How Investors Are Reacting To STERIS (STE) Slowing Growth And Flat Margins Amid Aggressive Capital Returns

STERIS plc STE | 0.00 |

- In recent months, STERIS has reported slowing revenue growth and flat adjusted operating margins, even as it continues investing in new sterility-assurance manufacturing capacity and executing a large share repurchase program.

- This combination of modest operating progress and sizable capital deployment has prompted investors to revisit how resilient STERIS’s infection-prevention, service, and consumables platform really is across its Healthcare, Applied Sterilization Technologies, and Life Sciences segments.

- We will now explore how concerns about decelerating revenue growth and unchanged margins may reshape STERIS’s previously optimistic investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

STERIS Investment Narrative Recap

To own STERIS, you need to believe its infection-prevention platform, built on consumables, services, and installed equipment, can support steady revenue and cash generation across cycles. The recent share price decline and slower revenue growth sharpen attention on whether that recurring model can sustain near term demand, while the biggest immediate risk remains pressure on margins if hospitals and life sciences customers tighten budgets further. For now, the headline news does not appear to alter that core debate in a material way.

The most relevant recent development is STERIS’s US$1.0 billion share repurchase program, which the company is funding alongside expanded sterility-assurance manufacturing capacity. This capital deployment matters because it amplifies the impact of any slowdown in revenue growth or flat margins on per share outcomes, making the durability of its Healthcare, Applied Sterilization Technologies, and Life Sciences demand profile even more important for investors to watch.

Yet even with these supports in place, investors should be aware of the risk that hospital and biopharma customers could tighten capital budgets and pricing, which could...

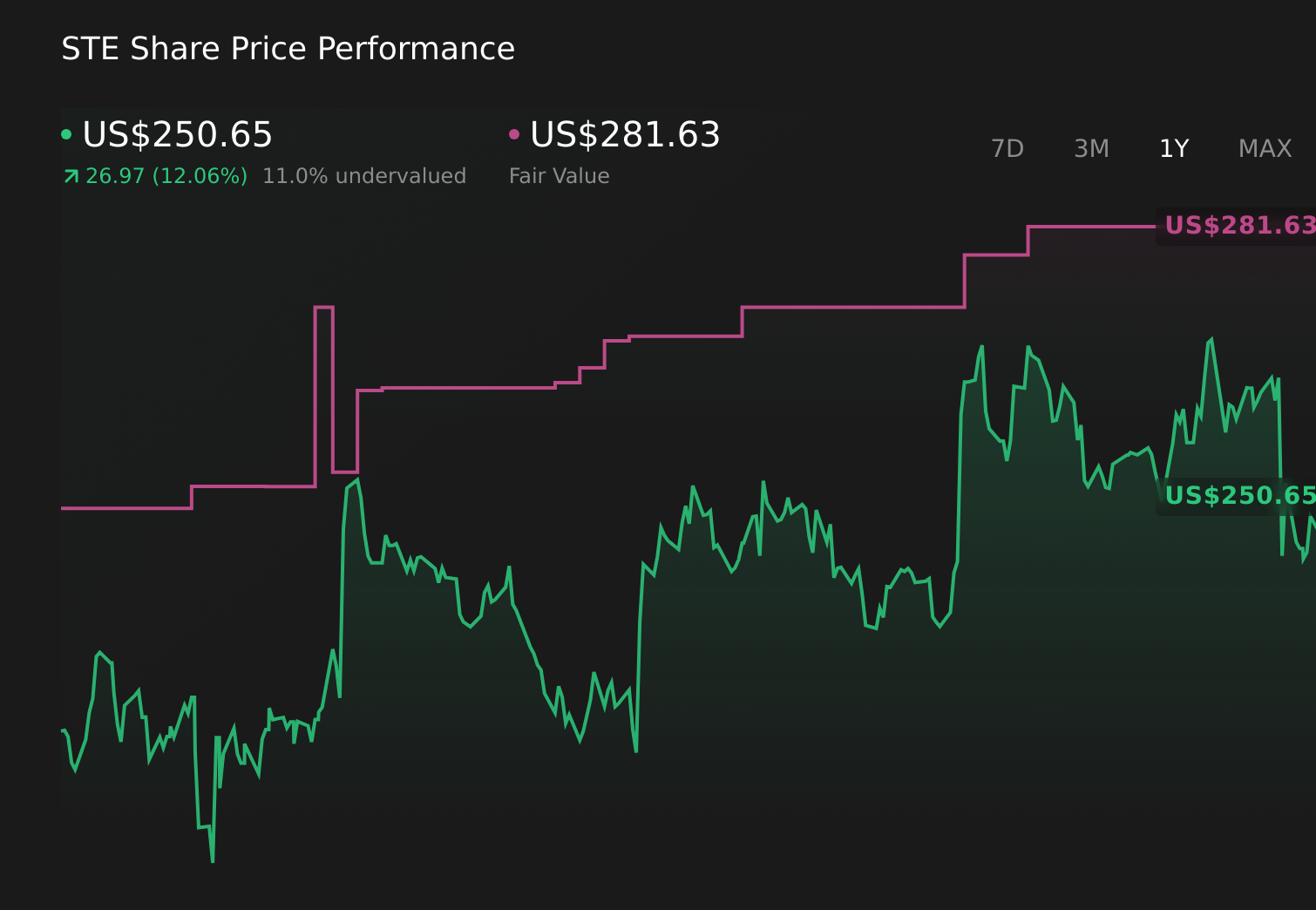

STERIS’ narrative projects $7.2 billion revenue and $1.0 billion earnings by 2029.

Uncover how STERIS' forecasts yield a $256.86 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community cluster between US$230 and about US$256.86, showing a fairly tight spread of views. Against this, concerns about slowing revenue growth and flat margins highlight why you should weigh different opinions carefully and consider how resilient STERIS’s infection prevention platform really is.

Explore 3 other fair value estimates on STERIS - why the stock might be worth just $230.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your STERIS research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free STERIS research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate STERIS' overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.