How Investors May Respond To CNH Industrial (CNH) Earnings And India-Focused Manufacturing Strategy

CNH Industrial NV CNH | 10.65 | -3.36% |

- CNH Industrial recently highlighted its India-built farm mechanisation portfolio at its advanced Pune plant and, on 17 February 2026, reported fourth-quarter earnings that investors had been closely awaiting for clues on margin recovery and finance-arm performance.

- The Pune facility’s role as a hub for locally engineered, India-specific equipment underlines how CNH is using emerging-market manufacturing depth to support both domestic demand and export opportunities.

- We’ll now examine how investor focus on CNH’s upcoming margin trajectory and finance-arm performance could influence the company’s broader investment narrative.

AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

CNH Industrial Investment Narrative Recap

To own CNH Industrial today, you need to be comfortable with a cyclical machinery business that is trying to defend margins while reshaping its portfolio and finance arm. The upcoming Q4 2025 results on 17 February are a key near term catalyst, as they should shed light on margin recovery and the resilience of CNH’s captive finance business. The Pune announcement is encouraging for long term diversification, but it does not materially alter the near term risk around leverage and financing sensitivity.

The recent spotlight on CNH’s Pune plant matters because it shows how the group is deepening its India footprint just as markets are watching for signs of margin stabilisation. By producing India specific farm equipment for both local and export markets, CNH is broadening its revenue mix beyond a soft North American agriculture cycle. That could become more relevant over time if Q4 results confirm that financing and input cost pressures are constraining margin progress elsewhere.

Yet behind this progress, CNH’s high leverage and the sensitivity of its finance arm remain issues investors should be aware of...

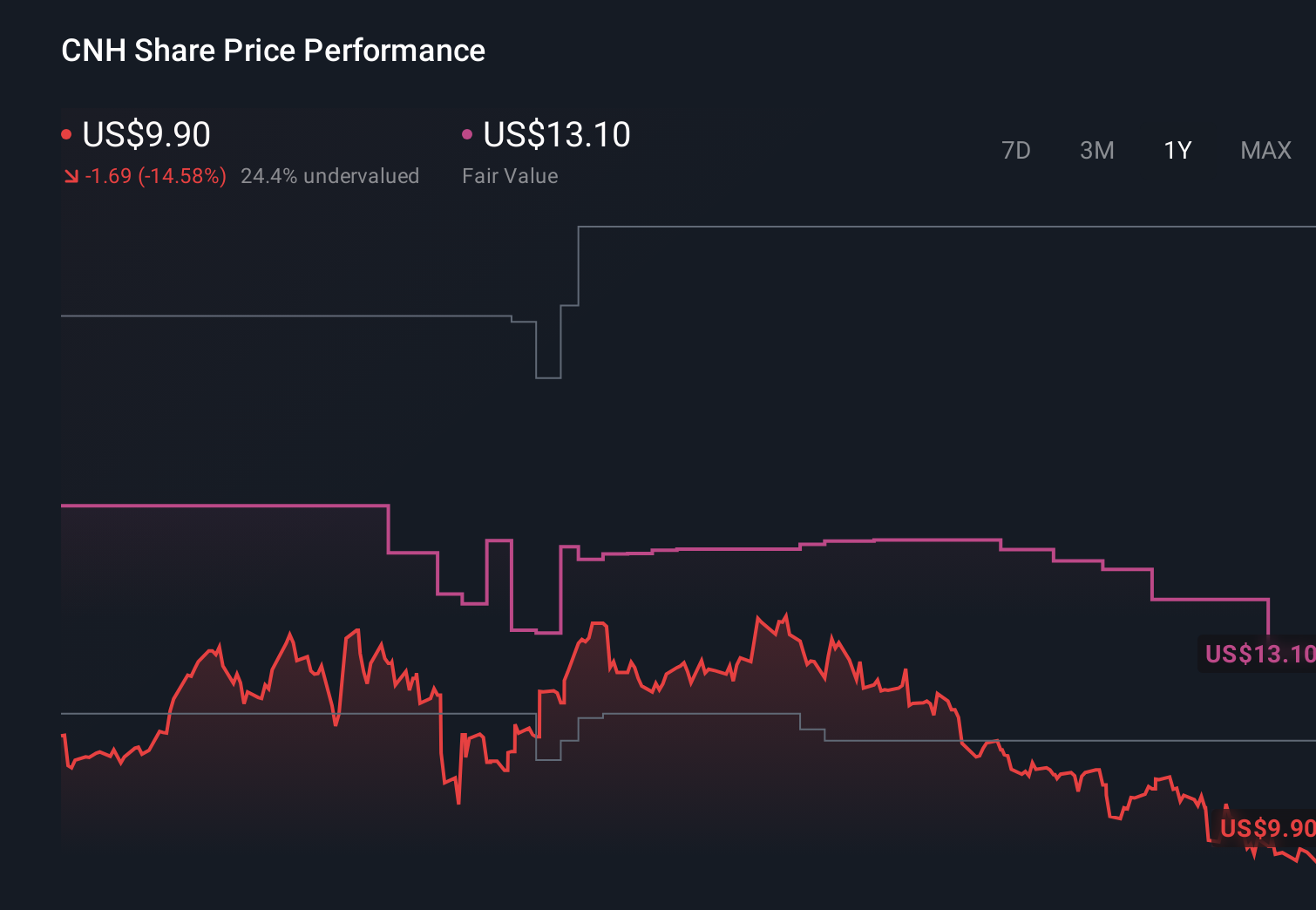

CNH Industrial's narrative projects $18.7 billion revenue and $1.6 billion earnings by 2028. This requires 1.2% yearly revenue growth and a $777.0 million earnings increase from $823.0 million today.

Uncover how CNH Industrial's forecasts yield a $12.81 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most cautious analysts were already assuming CNH’s revenue would shrink about 0.6% a year to roughly US$18.4 billion by 2028 and still see earnings only reaching about US$1.1 billion, so this latest focus on India and upcoming Q4 results could either challenge or reinforce that more pessimistic view, and it is worth you comparing those expectations with your own.

Explore 6 other fair value estimates on CNH Industrial - why the stock might be worth as much as 42% more than the current price!

Build Your Own CNH Industrial Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CNH Industrial research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free CNH Industrial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNH Industrial's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 53 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.