How Investors Are Reacting To Crane NXT (CXT) Balancing Q1 Margin Pressure With Aggressive M&A Growth Targets

Crane NXT, Co. CXT | 0.00 |

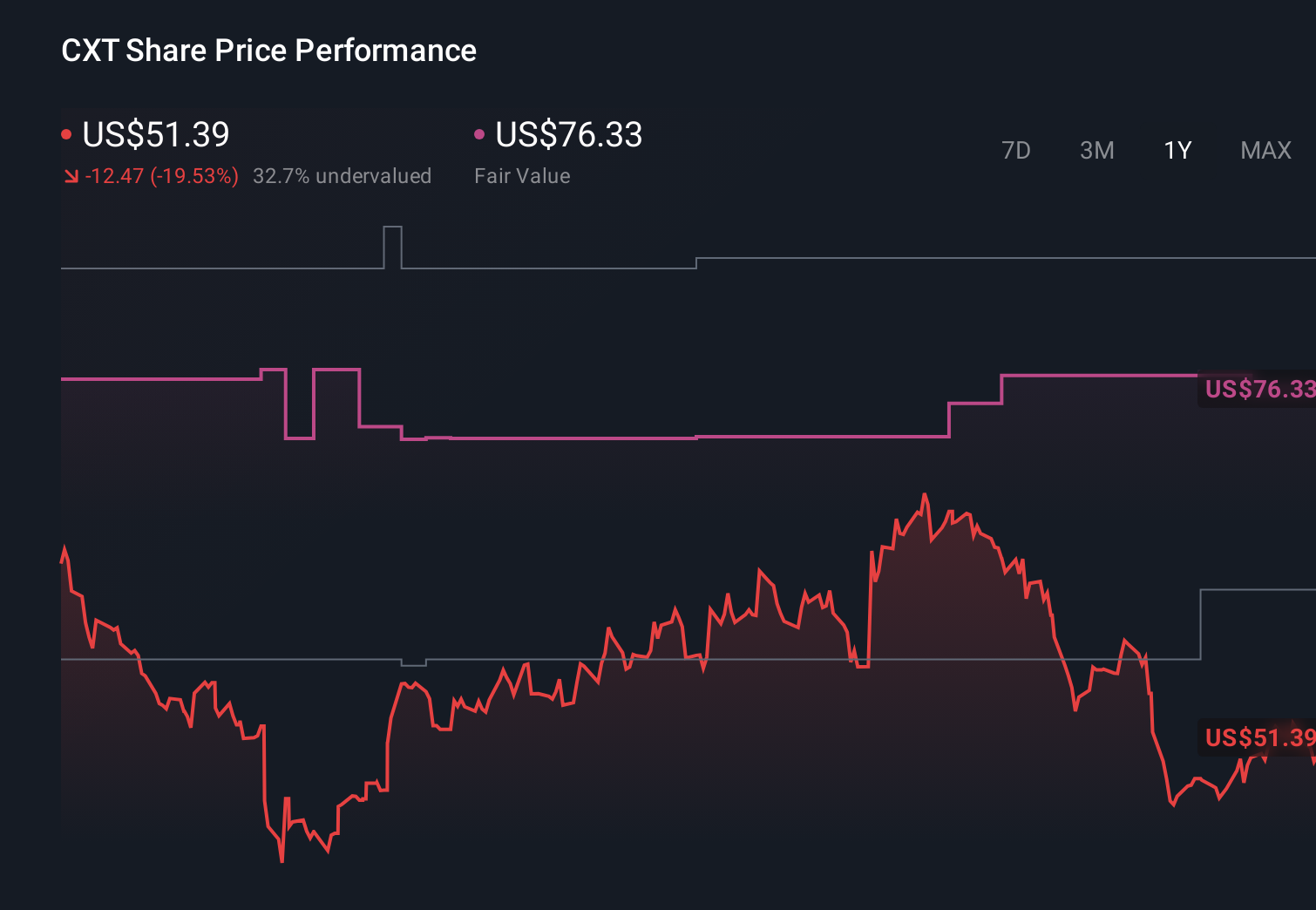

- In the past week, Crane NXT reported first-quarter 2026 results showing sales rising to US$387.7 million while net income fell to US$6.4 million, affirmed a quarterly dividend of US$0.18 per share, and outlined plans to pursue further M&A in authentication and traceability technologies.

- Management’s goal of reaching about US$2.50 billion in sales by 2028 while keeping net leverage below 3x highlights an ambition to scale primarily through disciplined acquisitions and organic investment despite current margin pressure.

- Next, we’ll examine how this acquisition-focused growth plan and Q1 margin pressure may reshape Crane NXT’s existing investment narrative.

Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

Crane NXT Investment Narrative Recap

To own Crane NXT, you need to believe the company can successfully pivot from legacy hardware and currency exposure toward higher value authentication and traceability solutions, largely through disciplined M&A. The key near term catalyst is whether recent acquisitions translate into improving margins, while the biggest risk remains execution on integrations against a backdrop of weaker profitability. The latest Q1 results, with higher sales but sharply lower net income, reinforce that this margin risk is very real rather than theoretical.

Among the recent announcements, management’s plan to reach about US$2,500 million in sales by 2028 while keeping net leverage below 3x feels most relevant here. It directly ties the current margin pressure and acquisition activity to a clear growth framework, signaling that investors will likely be watching both debt metrics and profitability closely as a way to judge whether this acquisition led model is genuinely creating value or just adding complexity.

Yet behind the growth story, investors should be aware that concentrated exposure to cash based and hardware heavy authentication markets could...

Crane NXT's narrative projects $1.8 billion revenue and $238.1 million earnings by 2029.

Uncover how Crane NXT's forecasts yield a $70.50 fair value, a 58% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$2.0 billion and earnings of roughly US$369 million by 2028, so you may find their more pessimistic view especially relevant when you weigh this Q1 margin setback against the promise of M&A led expansion.

Explore 4 other fair value estimates on Crane NXT - why the stock might be worth just $49.27!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Crane NXT research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Crane NXT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crane NXT's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.