How Investors Are Reacting To Customers Bancorp (CUBI) Strong Q1 Earnings, Lower Charge-Offs, And Share Buybacks

Customers Bancorp, Inc. CUBI | 0.00 |

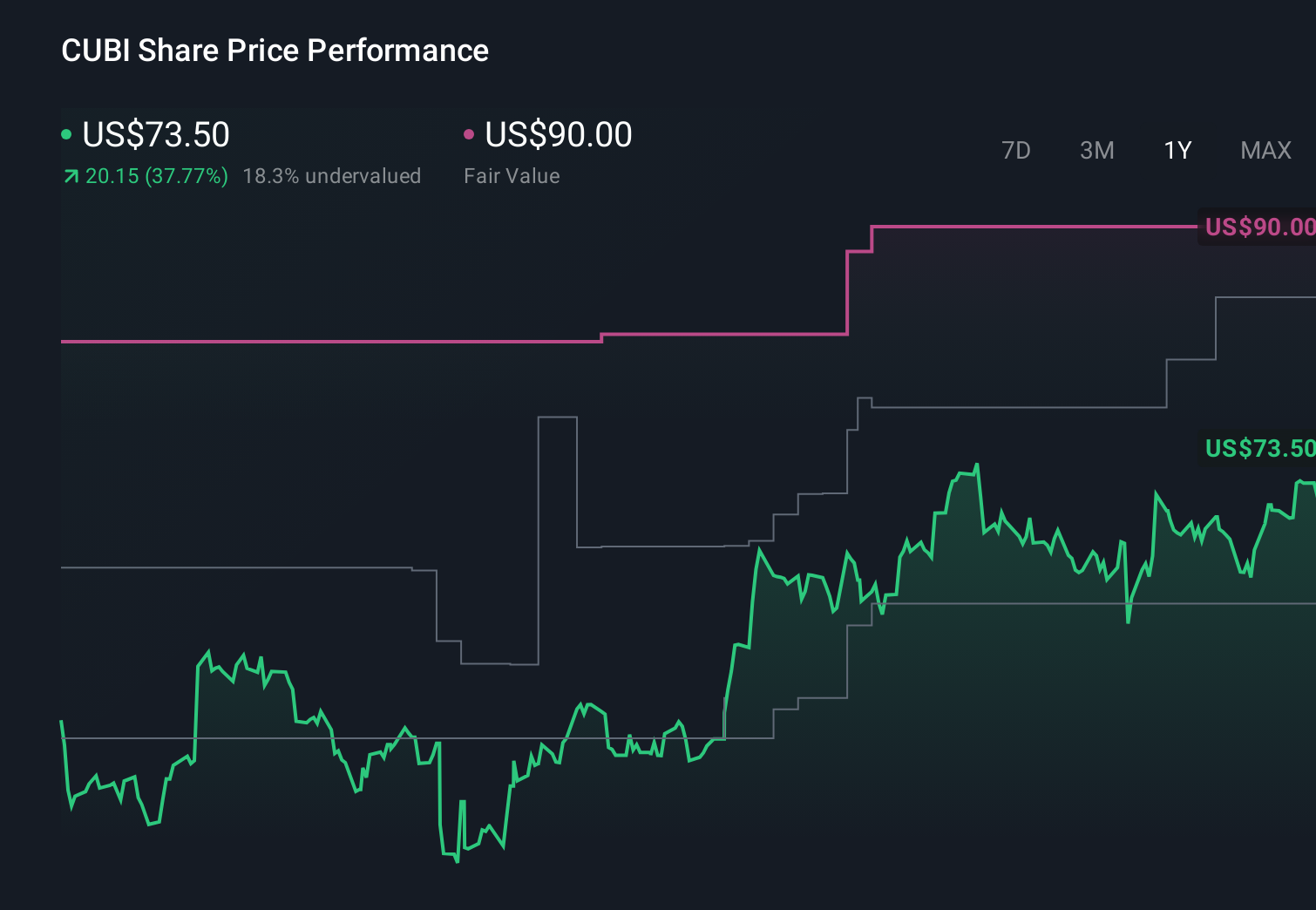

- Customers Bancorp, Inc. reported first-quarter 2026 results on April 23, 2026, posting higher net interest income of US$191.35 million, net income of US$69.65 million, and basic earnings per share from continuing operations of US$2.04, alongside lower net charge-offs of US$13.26 million and completion of a 621,668-share buyback for US$42.3 million.

- The combination of stronger profitability metrics, improved credit costs, and capital returned through buybacks highlights how the bank’s current operating model is generating higher earnings power while still managing asset quality and shareholder returns.

- We’ll now examine how this jump in quarterly net income and earnings per share may influence Customers Bancorp’s existing investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Customers Bancorp Investment Narrative Recap

To own Customers Bancorp, you need to believe its tech-focused commercial banking model and cubiX platform can keep attracting sticky deposits and fee income while managing niche credit and regulatory risks. The latest quarter’s stronger net interest income, higher earnings, and lower net charge-offs reinforce the near term earnings catalyst but do not remove concerns around digital asset deposit concentration, which still looks like the most important risk to watch.

The freshly completed repurchase of 621,668 shares for US$42.3 million sits alongside the Q1 2026 earnings beat as the most relevant update here, since it directly affects per share metrics that many investors track as a short term driver. Combined with improving credit costs, this capital return sharpens attention on how sustainable current profitability is if funding costs rise or digital asset related deposits prove less stable than expected.

Yet beneath the strong quarter, investors should still be aware of how quickly digital asset related deposits could move if...

Customers Bancorp's narrative projects $958.3 million revenue and $387.9 million earnings by 2029.

Uncover how Customers Bancorp's forecasts yield a $90.00 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Compared with the consensus view, the lowest analysts sound far more cautious, even though they were still assuming revenue of about US$975.1 million and earnings near US$387.4 million by 2029. If you worry that rising fintech competition and digital disruption could slow fee growth despite this strong Q1, their more pessimistic take offers a useful counterpoint to explore.

Explore 3 other fair value estimates on Customers Bancorp - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Customers Bancorp research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Customers Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Customers Bancorp's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.