How Investors May Respond To Hershey (HSY) Reaffirming 2026 Outlook Amid Brand Expansion Into Zero‑Sugar Beverages

Hershey Company HSY | 0.00 |

- In late April 2026, The Hershey Company reported first-quarter sales of US$3,104.17 million and net income of US$435.11 million, declared quarterly dividends on its common and Class B shares, and reaffirmed its 2026 earnings guidance.

- A separate collaboration announced by Ryl Tea introduced zero-sugar Jolly Rancher-branded iced teas, highlighting how Hershey is extending its confectionery brands into new beverage formats.

- Now we’ll consider how Hershey’s reaffirmed full-year earnings outlook might influence the existing investment narrative around cocoa costs and diversification.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

Hershey Investment Narrative Recap

To own Hershey, you generally need to believe in the resilience of its brands and its ability to manage input costs while broadening beyond core chocolate. The reaffirmed 2026 earnings outlook suggests management still sees its plans on cocoa cost mitigation and portfolio diversification as intact, so this update does not fundamentally alter the near term focus on margin pressure as the key risk.

The most relevant announcement here is Hershey’s decision to reaffirm its 2026 guidance, including expected reported EPS of US$7.77 to US$8.19. For investors watching cocoa costs and tariff exposure, that stance sits alongside initiatives like Jolly Rancher branded Ryl zero sugar teas as evidence of how Hershey is balancing cost pressures with new revenue streams in less cocoa intensive areas.

Yet while guidance sounds reassuring, the real test for investors who are aware of cocoa and tariff risks will be whether...

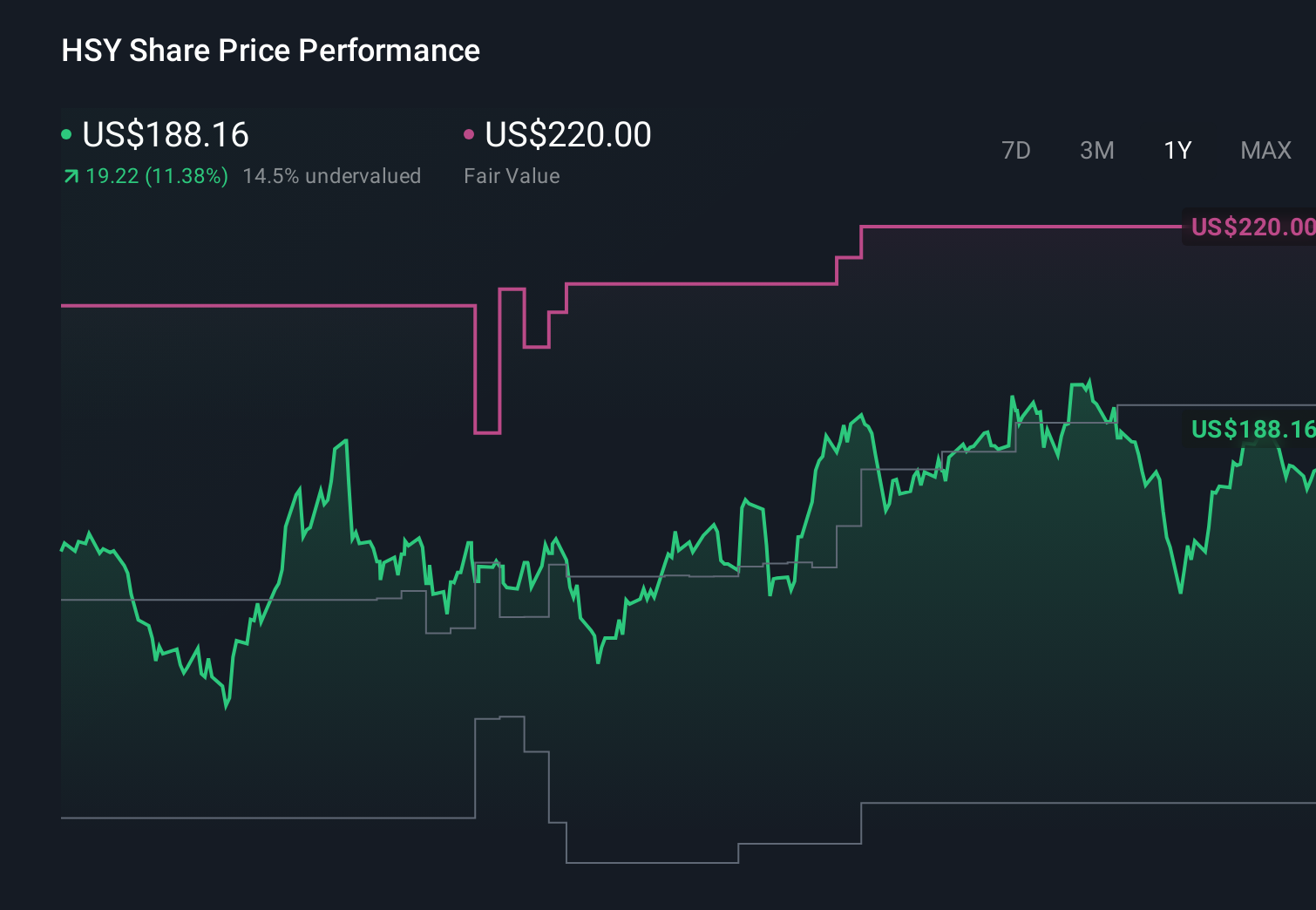

Hershey's narrative projects $12.9 billion revenue and $2.1 billion earnings by 2029. This requires 3.4% yearly revenue growth and about a $1.2 billion earnings increase from $883.3 million today.

Uncover how Hershey's forecasts yield a $227.78 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue growth near 2 percent and earnings of about US$2.1 billion by 2029, so if you worry about cocoa driven margin risk and slower confectionery demand, this latest earnings reaffirmation could either soften that pessimism or reinforce it, depending on how you read the underlying trends.

Explore 4 other fair value estimates on Hershey - why the stock might be worth 6% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hershey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hershey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hershey's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.