How Investors May Respond To Bank of America (BAC) Q1 Earnings, Capital Returns, and AI Initiatives

Bank of America Corp BAC | 0.00 |

- In April 2026, Bank of America reported first‑quarter net interest income of US$15,745 million and net income of US$8,584 million, alongside continued bond issuance, share repurchases of 213,639,234 shares for US$10,849.31 million, and fresh common and preferred dividend declarations across its capital structure.

- Together with expanded use of artificial intelligence and a renewed co‑branded card partnership with Alaska Air Group, these moves highlight Bank of America’s focus on funding flexibility, digital efficiency, and shareholder returns across both equity and fixed‑income investors.

- We’ll now explore how Bank of America’s strong first‑quarter earnings and higher net interest income guidance may influence its investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Bank of America Investment Narrative Recap

To own Bank of America, you need to believe in its ability to convert scale, deposits, and technology into resilient earnings and disciplined capital returns. The latest quarter’s higher net interest income and firm earnings guidance support that thesis, while the biggest near term swing factor remains how funding costs and deposit competition evolve. The recent burst of bond issuance and dividend actions does not materially change that risk, but it reinforces the short term focus on net interest income.

The renewed multi year co branded card partnership with Alaska Air Group stands out because it sits at the intersection of Bank of America’s digital ambitions and fee income growth. As the bank leans on AI and card partnerships to deepen customer relationships, investors watching catalysts around earnings resilience and revenue mix may find this expansion of a long running franchise particularly relevant.

Yet even with solid earnings and expanded partnerships, investors still need to consider how rising competition for deposits could...

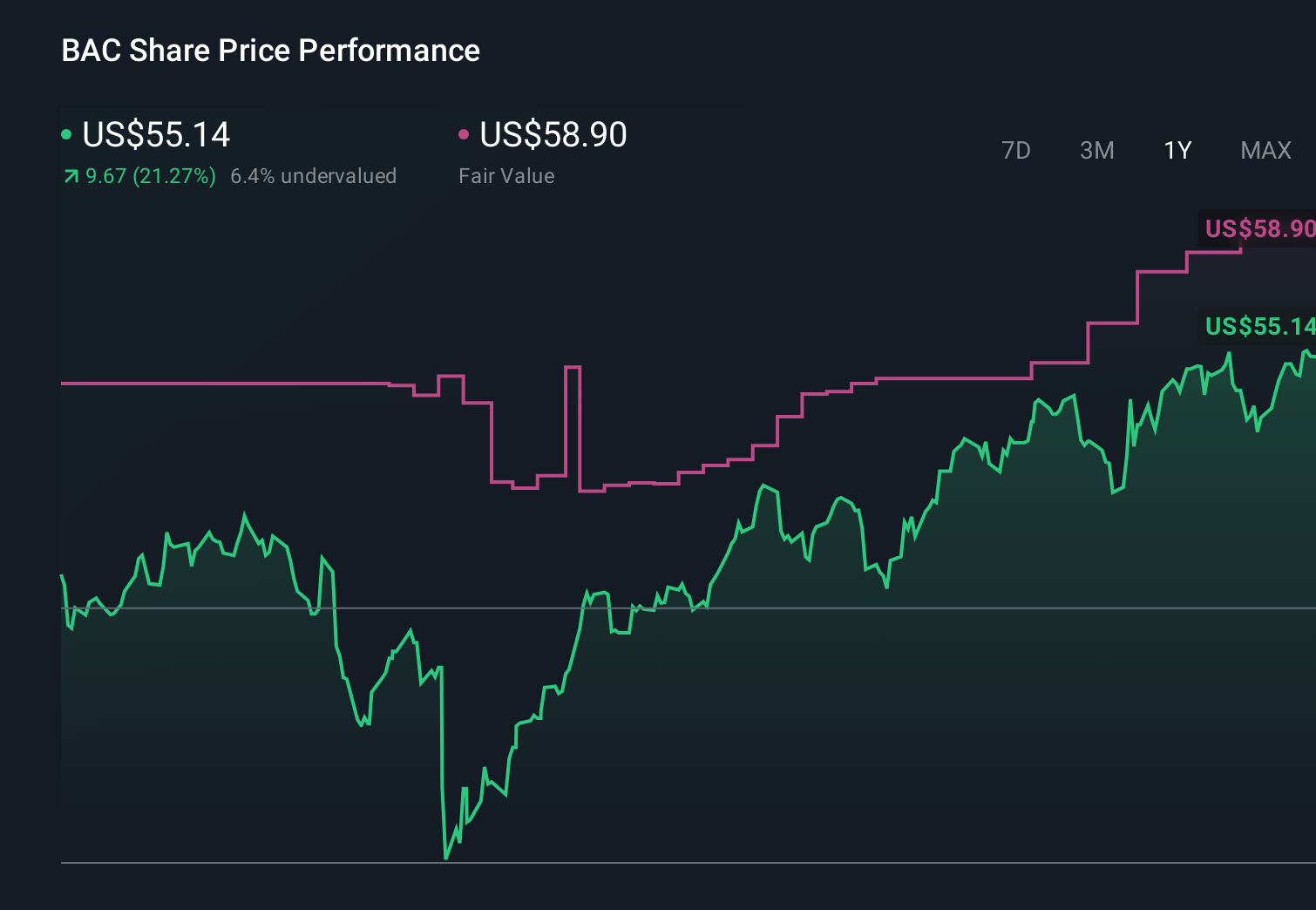

Bank of America's narrative projects $133.5 billion revenue and $36.8 billion earnings by 2029. This requires 6.8% yearly revenue growth and about a $6.5 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $62.72 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Eleven fair value estimates from the Simply Wall St Community span roughly US$52 to US$68 per share, showing how wide individual opinions can run. Against that backdrop, the bank’s push to enhance net interest income through asset repricing and balance sheet actions becomes a key lens for thinking about its longer term earnings power and invites you to weigh several contrasting views.

Explore 11 other fair value estimates on Bank of America - why the stock might be worth as much as 29% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 32 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.