How Investors May Respond To O-I Glass (OI) Wider Q1 Loss Amid Slight Sales Decline

O-I Glass Inc OI | 0.00 |

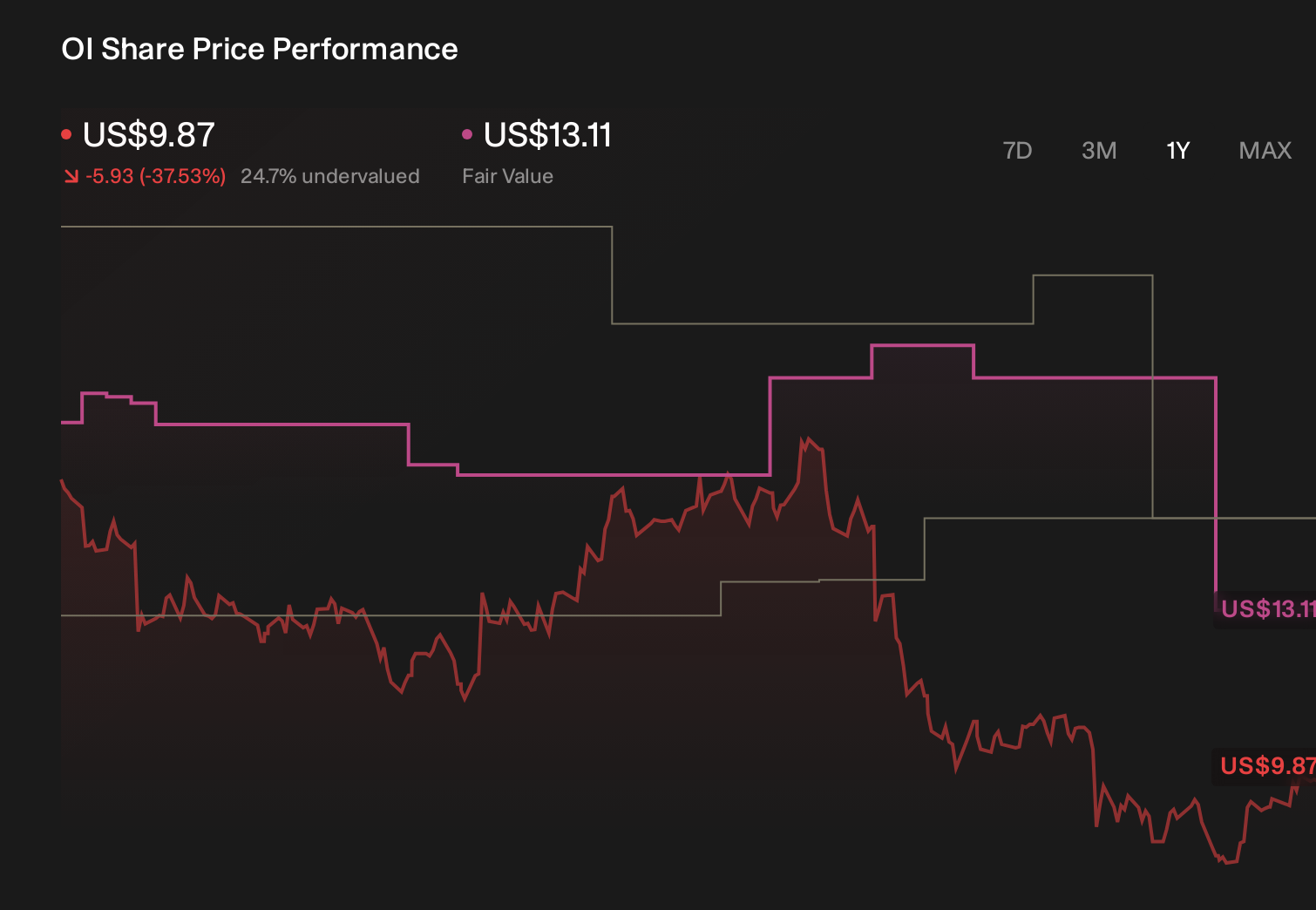

- In late April 2026, O-I Glass, Inc. reported first-quarter 2026 results showing sales of US$1,540 million, down from US$1,567 million a year earlier, and a wider net loss of US$73 million versus US$16 million, with basic and diluted loss per share from continuing operations both at US$0.48 compared to US$0.10 previously.

- This sharp increase in quarterly loss, despite only a modest sales decline, raises questions about cost pressures and profitability trends across O-I Glass's operations.

- With this weaker first-quarter profitability now on the table, we’ll assess how the enlarged net loss reshapes O-I Glass’s existing investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

O-I Glass Investment Narrative Recap

To own O-I Glass, you generally need to believe that cost savings, modernization and resilient demand for glass packaging can outweigh ongoing losses and heavy capital needs. The latest first quarter loss deepens concerns around near term profitability and cost inflation, so the key short term catalyst is whether margin initiatives can visibly slow these losses, while the biggest risk remains that rising costs and weak volumes keep the company stuck in the red.

One recent development that matters here is the continued share repurchase activity, with about 5.0 million shares bought back for roughly US$59.9 million under the May 2024 plan. Against widening losses, this raises sharper questions about capital allocation and balance sheet flexibility at a time when cost control and plant upgrades are central catalysts for any improvement in earnings quality.

Yet beneath the cost saving story lies a risk investors should be aware of around sustained production curtailments and delayed facility reconfigurations...

O-I Glass’ narrative projects $6.6 billion revenue and $380.4 million earnings by 2029.

Uncover how O-I Glass' forecasts yield a $17.89 fair value, a 99% upside to its current price.

Exploring Other Perspectives

The lowest estimate analysts took a more cautious view, even as they still expected earnings to swing from about US$255 million loss to US$407 million profit by 2028. Compared with the focus on Fit to Win savings, they stressed that high energy costs and tightening carbon rules could steadily erode margins, and the latest wider loss suggests both narratives may need another look.

Explore 3 other fair value estimates on O-I Glass - why the stock might be worth just $17.89!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your O-I Glass research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free O-I Glass research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate O-I Glass' overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.