How Investors Are Reacting To Tractor Supply (TSCO) Store Expansion Amid Truist Downgrade and Softer Sales

Tractor Supply Company TSCO | 43.82 | -1.59% |

- Tractor Supply Company recently opened its 2,400th store in Aiken, South Carolina, as part of plans to add 100 new locations in 2026, while continuing community-focused efforts such as supporting Aiken Equine Rescue with a US$2,400 donation.

- Soon after this expansion milestone, Truist Securities downgraded Tractor Supply to a Hold rating, citing proprietary card data that pointed to softening sales trends and competitive pressures despite the company’s growth plans.

- We’ll now examine how Truist’s concerns about flat same-store sales and weaker demand could influence Tractor Supply’s existing investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Tractor Supply Investment Narrative Recap

To own Tractor Supply, you need to believe its rural lifestyle focus, dense store network and recurring consumables demand can offset cyclical pressure on big-ticket and discretionary spending. The recent store milestone and Truist downgrade do not materially change the near term focus for investors, which remains on Q4 results and 2026 guidance as the key catalyst, and on the risk that soft comparable sales and weaker average tickets persist longer than expected.

The most relevant recent announcement is Truist Securities cutting Tractor Supply to Hold and lowering its price target to US$55, pointing to flat Q4 same-store sales and softer demand. That directly links to the existing risk of declining comparable store sales and pressure on big ticket categories, and sets the stage for how closely the market may scrutinize upcoming guidance relative to Tractor Supply’s longer term growth ambitions.

Yet even with expansion and community goodwill, investors should be aware that pressure on comparable sales and cautious consumer demand could...

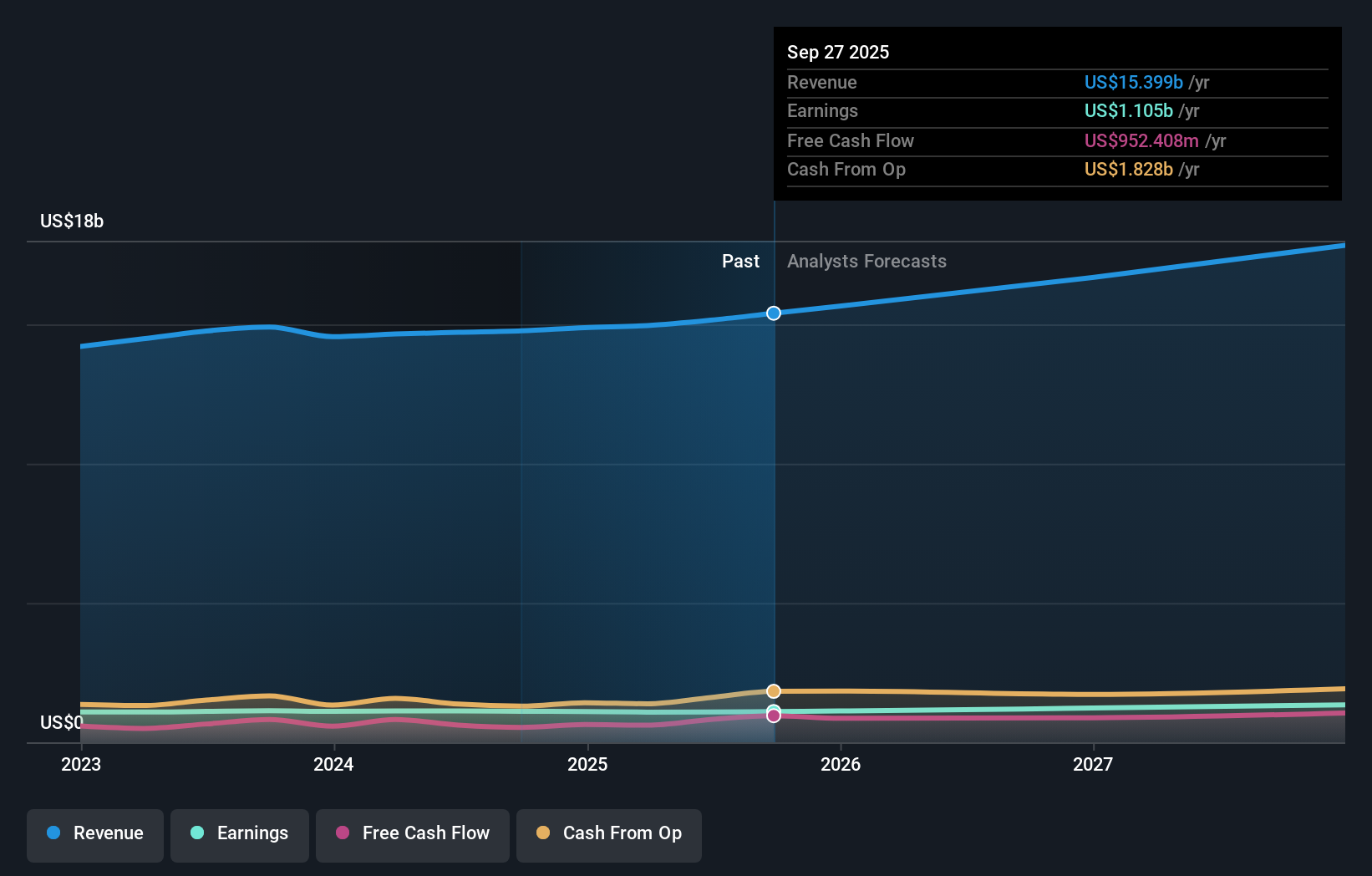

Tractor Supply's narrative projects $18.7 billion revenue and $1.4 billion earnings by 2028. This requires 7.3% yearly revenue growth and about a $0.3 billion earnings increase from $1.1 billion today.

Uncover how Tractor Supply's forecasts yield a $63.15 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community value Tractor Supply between US$36.54 and US$63.15, showing how far apart individual views can be. Against that wide spread, the recent concerns about flat comparable sales and softer demand invite you to weigh how different assumptions about growth and margins might affect Tractor Supply’s longer term performance.

Explore 5 other fair value estimates on Tractor Supply - why the stock might be worth as much as 24% more than the current price!

Build Your Own Tractor Supply Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tractor Supply research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Tractor Supply research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tractor Supply's overall financial health at a glance.

No Opportunity In Tractor Supply?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.