How Raised 2026 Revenue Guidance and New Contracts At Seadrill (SDRL) Has Changed Its Investment Story

Seadrill Limited SDRL | 0.00 |

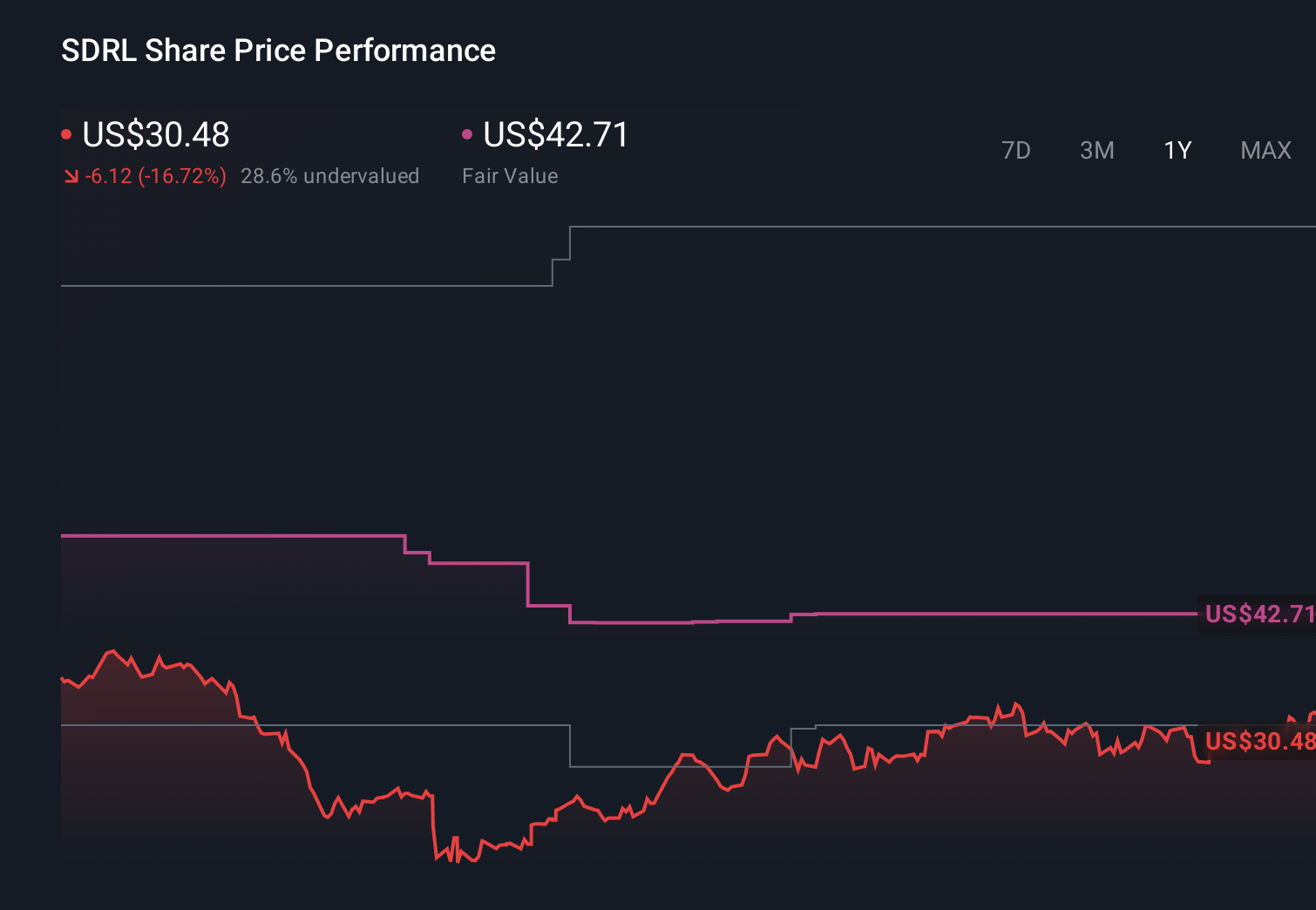

- In the past week, Seadrill Limited reported first-quarter 2026 results showing revenue of US$358 million, sales of US$285 million, and a narrowed net loss of US$7 million, while also lifting its full-year 2026 total operating revenue guidance to US$1.43 billion–US$1.48 billion.

- The company also highlighted more than US$860 million of new contract awards across key offshore basins and timely completion of major projects, which together point to a growing contract backlog and improving operational execution in a tighter deepwater rig market.

- We’ll now explore how Seadrill’s raised 2026 revenue guidance, underpinned by new contract awards, might influence its existing investment narrative.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Seadrill Investment Narrative Recap

To own Seadrill, you need to believe that tightening deepwater rig supply, high spec assets and a growing contract backlog can ultimately translate into sustainable profitability despite ongoing losses. The raised 2026 revenue guidance and US$860 million of new awards support the near term catalyst of stronger utilization and pricing, but they do not remove key risks around market softness, legal overhangs and the cost of aging or idle rigs.

The most relevant recent update here is the multi year West Polaris extension with Petrobras, adding about US$480 million to backlog at specified dayrates through early 2028. Together with the new awards highlighted in the first quarter release, this builds multi year visibility that directly ties into Seadrill's backlog driven catalyst, while also testing whether the company can manage utilization and margins in regions like Brazil where regulatory and legal risks have been an issue.

But even with improving guidance and backlog, investors still need to be aware of how unresolved legal claims and aging assets could...

Seadrill's narrative projects $1.7 billion revenue and $194.6 million earnings by 2029. This requires 6.8% yearly revenue growth and a $271.6 million earnings increase from -$77.0 million today.

Uncover how Seadrill's forecasts yield a $51.71 fair value, a 4% upside to its current price.

Exploring Other Perspectives

While the consensus view flags utilization and legal risks, the most optimistic analysts were already assuming revenue of around US$1.9 billion and earnings of about US$231 million by 2029, which shows just how far opinions can diverge and how this new guidance might shift expectations again.

Explore 6 other fair value estimates on Seadrill - why the stock might be worth 18% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

No Opportunity In Seadrill?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with 26 elite penny stocks that balance risk and reward.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.