How Investors Are Reacting To Philip Morris International (PM) Leadership Changes, Dividend Affirmation, And Regulatory Shifts

Philip Morris International Inc. PM | 0.00 |

- In recent days, Philip Morris International announced new regional leadership appointments effective August 1, 2026, while also affirming a quarterly dividend of US$1.4700 per share payable on July 20, 2026.

- Together with recent regulatory signals in the EU and the U.S. that appear to reduce perceived policy risk, these moves highlight how governance, cash returns, and the regulatory backdrop are all shaping Philip Morris International’s smoke-free transition.

- We’ll now examine how the evolving EU and FDA regulatory landscape could alter Philip Morris International’s existing investment narrative and risk profile.

Find 44 companies with promising cash flow potential yet trading below their fair value.

Philip Morris International Investment Narrative Recap

To own Philip Morris International today, you need to believe its shift toward smoke free products can offset pressure on traditional cigarettes while supporting high margins and dividends. The most important short term catalyst remains regulatory treatment of reduced risk products in the EU and U.S.; recent EU and FDA signals appear to modestly ease headline policy risk, but they do not remove the core uncertainty around future taxation and restrictions.

The most relevant recent announcement is the FDA guidance that signaled a more favorable enforcement stance for certain nicotine products, which may slightly reduce near term regulatory risk to IQOS and oral nicotine. This sits alongside PMI’s 66.5% gross margin and 43% of revenue from smoke free products, and it directly affects the key catalyst of whether regulation will support or constrain the company’s effort to replace declining combustible volumes.

Yet behind PMI’s smoke free progress, the risk that EU tax or product rules tighten more than expected is something investors should be very aware of...

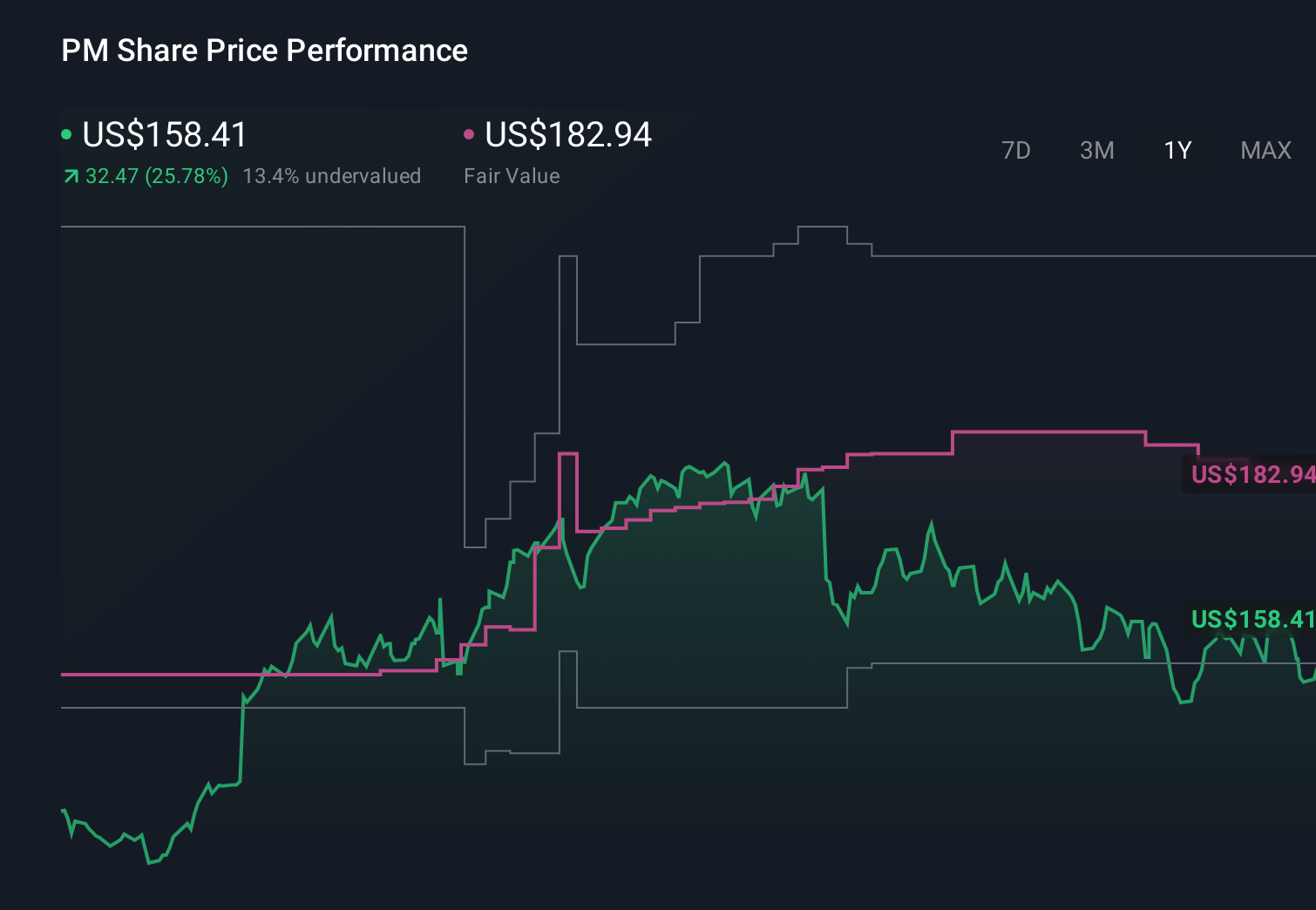

Philip Morris International's narrative projects $49.6 billion revenue and $15.3 billion earnings by 2029.

Uncover how Philip Morris International's forecasts yield a $193.14 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts take a much more cautious view, even before this news, assuming about US$47.1 billion in 2028 revenue and US$14.4 billion in earnings, so if you are weighing today’s EU and FDA developments against that more pessimistic path, it is worth recognizing how far expectations can differ and considering how fresh regulatory events might shift those scenarios.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth as much as 18% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Philip Morris International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.