How Investors Are Reacting To Millicom (TIGO) Revenue Jump And Profit Squeeze From Recent Acquisitions

Millicom International Cellular SA TIGO | 0.00 |

- Millicom International Cellular’s first-quarter 2026 results, released earlier this week, showed revenue rising to US$1.99 billion from US$1.37 billion a year earlier, while net income declined to US$109 million and earnings per share fell to US$0.65 amid higher restructuring and integration costs.

- The quarter underlined how recent acquisitions across Colombia, Chile, Ecuador, and Uruguay are rapidly expanding Millicom’s scale and service revenues, but also increasing leverage and near-term restructuring expenses as the company works to capture cost savings and cash flow benefits.

- We’ll now examine how this acquisition-fueled revenue growth and management’s reaffirmed cash flow targets could influence Millicom’s existing investment narrative.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Millicom International Cellular Investment Narrative Recap

To own Millicom today, you need to believe that its larger Latin American footprint can convert into durable cash generation despite higher leverage, intense competition, and currency swings. The Q1 2026 results reinforce that the key near term catalyst remains management’s ability to turn acquisition driven revenue into the at least US$900 million equity free cash flow target, while the biggest risk is that rising debt and refinancing needs strain interest coverage if conditions worsen.

The recent upsized US$87.5 million placement of 7.375% senior notes due 2032 is particularly relevant here, because it highlights how Millicom is funding heavy integration, capex, and M&A with additional borrowing at a relatively expensive coupon. That choice ties directly into both the cash flow catalyst and the leverage risk, especially as management also commits to a US$3.00 per share dividend over the next year.

But behind the headline revenue growth, investors should be aware that rising leverage and interest costs could...

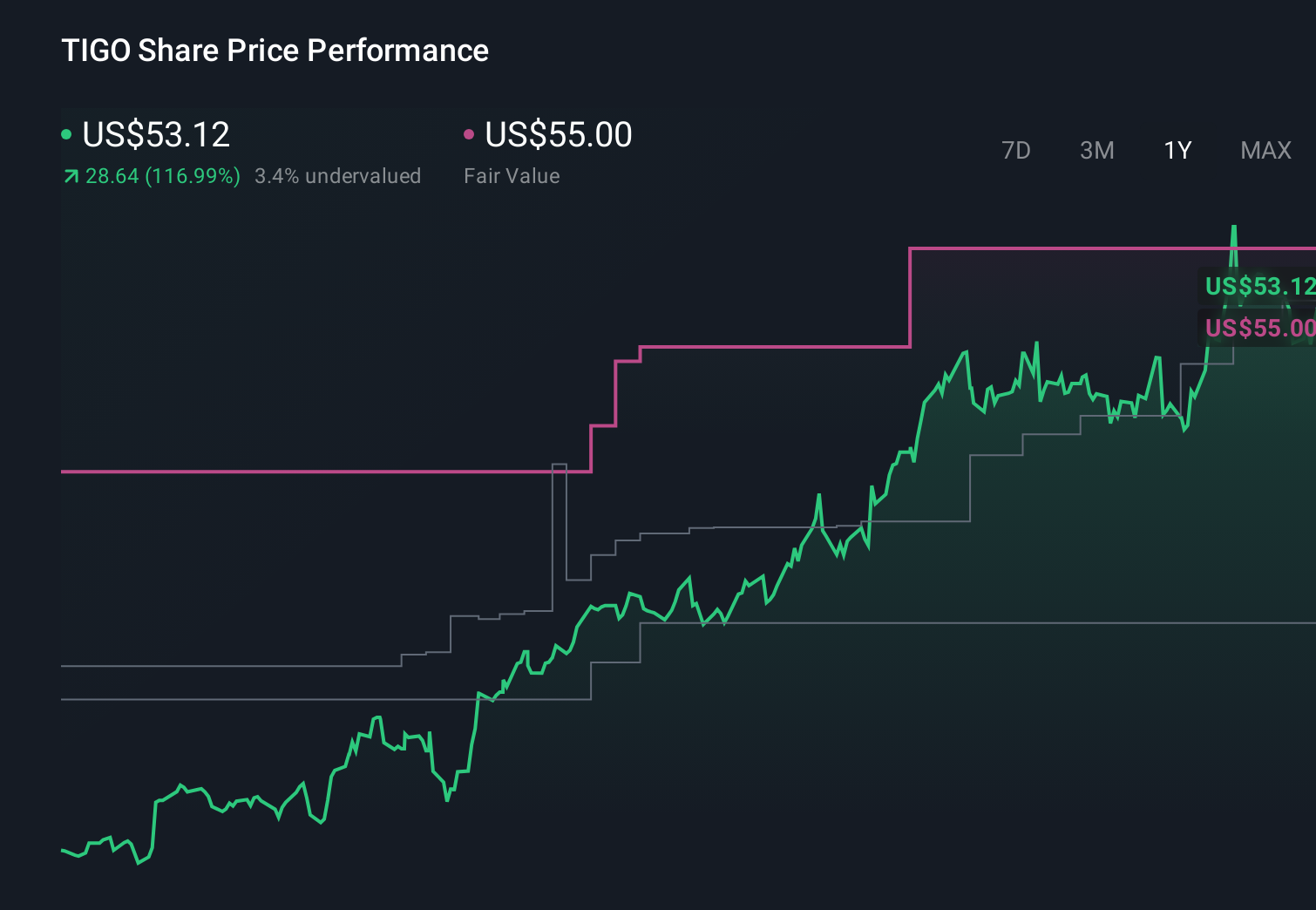

Millicom International Cellular's narrative projects $5.9 billion revenue and $628.3 million earnings by 2028. This requires 1.7% yearly revenue growth and a $326.7 million earnings decrease from $955.0 million today.

Uncover how Millicom International Cellular's forecasts yield a $52.35 fair value, a 34% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts came in far more cautious, assuming revenues drift to about US$5.8 billion and earnings fall toward US$511 million, so this latest acquisition driven quarter could challenge their view just as much as it tests your own expectations about whether competition and capex will keep squeezing margins.

Explore 8 other fair value estimates on Millicom International Cellular - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Millicom International Cellular research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Millicom International Cellular research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Millicom International Cellular's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.