deeper integration with Anduril’s Menace and Lattice platforms, bringing its Sit(x), DETS, and Zero Trust tools onto a single tactical edge system. This aligns directly with the catalyst around expanding higher value, tech-enabled offerings in AI, cyber, and mission software, which could become increasingly important if traditional consulting activity faces more procurement friction or pricing pressure.

Yet behind the stable dividend and contract wins, investors should also be aware of increasing pressure from evolving federal contract structures and how quickly that could...

Booz Allen Hamilton Holding's narrative projects $12.3 billion revenue and $725.2 million earnings by 2029. This requires 2.5% yearly revenue growth and a $107.8 million earnings decrease from $833.0 million.

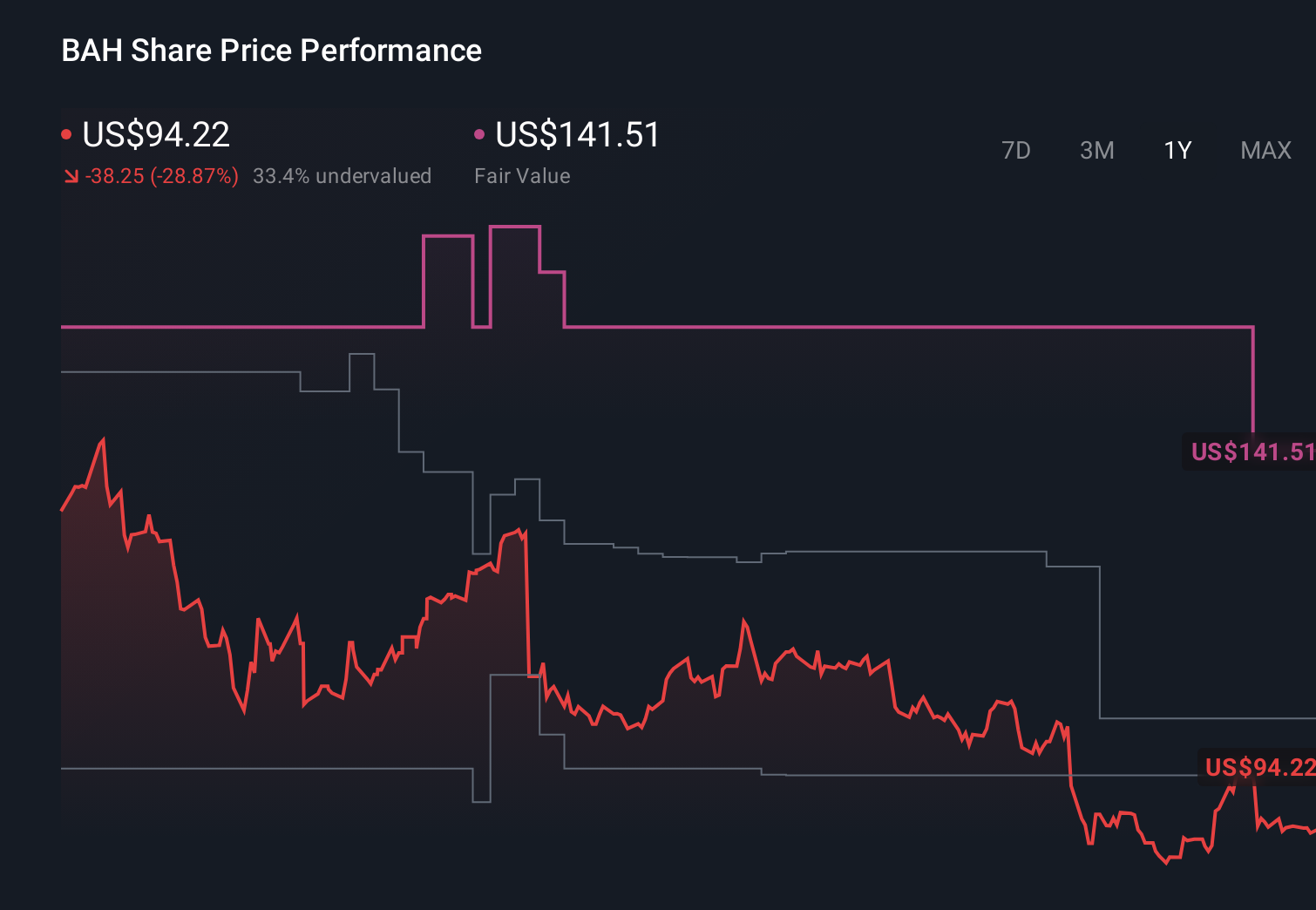

Uncover how Booz Allen Hamilton Holding's forecasts yield a $97.83 fair value, a 24% upside to its current price.

Exploring Other Perspectives

While consensus focuses on backlog and tech partnerships, the most bearish analysts were already assuming only about 2.1% annual revenue growth and earnings of roughly US$764 million, so this earnings and dividend update could either soften or reinforce that more cautious AI and cyber consulting story, depending on how you interpret it.

Explore 7 other fair value estimates on Booz Allen Hamilton Holding - why the stock might be worth as much as 82% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Booz Allen Hamilton Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Booz Allen Hamilton Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Booz Allen Hamilton Holding's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 29 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.