How New Singapore Airlines Partnership and Pricing Push Will Impact Southwest Airlines (LUV) Investors

Southwest Airlines Co. LUV | 0.00 |

- In early June 2026, Singapore Airlines announced a new interline partnership with Southwest Airlines, enabling single-ticket journeys that connect Singapore’s global network with Southwest’s nearly 120 U.S. destinations via Los Angeles, Seattle/Tacoma, and San Francisco, alongside Southwest’s recent expansion into five additional airports including Anchorage and St. Thomas.

- At the same time, Southwest’s Week of WOW promotion, offering discounted fares and bundled travel services, highlights how the airline is using pricing and partnerships to broaden its reach and attract both domestic and international travelers.

- We’ll now examine how Southwest’s new Singapore Airlines partnership could influence its investment narrative, particularly around revenue mix and route diversification.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

Southwest Airlines Investment Narrative Recap

To own Southwest, you need to believe its push to widen distribution and refresh the product can support earnings growth while managing costs and capacity risks. The Singapore Airlines tie-up broadens connectivity, but it does not materially change near term sensitivities around macro-driven demand, Boeing delivery timing, or fuel volatility, which still look like the key near term catalyst and risk pair for the stock.

The Singapore Airlines interline deal sits neatly alongside Southwest’s earlier Expedia partnership, which opened the door to new customer segments and booking channels. Together, these moves frame a catalyst around diversifying revenue sources and deepening loyalty economics without changing Southwest’s core domestic focus, giving investors a clearer line of sight on how partnerships might support the existing earnings and margin narrative.

Yet behind these positives, investors should also understand how Southwest’s concentration in the U.S. market could amplify the impact of any domestic travel slowdown...

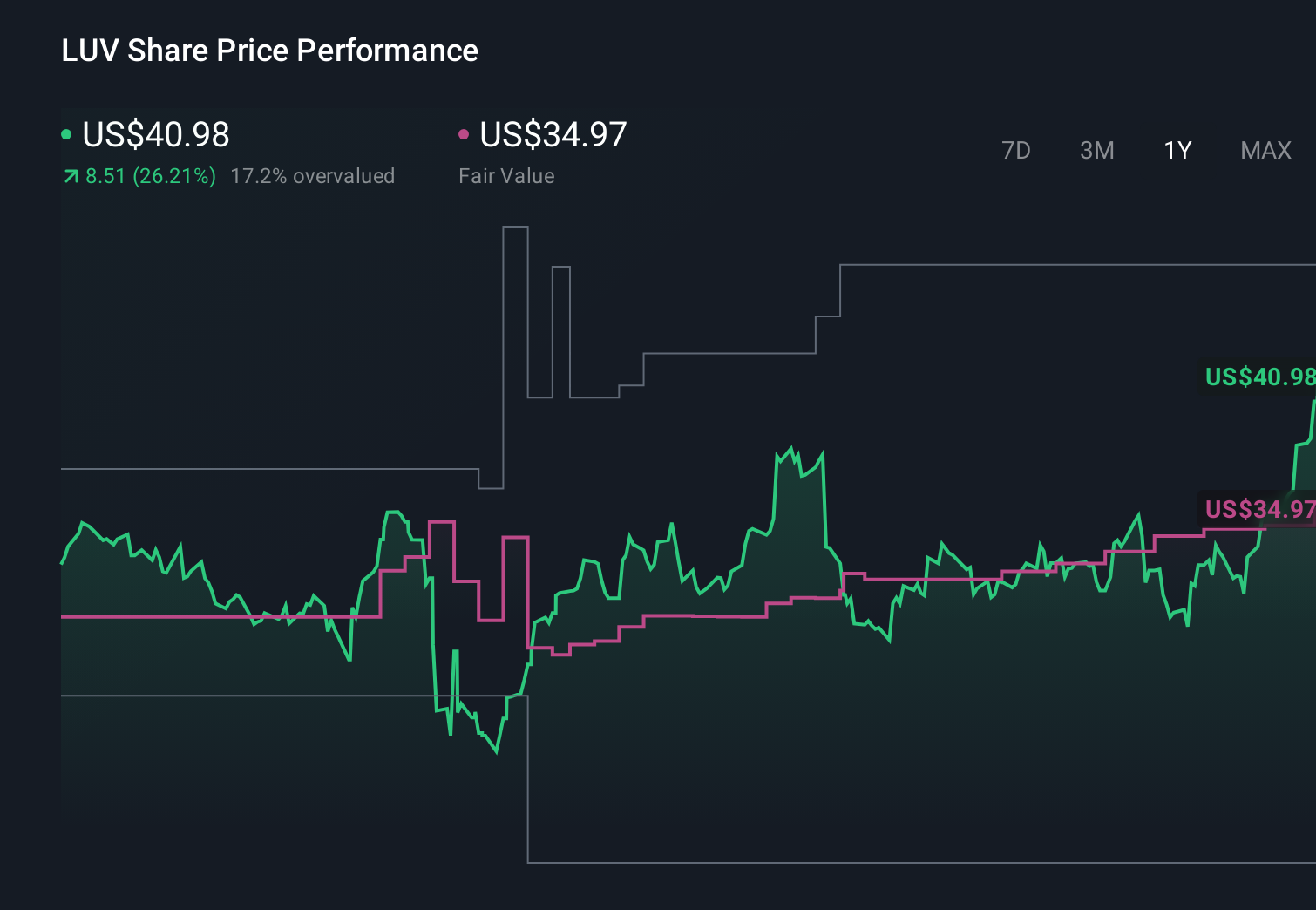

Southwest Airlines' narrative projects $34.6 billion revenue and $2.2 billion earnings by 2029. This requires 6.2% yearly revenue growth and about a $1.4 billion earnings increase from $817.0 million today.

Uncover how Southwest Airlines' forecasts yield a $45.64 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already saw bigger upside from Southwest’s expanding partnerships, with revenue reaching about US$36.6 billion and earnings near US$2.7 billion, while others worry that heavy domestic exposure could magnify any future shocks, so you should weigh how this new Singapore Airlines agreement might shift that wide range of views.

Explore 4 other fair value estimates on Southwest Airlines - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Southwest Airlines research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Southwest Airlines research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southwest Airlines' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.