How Slower Organic Growth and Margin Pressure in Q1 2026 Will Impact Willis Towers Watson (WTW) Investors

Willis Towers Watson WTW | 0.00 |

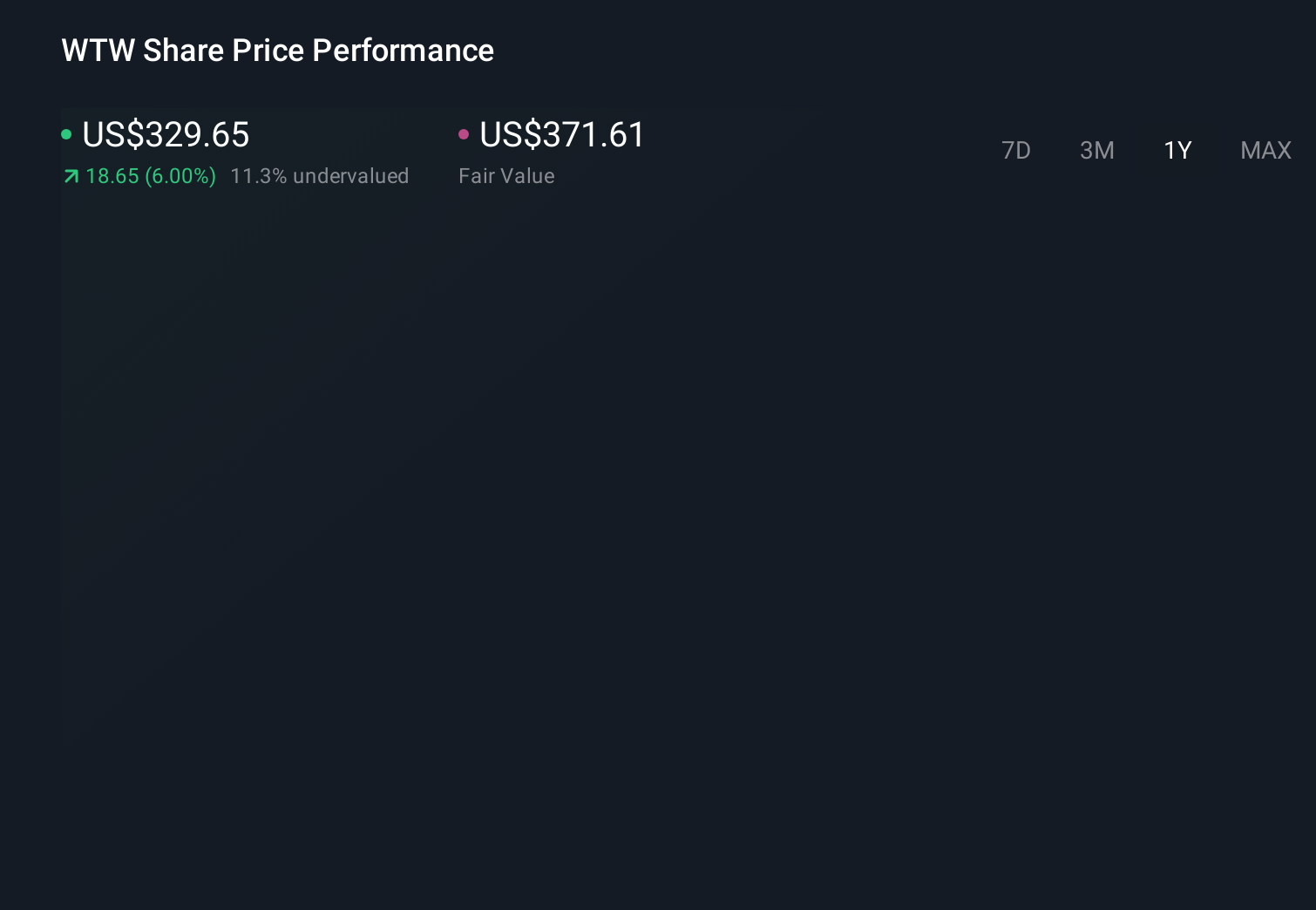

- Willis Towers Watson recently reported first-quarter 2026 results showing sales of US$2,412 million and net income of US$297 million, alongside leadership changes in North America and the release of its Political Risk Survey Report.

- Despite higher earnings per share, investors are focused on slower organic revenue growth, margin pressure, and client project deferrals that have attracted law firm investigations into potential securities issues.

- We’ll now examine how concerns over slower organic growth and margin pressure may influence Willis Towers Watson’s broader investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Willis Towers Watson Investment Narrative Recap

To stay invested in Willis Towers Watson, you need to believe in its ability to convert its global insurance broking and consulting footprint into steady revenue and earnings, even when client spending softens. The latest quarter delivered higher sales and net income, but the stock reaction shows the near term catalyst is confidence in organic growth and margins, while the biggest current risk is that client deferrals and margin pressure persist longer than expected.

The most relevant recent announcement is the law firm investigations triggered by slower organic revenue growth and margin compression following the first quarter results. These probes do not change the underlying business model, but they highlight how sensitive the share price is to any signs of weaker demand and execution at a time when analysts already expect only moderate earnings growth.

Yet investors should also be aware that slower organic growth, client deferrals and margin pressure could...

Willis Towers Watson's narrative projects $11.9 billion revenue and $1.8 billion earnings by 2029. This requires 6.9% yearly revenue growth and about a $0.2 billion earnings increase from $1.6 billion today.

Uncover how Willis Towers Watson's forecasts yield a $354.74 fair value, a 41% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community valuations for WTW cluster between US$354.74 and US$446.15 per share, showing how far private investor expectations can stretch. Set these views against the risk that slower organic growth and margin pressure, now under legal scrutiny, could weigh on how the market prices WTW’s execution in the coming years, and you may want to compare several different scenarios before deciding where you stand.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth just $354.74!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.