How Investors May Respond To Trinity Industries (TRN) $480.8 Million Green Railcar Securitization

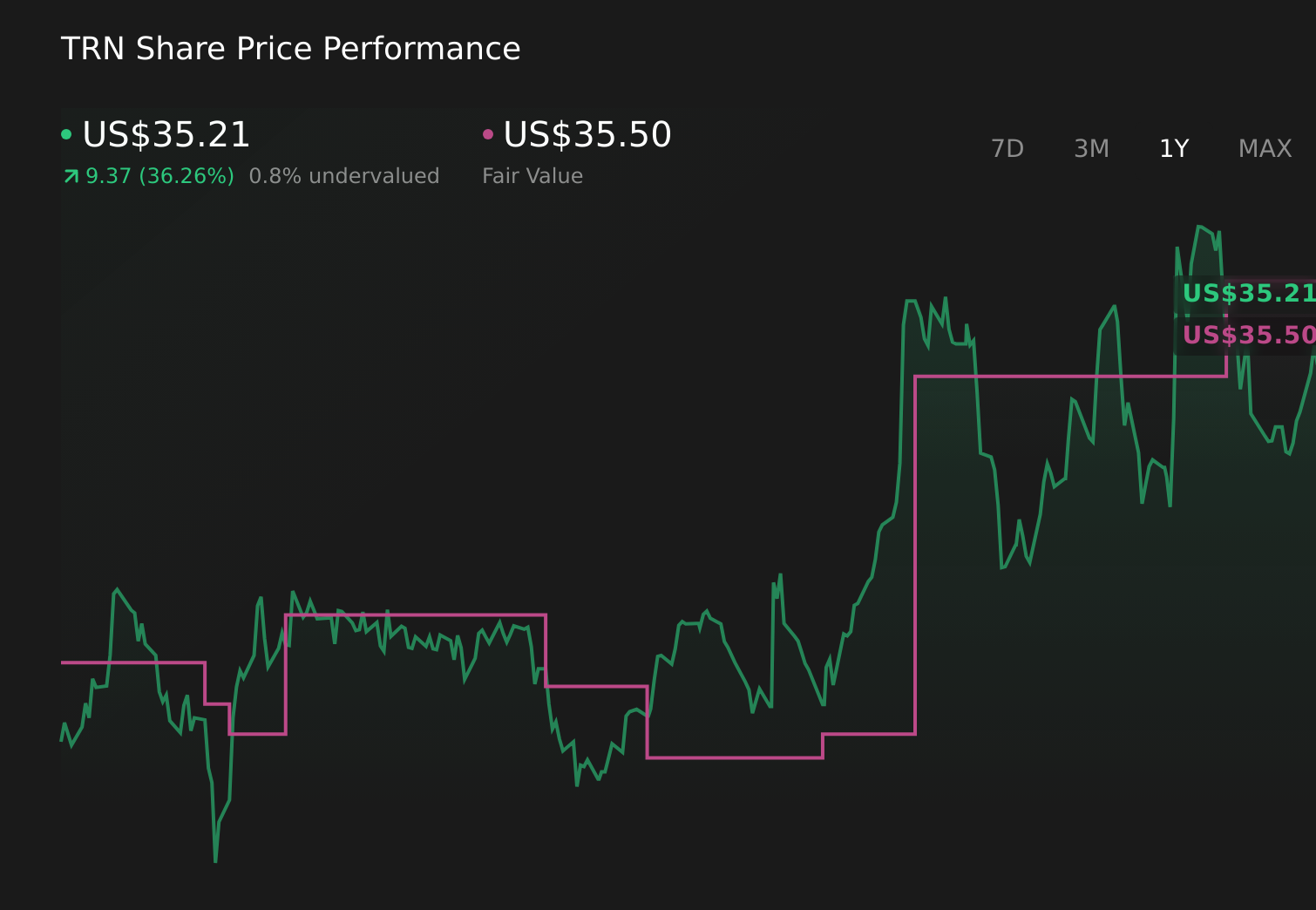

Trinity Industries, Inc. TRN | 34.45 | -0.43% |

- On April 1, 2026, Trinity Industries subsidiaries issued US$480.8 million of secured green railcar notes backed by about 15,082 leased railcars through an asset-backed securitization, reinforcing the company’s use of capital markets and green-labeled structures to finance its railcar leasing platform.

- This large green securitization not only recycles railcar assets and shifts funding needs to institutional investors, it also reinforces Trinity’s access to specialized capital aligned with environmental financing criteria.

- Next, we’ll examine how this sizable green asset-backed railcar issuance may influence Trinity’s investment narrative around capital efficiency and risk transfer.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Trinity Industries Investment Narrative Recap

To own Trinity Industries, you have to believe in the long term relevance of North American rail freight and Trinity’s ability to earn acceptable returns from its manufacturing and leasing platforms despite cyclical swings. The recent US$480.8 million green railcar securitization supports Trinity’s focus on capital efficiency and balance sheet flexibility, but it does not fundamentally change the near term catalyst around railcar demand recovery or the key risk from exposure to energy and agriculture cycles.

The most relevant near term announcement is Trinity’s plan to report first quarter 2026 results on April 30, 2026, when investors will get updated detail on leasing performance, railcar demand, and funding costs. Set alongside the new green asset backed issuance, that update should help clarify whether Trinity is turning its use of securitization into more resilient earnings and cash flows or relying more heavily on financial engineering at a time when end markets remain exposed.

Yet investors should also recognize the risk that Trinity’s rail dependent earnings remain tied to volatile end markets and evolving maintenance costs...

Trinity Industries' narrative projects $2.7 billion revenue and $141.3 million earnings by 2029. This requires 7.9% yearly revenue growth and a $119.0 million earnings decrease from $260.3 million today.

Uncover how Trinity Industries' forecasts yield a $33.50 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between US$33.50 and about US$35.71, underscoring how opinions can differ even in a narrow sample. Readers should weigh those views against Trinity’s reliance on cyclical end markets and consider how shifts in energy and agriculture demand could influence future performance before forming their own stance.

Explore 2 other fair value estimates on Trinity Industries - why the stock might be worth as much as $35.71!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Trinity Industries research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Trinity Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trinity Industries' overall financial health at a glance.

No Opportunity In Trinity Industries?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 62 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.