How Investors May Respond To Woodward (WWD) Beating Guidance And Expanding With Aerospace Valve Deal

Woodward, Inc. WWD | 371.78 | -1.09% |

- Woodward recently reported strong first-quarter fiscal 2026 results that exceeded market expectations, while CEO Charles P. Blankenship sold about US$3.8 million of stock under a pre-arranged Rule 10b5-1 trading plan and shareholders re-elected three directors for new three-year terms.

- In addition, Woodward agreed to acquire Florida-based Valve Research & Manufacturing Company, adding high-precision aerospace flow control valves that expand its electromagnetic aerospace controls capabilities and support new commercial and defense applications.

- With these stronger-than-expected quarterly results and raised guidance now on the table, we’ll examine how they reshape Woodward’s investment narrative.

This technology could replace computers: discover 22 stocks that are working to make quantum computing a reality.

Woodward Investment Narrative Recap

To own Woodward, you need to believe it can convert its aerospace and industrial controls niche into durable earnings, even as technology and customer needs evolve. The biggest near term catalyst is management’s raised fiscal 2026 guidance, while a key risk is heavy capital and integration demands from new programs and acquisitions that could pressure margins and cash generation. The latest results, CEO share sale, and acquisition announcement do not materially change those core drivers, but they sharpen the focus on execution.

The planned purchase of Valve Research & Manufacturing looks most relevant here, because it directly ties into Woodward’s effort to deepen its aerospace controls portfolio at a time when guidance already reflects higher expectations. Folding VRM into the business could amplify both the upside from strong aero demand and the risk that integration and incremental investment weigh on free cash flow if benefits take longer to emerge than investors currently hope.

Yet beneath the upbeat guidance, investors should be aware that concentrated capex and acquisition integration could still...

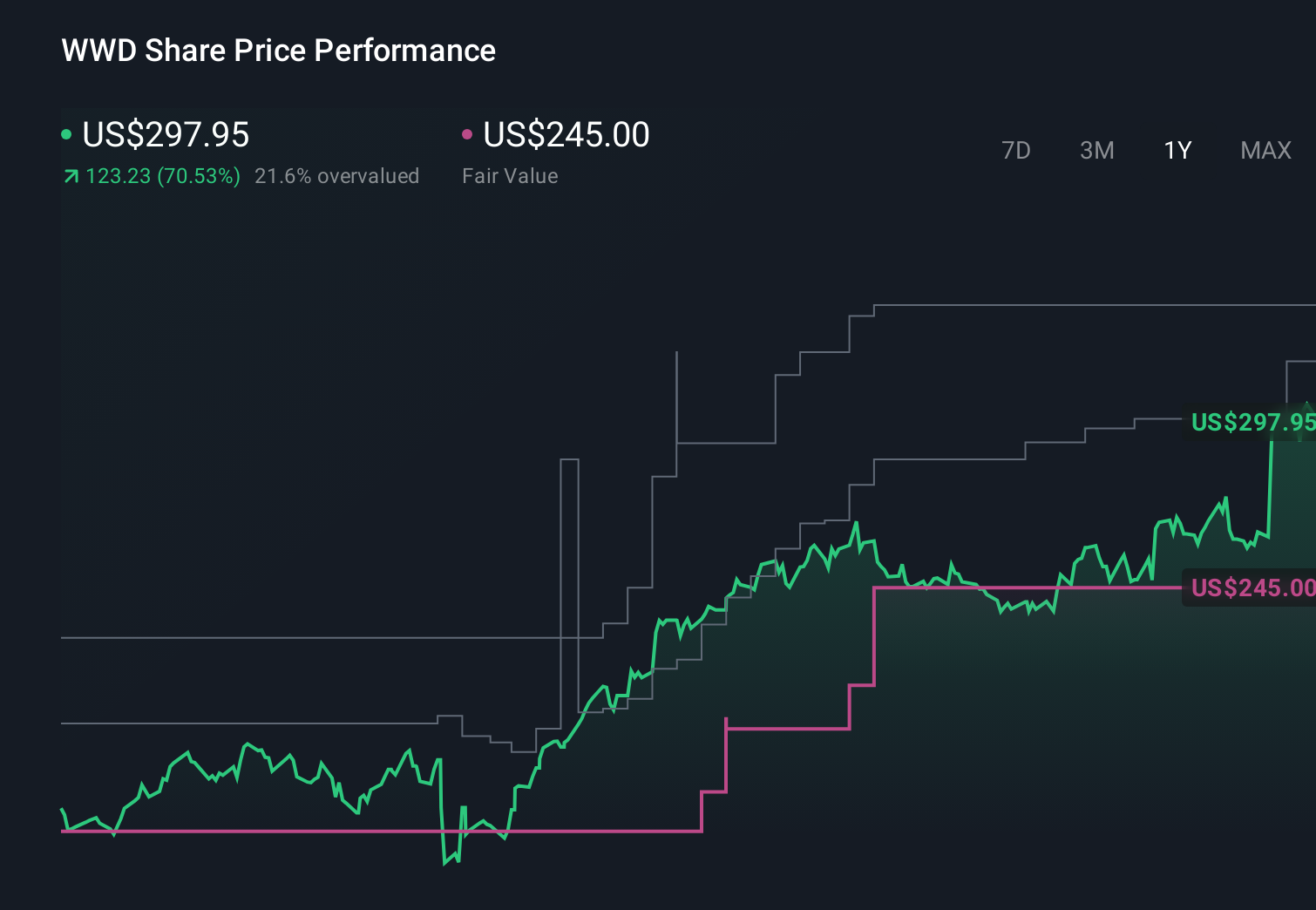

Woodward’s narrative projects $4.1 billion revenue and $561.5 million earnings by 2028. This requires 6.5% yearly revenue growth and about a $173.7 million earnings increase from $387.8 million today.

Uncover how Woodward's forecasts yield a $417.75 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some analysts were already much more optimistic, expecting revenue near US$4.5 billion and earnings around US$648 million by 2028, so this quarter’s strength and the VRM deal may either support that bullish view or prompt a rethink, depending on how you weigh the added growth potential against the risk of technological disruption and execution missteps.

Explore 7 other fair value estimates on Woodward - why the stock might be worth 33% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Woodward research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Woodward research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Woodward's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.