How Investors Are Reacting To Brink's (BCO) Upgraded Zacks Rank And Earnings Outlook Shift

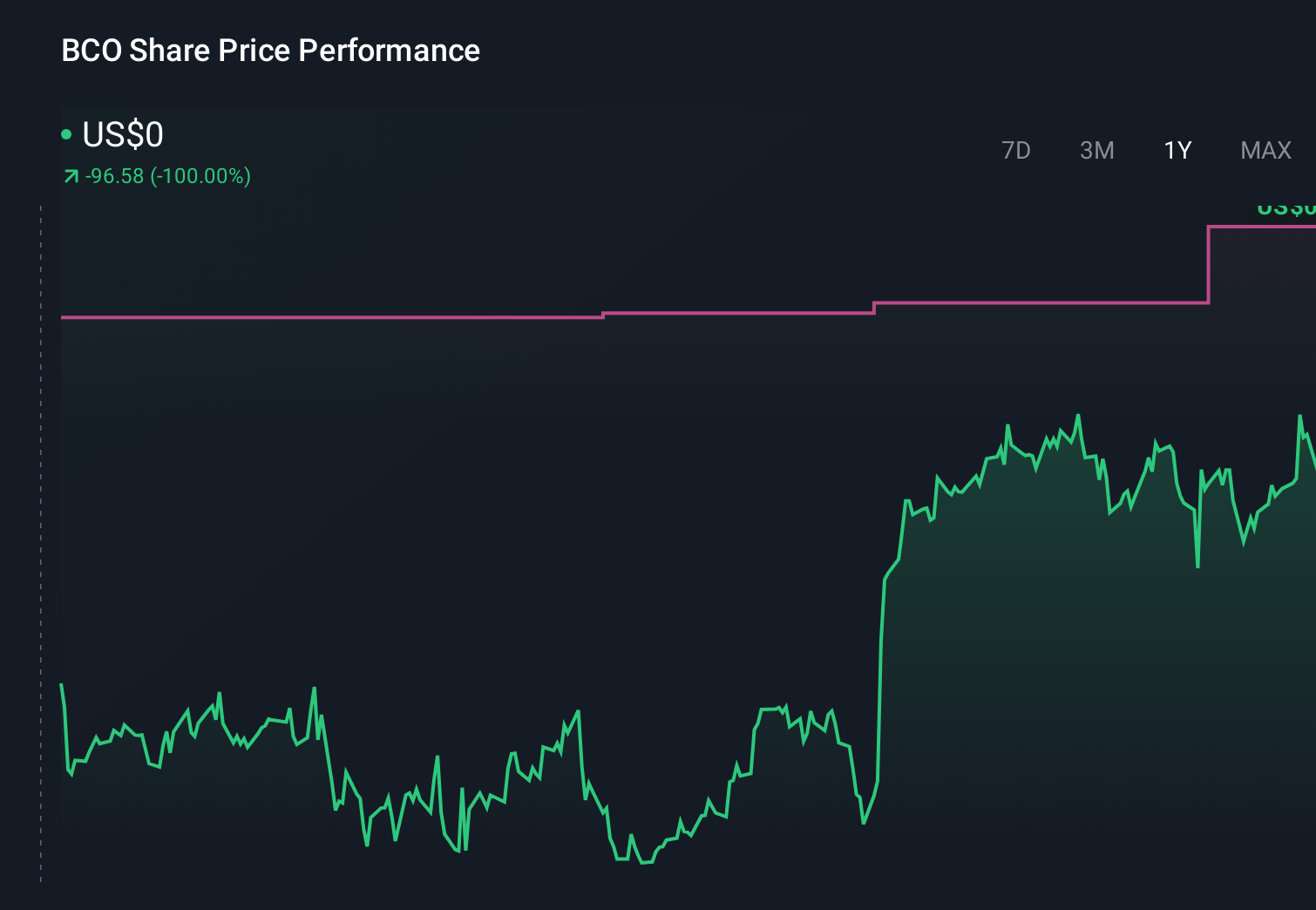

Brink's Company BCO | 0.00 |

- Recently, Zacks upgraded Brink's to a Rank #2 (Buy), citing a positive shift in analyst earnings estimates and a stronger earnings outlook for the company.

- This ratings change highlights how revisions to profit expectations can shape investor perception of Brink's evolving cash-management and digital services business model.

- Next, we'll examine how this more optimistic earnings outlook might influence Brink's broader investment narrative built around AMS and digital solutions.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Brink's Investment Narrative Recap

To own Brink’s, you need to believe its shift toward higher margin AMS and digital solutions can offset structural pressure on cash usage, while the NCR Atleos acquisition is integrated without eroding profitability. The Zacks Rank upgrade reflects improved earnings expectations, but does not materially change the near term focus on execution risk around elevated debt levels and margin pressures from technology investment and competition.

Among recent announcements, Brink’s amended and expanded its credit facilities to US$3,850,000,000 to help fund the pending NCR Atleos acquisition. This financing move directly ties into the key catalyst of scaling AMS and digital offerings, but it also heightens the importance of Brink’s managing interest costs and maintaining healthy coverage ratios as it leans further into growth tied to cash handling infrastructure.

Yet investors should be aware that higher leverage and interest coverage constraints could quickly matter if...

Brink's narrative projects $6.3 billion revenue and $745.7 million earnings by 2029. This requires 5.4% yearly revenue growth and a roughly $565.1 million earnings increase from $180.6 million.

Uncover how Brink's forecasts yield a $153.00 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community see Brink’s fair value between US$135.82 and US$365.80, showing very different expectations for upside. When you weigh those views against the earnings driven AMS and digital growth catalyst, it becomes clear why comparing several perspectives on Brink’s future performance can be useful before making any decision.

Explore 3 other fair value estimates on Brink's - why the stock might be worth over 3x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Brink's research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Brink's research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brink's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.