How Investors May Respond To Range Resources (RRC) As Barclays Highlights Tighter Oil Fundamentals

Range Resources Corporation RRC | 0.00 |

- Earlier this week, Barclays reiterated its Equal Weight rating on Range Resources while updating its outlook to reflect tighter global oil market conditions and a softer near-term gas price view due to oversupply.

- The bank’s commentary links shrinking oil inventories, reduced OPEC spare capacity, and geopolitical risks to a potential re-rating for exploration and production companies such as Range Resources once regional tensions ease.

- We’ll now explore how Barclays’ emphasis on tighter oil fundamentals and possible sector re-rating might influence Range Resources’ existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Range Resources Investment Narrative Recap

To own Range Resources, you need to believe that growing gas demand from data centers and LNG exports will outweigh regulatory, ESG, and regional Appalachian constraints. Barclays’ tighter oil thesis and softer near term gas view do not materially change the key near term catalyst, which remains access to premium markets for gas and NGLs, or the biggest risk, which is infrastructure and permitting friction that could cap volumes and pressure realized prices.

The most relevant recent announcement here is Range’s Q1 2026 update, which combined strong operating metrics with continued capital returns. Management reported production of about 2.21 Bcfe per day, reaffirmed 2026 guidance of 2.35 to 2.40 Bcfe per day with liquids above 30 percent, and repurchased 800,000 shares in the quarter, all of which frame how any sector re rating tied to oil fundamentals could intersect with Range’s existing production and cash return plans.

But beneath that attractive production and buyback story, investors should also be aware of how tighter pipeline permitting and local oversupply risk could...

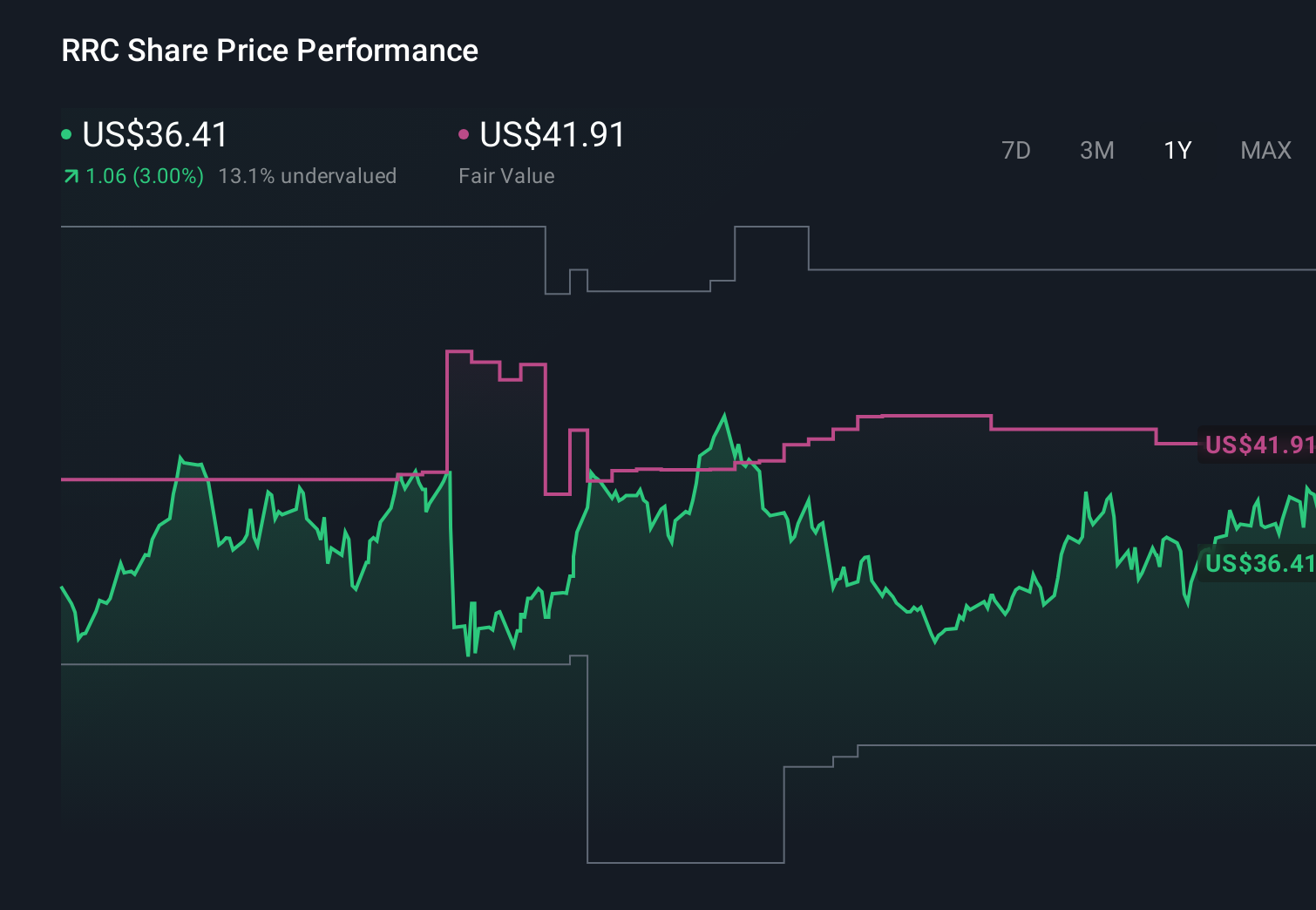

Range Resources' narrative projects $4.1 billion revenue and $804.1 million earnings by 2028. This requires 13.7% yearly revenue growth and roughly a $325 million earnings increase from $478.7 million today.

Uncover how Range Resources' forecasts yield a $42.17 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts take a far more cautious view, assuming earnings drift toward about US$796.0 million by 2029, so if you are weighing Barclays’ tighter oil thesis against this more pessimistic path for cash generation, it is worth recognizing how widely opinions can differ and how both scenarios might shift once this new information is fully reflected.

Explore 4 other fair value estimates on Range Resources - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Range Resources research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Range Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Range Resources' overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.