How Investors May Respond To Willis Towers Watson (WTW) Dividend Hike And New Digital Infrastructure Push

Willis Towers Watson WTW | 288.64 | +0.39% |

- In late February 2026, Willis Towers Watson reported fourth-quarter 2025 results that beat expectations, expanded operating margins, and approved a regular quarterly cash dividend of US$0.96 per share, a 4% increase from the prior quarter.

- Alongside these results, WTW created new leadership roles and launched a Global Digital Infrastructure Group, highlighting its push into specialized, cross-functional risk solutions for data center and digital infrastructure clients.

- Now we’ll examine how the dividend increase and launch of the Global Digital Infrastructure Group may influence Willis Towers Watson’s investment narrative.

AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to be comfortable with a consulting and broking business that is leaning into more complex risk advisory while managing pressure from technology, pricing and integration costs. The latest earnings beat and 4% dividend increase support the near term margin expansion story, but they do not significantly change the key risk that AI driven automation could compress fees across its core insurance and benefits services.

The launch of the Global Digital Infrastructure Group is the clearest link to WTW’s long term catalyst of growing demand for advanced risk management, especially around cyber, climate and digital infrastructure. By packaging cross functional expertise for data centers and hyperscalers, WTW is trying to anchor itself in higher value, less commoditized work, which may help offset competitive pressures from large peers and emerging technology platforms.

Yet despite these encouraging developments, investors still need to be aware of how accelerating AI adoption could...

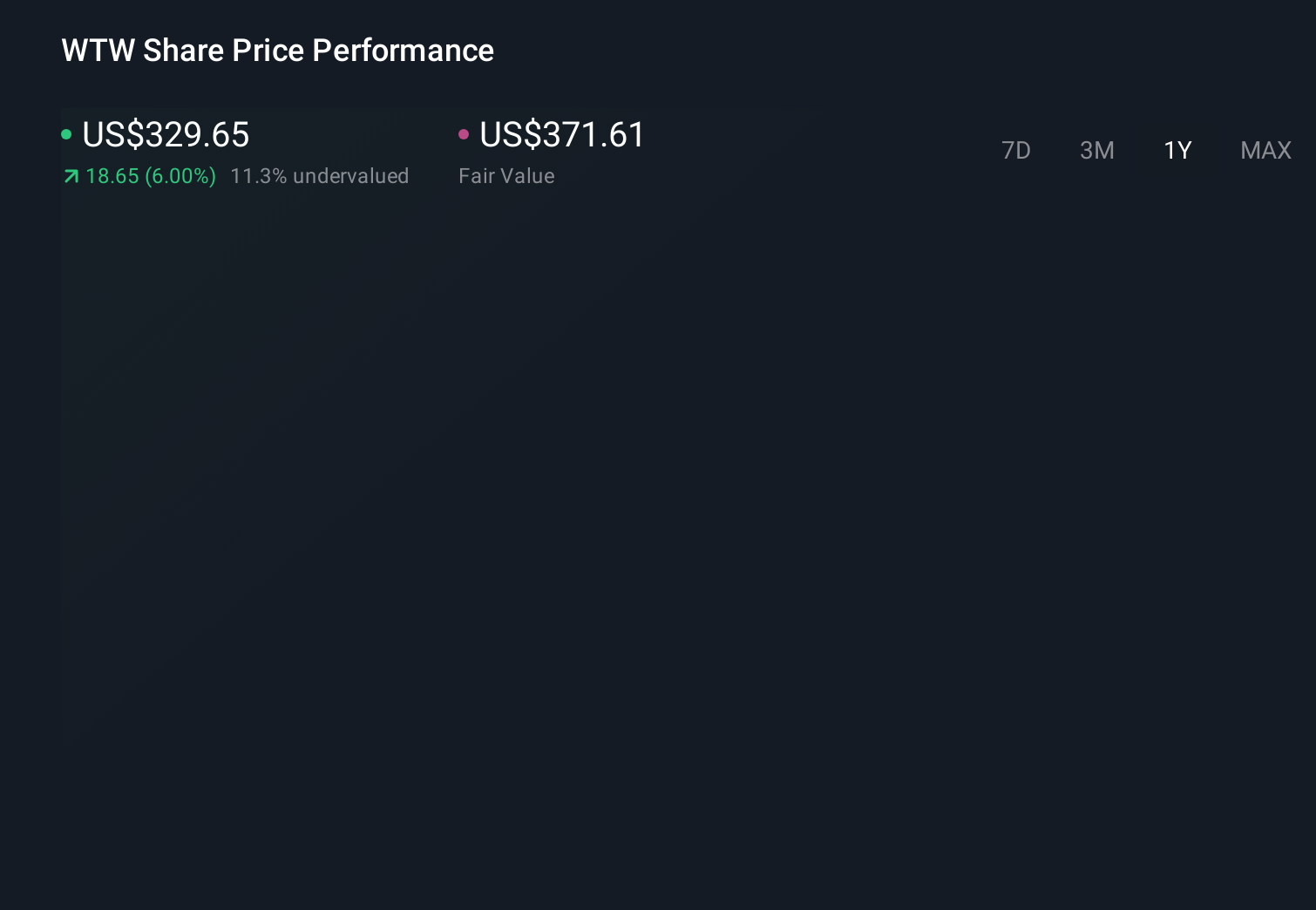

Willis Towers Watson's narrative projects $10.9 billion revenue and $2.5 billion earnings by 2028.

Uncover how Willis Towers Watson's forecasts yield a $372.00 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community range widely, from about US$187 to US$372 per share, showing how far apart individual views can be. You are seeing this divergence at a time when WTW is pushing into higher margin digital risk advisory through its new Global Digital Infrastructure Group, which could meaningfully influence how different investors think about its longer term earnings power and resilience.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth as much as 26% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.