How Permian’s Expanded Equity Plan and Share Shelf At Permian Resources (PR) Has Changed Its Investment Story

Permian Resources PR | 0.00 |

- In May 2026, Permian Resources Corporation filed a US$700.26 million shelf registration for 33,000,000 Class A common shares, following shareholder approval to expand its 2023 Long Term Incentive Plan share pool from 71,718,560 to 101,718,560 shares.

- This combination of a larger equity compensation pool and a substantial shelf registration highlights the company’s increased use of stock-based incentives and potential future share issuance for employees and related plans.

- We’ll now examine how this expanded equity incentive plan and related shelf registration could influence Permian Resources’ existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Permian Resources Investment Narrative Recap

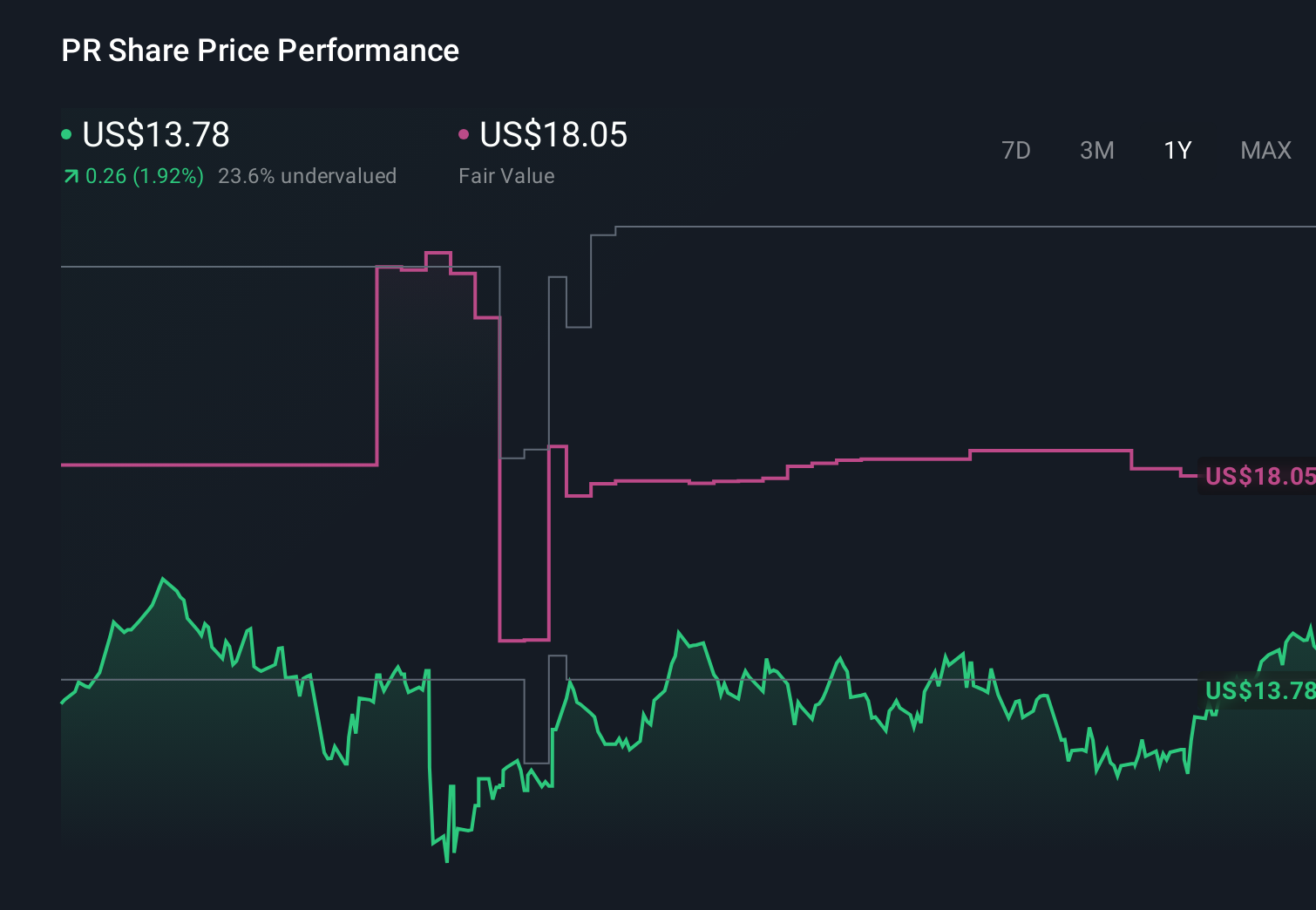

To own Permian Resources, you need to believe in its ability to keep growing production and cash generation from its Permian Basin footprint while managing commodity and regulatory uncertainty. The expanded equity incentive plan and US$700.26 million shelf registration do not materially change the near term operational catalyst around execution on drilling, costs and production guidance, but they do modestly increase the risk of future dilution for existing shareholders.

The shareholder approval to expand the 2023 Long Term Incentive Plan is most relevant here, because it directly connects to the new ESOP related shelf registration. Together, they point to heavier use of stock-based pay at a time when recent earnings have come under pressure and insider selling has picked up, which may matter for how you weigh short term valuation risk against the operational growth story.

Yet beneath the production growth story, investors should also be aware of the growing risk that continued equity issuance could...

Permian Resources' narrative projects $6.4 billion revenue and $1.3 billion earnings by 2029. This requires 7.9% yearly revenue growth and an earnings increase of about $0.4 billion from $935.2 million.

Uncover how Permian Resources' forecasts yield a $23.90 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were penciling in earnings of about US$1.8 billion by 2029, but if you worry more about acquisition and inventory replacement risks than they do, this new equity overhang may feel very different to you.

Explore 5 other fair value estimates on Permian Resources - why the stock might be worth 9% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Permian Resources research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Permian Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Permian Resources' overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- Capitalize on the AI infrastructure supercycle with our selection of the 44 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.