How Investors Are Reacting To Rayonier (RYN) Rising Institutional Ownership And A Low P/E Multiple

Rayonier Inc. RYN | 0.00 |

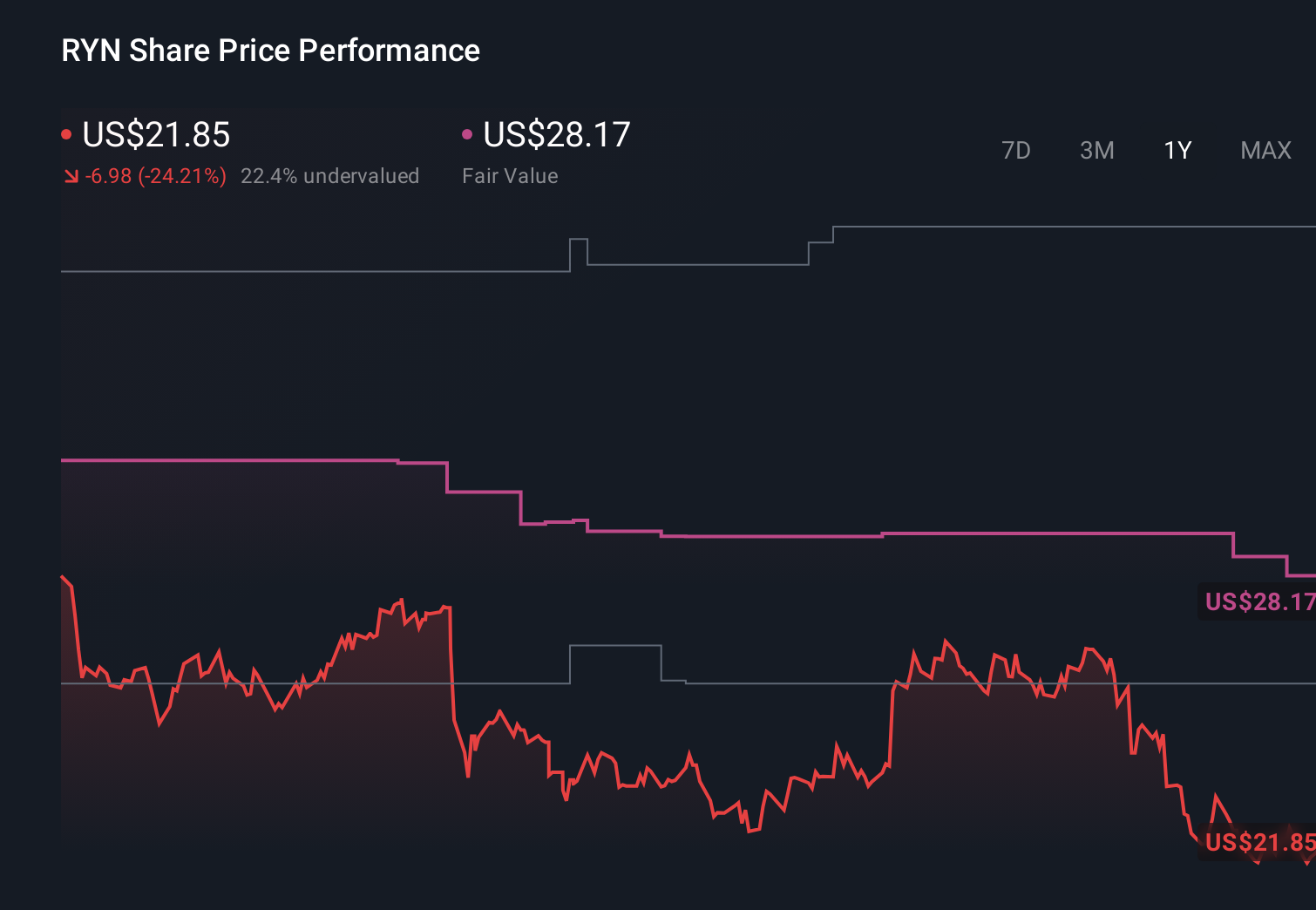

- Recently, Rayonier Inc. reported a valuation score of 8.90, placing it 52nd out of 191 Residential & Commercial REITs, alongside a P/E ratio of 6.90, while institutional shareholdings rose as major investors such as Cohen & Steers Capital Management and BlackRock increased their positions and Mason Hawkins remained the largest holder despite slightly reducing its stake.

- This combination of a relatively low earnings multiple and rising institutional ownership suggests that professional investors are taking a closer interest in Rayonier’s evolving business profile and risk‑reward trade‑off.

- We’ll now examine how this increased institutional participation could influence Rayonier’s investment narrative, including its timberland REIT positioning and growth initiatives.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Rayonier Investment Narrative Recap

To own Rayonier today, you need to be comfortable owning a timberland REIT that is trying to balance traditional timber and real estate cash flows with newer land based opportunities in renewables and carbon. The latest valuation score, low P/E multiple, and rising institutional stakes do not materially change the near term picture, where the key catalyst is how effectively the merged business executes on its timber and real estate pipeline, while climate risk and Southern timber pricing remain central concerns.

The most relevant recent announcement here is the ongoing share repurchase activity, including US$31.06 million of buybacks in the first quarter of 2026. Against a backdrop of higher institutional ownership, these buybacks tie directly into the near term catalyst of how Rayonier allocates capital between dividends, repurchases, and growth projects, and whether that mix can offset earnings volatility from weather, timber markets, and lumpier real estate income.

Yet while increased institutional interest can look reassuring, investors should still be aware of how concentrated Southern timber exposure could affect Rayonier if severe weather trends intensify...

Rayonier's narrative projects $1.5 billion revenue and $255.1 million earnings by 2029.

Uncover how Rayonier's forecasts yield a $26.83 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenue to reach about US$2.0 billion and earnings of roughly US$251.4 million, which is a very different story if rising climate and timber demand risks play out differently than they assumed, especially now that fresh valuation and ownership data could shift those expectations.

Explore 7 other fair value estimates on Rayonier - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Rayonier research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Rayonier research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Rayonier's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.