How Strong Q1 Results And Raised EBITDA Guidance At ATI (ATI) Has Changed Its Investment Story

ATI Inc. ATI | 0.00 |

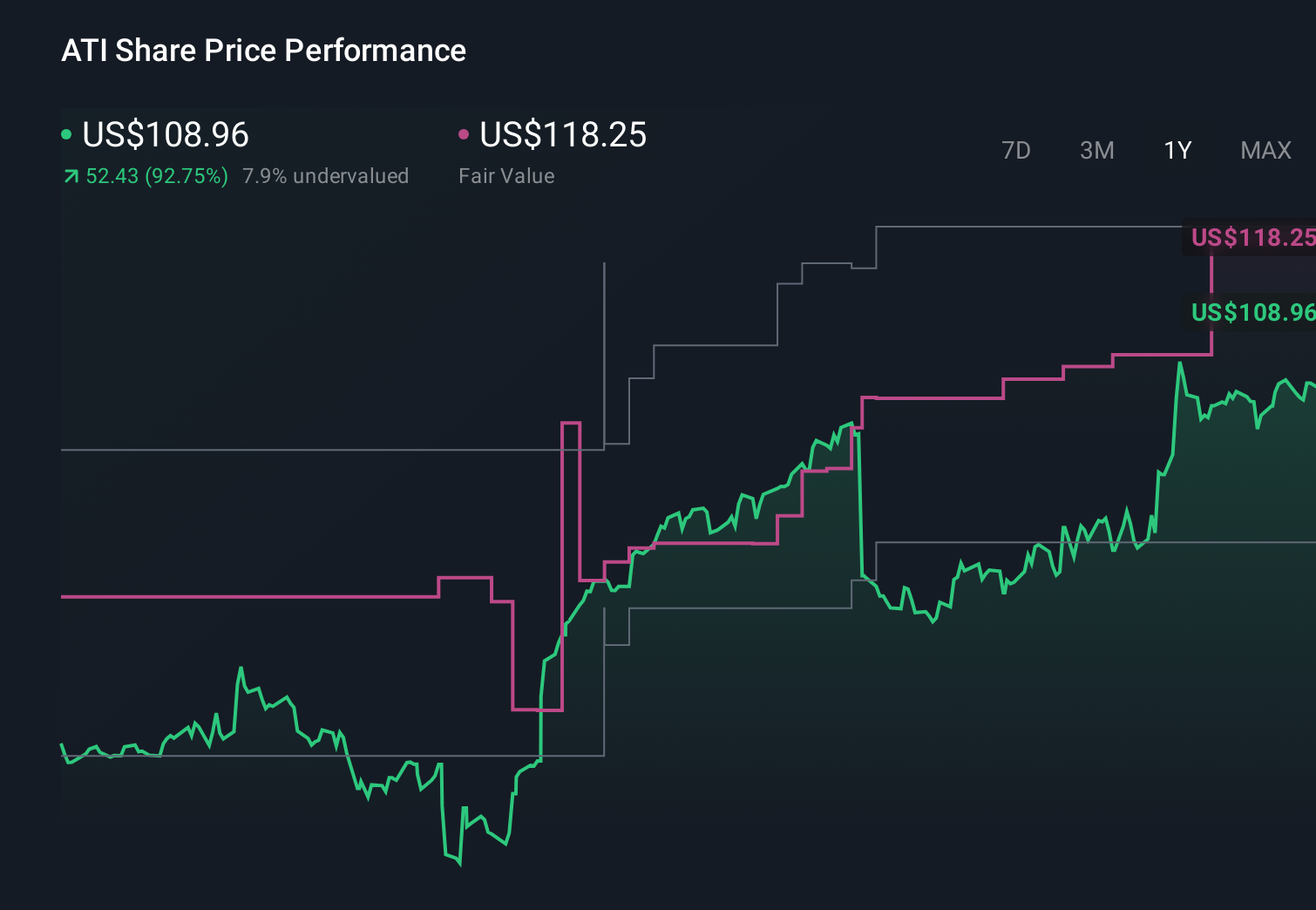

- In the first quarter of 2026, ATI Inc. reported sales of US$1,151.5 million, net income of US$118.2 million, and diluted earnings per share from continuing operations of US$0.85, all higher than a year earlier, and lifted its full-year adjusted EBITDA outlook while expanding its share repurchase authorization.

- ATI also reported a record US$4.10 billion backlog and renewed or signed multi‑year contracts in naval nuclear and specialty energy markets, reinforcing the earnings impact of its focus on higher‑margin aerospace, defense, and energy applications.

- Next, we’ll examine how ATI’s raised full-year adjusted EBITDA guidance influences the existing investment narrative built around aerospace and defense growth.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

ATI Investment Narrative Recap

To own ATI, you have to believe its pivot toward higher margin aerospace, defense, and specialty energy can offset softer industrial and medical exposure and ongoing capital intensity. The Q1 2026 beat, record US$4.10 billion backlog, and higher adjusted EBITDA outlook support that thesis and appear to strengthen the near term earnings and cash flow catalyst. The biggest risk still looks like concentration in a handful of major aerospace customers if their volumes or sourcing decisions change.

The company’s decision in early 2026 to boost its share repurchase authorization by US$500 million sits alongside the raised full year adjusted EBITDA guidance of about US$1.035 billion. Together with the renewed 5 year naval nuclear agreement and the US$250 million Cameco deal, this capital return move ties directly into the current catalyst: ATI leaning into higher quality aerospace, defense, and energy revenue while using excess cash to reshape its capital structure.

Yet while backlog is high and guidance is up, investors should still pay close attention to the risk that a few large aerospace OEMs account for so much of ATI’s future...

ATI’s narrative projects $5.9 billion revenue and $862.2 million earnings by 2029. This requires 8.8% yearly revenue growth and an earnings increase of about $436.7 million from $425.5 million today.

Uncover how ATI's forecasts yield a $178.67 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts saw ATI more cautiously, with revenue growing only about 4.3 percent annually and earnings reaching about US$612.9 million by 2028, which contrasts sharply with today’s stronger backlog and margin story and shows how differently you and other shareholders might weigh the risk that advanced composites slowly eat into ATI’s core alloy positions.

Explore 6 other fair value estimates on ATI - why the stock might be worth as much as 23% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ATI research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.