How Investors Are Reacting To Federated Hermes (FHI) Rising AUM And Schneider Downs’ Concentrated Bet

Federated Hermes, Inc. Class B FHI | 0.00 |

- In the first quarter of 2026, Schneider Downs Wealth Management Advisors increased its position in Federated Hermes to about US$3.56 million, bringing the asset manager to roughly 17% of Schneider Downs’ reportable assets under management as disclosed in a May 14 SEC filing.

- This concentration coincided with Federated Hermes reporting record assets under management and strong revenue growth, underlining how the firm’s money market and equity products are attracting sizeable institutional allocations.

- Next, we’ll consider how Federated Hermes’ record assets under management and growing institutional interest may influence its existing investment narrative.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Federated Hermes Investment Narrative Recap

To own Federated Hermes, you generally need to believe that its scale in money market and active equity products can support resilient fee revenue, even as competition and fee pressure remain real. The Schneider Downs move adds another data point that institutional allocators are comfortable concentrating in Federated Hermes, but it does not materially change the near term catalyst around money market asset trends or the key risk from industry wide fee compression and passive alternatives.

Among recent updates, the first quarter 2026 result, with revenue of US$478.96 million and record assets under management, is most relevant to Schneider Downs’ allocation. It anchors the idea that higher money market and equity balances are still supporting the core business, while also keeping attention on whether asset growth can translate into sustained profitability in the face of rising compliance demands and growing regulatory complexity.

Yet against these positives, investors should still consider how fee compression and passive products could affect Federated Hermes over time...

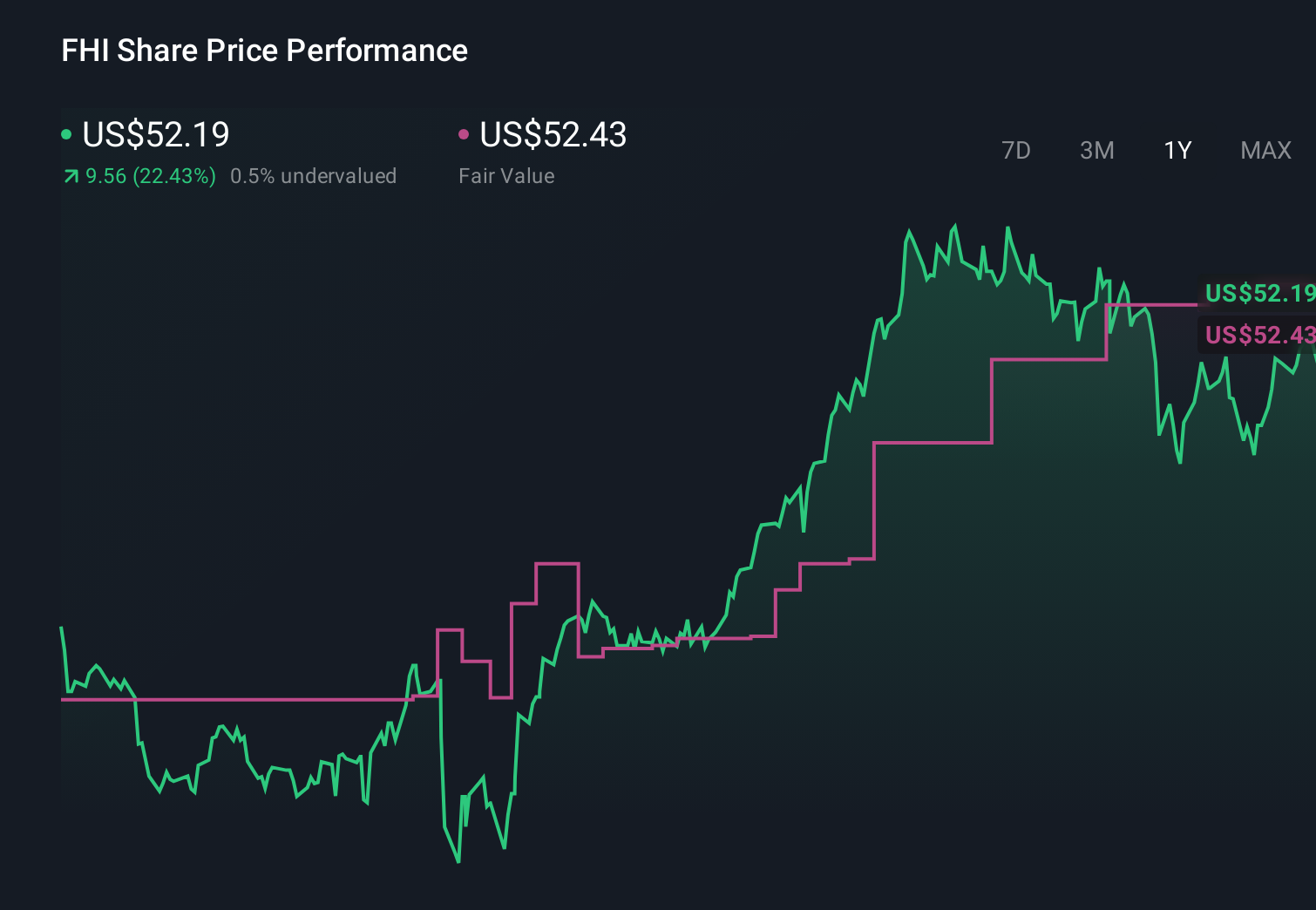

Federated Hermes' narrative projects $2.0 billion revenue and $422.2 million earnings by 2029. This requires 2.3% yearly revenue growth and about a $41.8 million earnings increase from $380.4 million today.

Uncover how Federated Hermes' forecasts yield a $57.14 fair value, in line with its current price.

Exploring Other Perspectives

Four Simply Wall St Community fair value estimates for Federated Hermes span roughly US$52 to US$69 per share, underscoring how far apart individual views can be. When you weigh these against the risk of ongoing fee compression across active asset managers, it becomes even more important to compare several perspectives before forming your own view.

Explore 4 other fair value estimates on Federated Hermes - why the stock might be worth as much as 22% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Federated Hermes research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Federated Hermes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Federated Hermes' overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.