How Investors Are Reacting To Vulcan Materials (VMC) Q1 Earnings Beat And Completed Buyback Program

Vulcan Materials Company VMC | 0.00 |

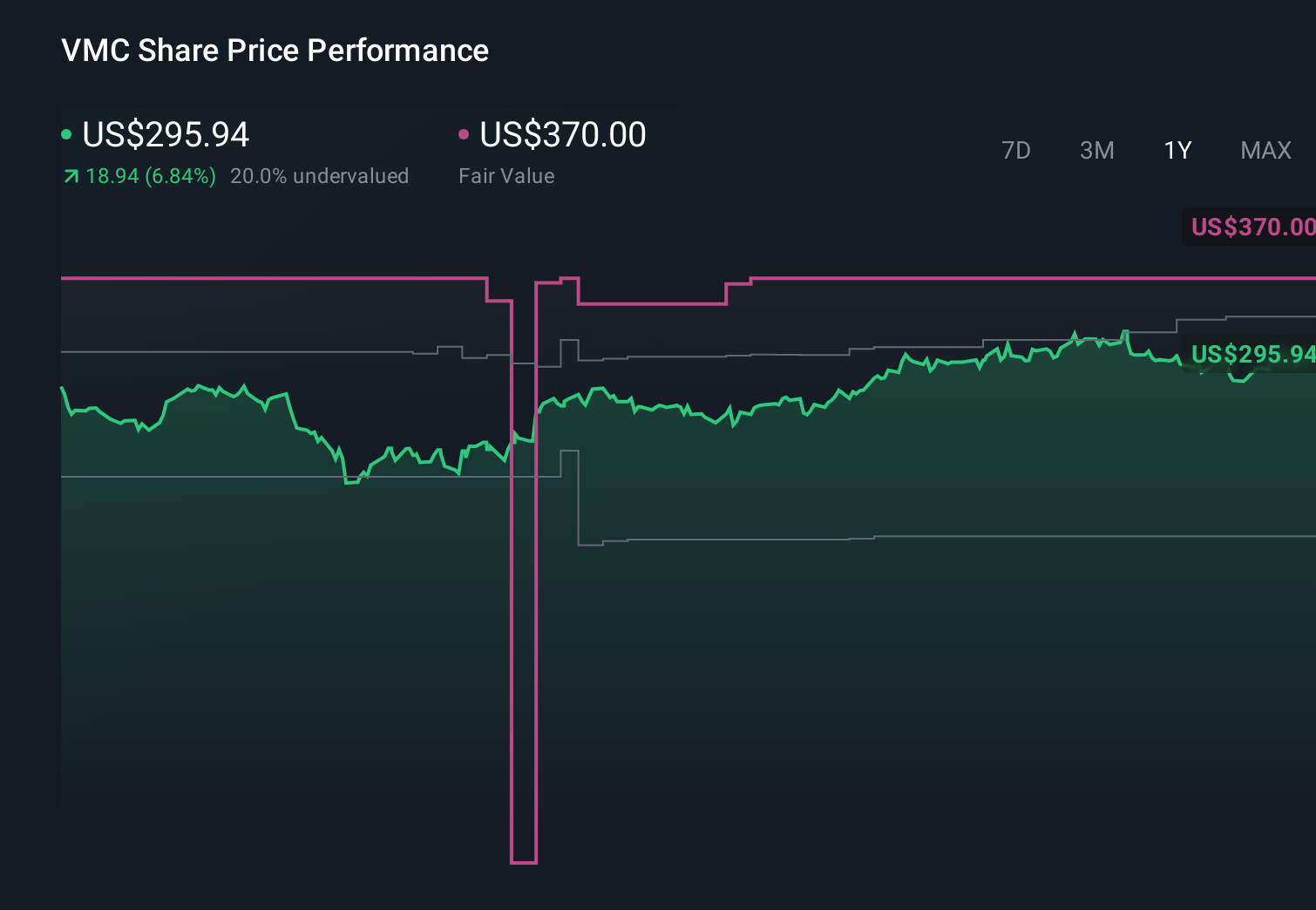

- In the first quarter of 2026, Vulcan Materials Company reported higher sales of US$1,755.9 million and net income of US$165.5 million, alongside completing a long-running US$1.77 billion share repurchase program initiated in 2006.

- This combination of stronger earnings per share and a materially reduced share count highlights how Vulcan’s aggregates-led cash generation is supporting ongoing capital returns to shareholders.

- We’ll now examine how Vulcan’s stronger first-quarter earnings and reaffirmed full-year guidance may influence its existing investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Vulcan Materials Investment Narrative Recap

To own Vulcan Materials, you need to believe in steady aggregates demand from roads, infrastructure and growth in Sunbelt markets, backed by disciplined cost control. The latest first quarter earnings beat and completion of the long-running share repurchase do not radically change that story in the near term. The most important short term catalyst remains how effectively Vulcan converts strong backlogs into margins, while the biggest risk is still project delays or funding shifts in public infrastructure.

Against that backdrop, the reaffirmed full year adjusted EBITDA guidance of US$2.4 billion to US$2.6 billion is the most relevant recent announcement. It signals that, despite higher energy and diesel costs, management is still comfortable with its earnings range. For investors watching infrastructure related catalysts, this guidance sits alongside the completed US$1,774.99 million buyback as another data point on how Vulcan is balancing growth investment with cash returns.

Yet beneath these solid quarterly numbers, the risk that infrastructure funding priorities or timing could shift remains something investors should be aware of...

Vulcan Materials' narrative projects $9.6 billion revenue and $1.5 billion earnings by 2028. This requires 8.1% yearly revenue growth and a roughly $541.9 million earnings increase from $958.1 million today.

Uncover how Vulcan Materials' forecasts yield a $327.57 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue of about US$10.0 billion and earnings near US$1.9 billion by 2029, so you may see this stronger quarter and the completed buyback as either reinforcing that upbeat view or as a reason to question it, depending on how you weigh those forecasts against ongoing risks like stricter environmental rules and higher compliance costs.

Explore 4 other fair value estimates on Vulcan Materials - why the stock might be worth as much as 27% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Vulcan Materials research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vulcan Materials research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vulcan Materials' overall financial health at a glance.

Contemplating Other Strategies?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.