How Strong Q2 Results And New Acquisition At Woodward (WWD) Have Changed Its Investment Story

Woodward, Inc. WWD | 0.00 |

- Woodward, Inc. recently reported second-quarter 2026 results, with sales rising to US$1,090.57 million and net income reaching US$134.01 million, while also affirming a quarterly dividend of US$0.32 per share.

- Alongside these results, Woodward raised its full-year 2026 sales growth guidance and highlighted the acquisition of Valve Research & Manufacturing to strengthen its position in next-generation single-aisle aircraft systems.

- With Woodward lifting its 2026 sales growth guidance, we will now examine how this update reshapes the company’s existing investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Woodward Investment Narrative Recap

To own Woodward, you generally need to believe its aerospace and industrial control systems can stay relevant as platforms evolve, while capital-heavy growth projects and acquisitions still translate into healthy margins. The raised 2026 sales growth guidance and solid second quarter results reinforce the near term revenue story, but they do not remove the execution risk around integrating Valve Research & Manufacturing and delivering acceptable returns on recent manufacturing and M&A spending.

The most relevant recent announcement here is the upgraded 2026 sales growth guidance to 20%–23%, which directly ties to Woodward’s push into next generation aircraft systems, including the Valve Research & Manufacturing deal. This guidance increase sits alongside ongoing dividends and buybacks, underscoring management’s confidence in current momentum, but it also heightens investor focus on whether capital allocation into new programs and acquisitions can offset risks like supply chain pressures and shifting propulsion technologies.

Yet beneath the upbeat guidance, investors still need to consider how sensitive Woodward might be if major aerospace customers accelerate technology shifts and...

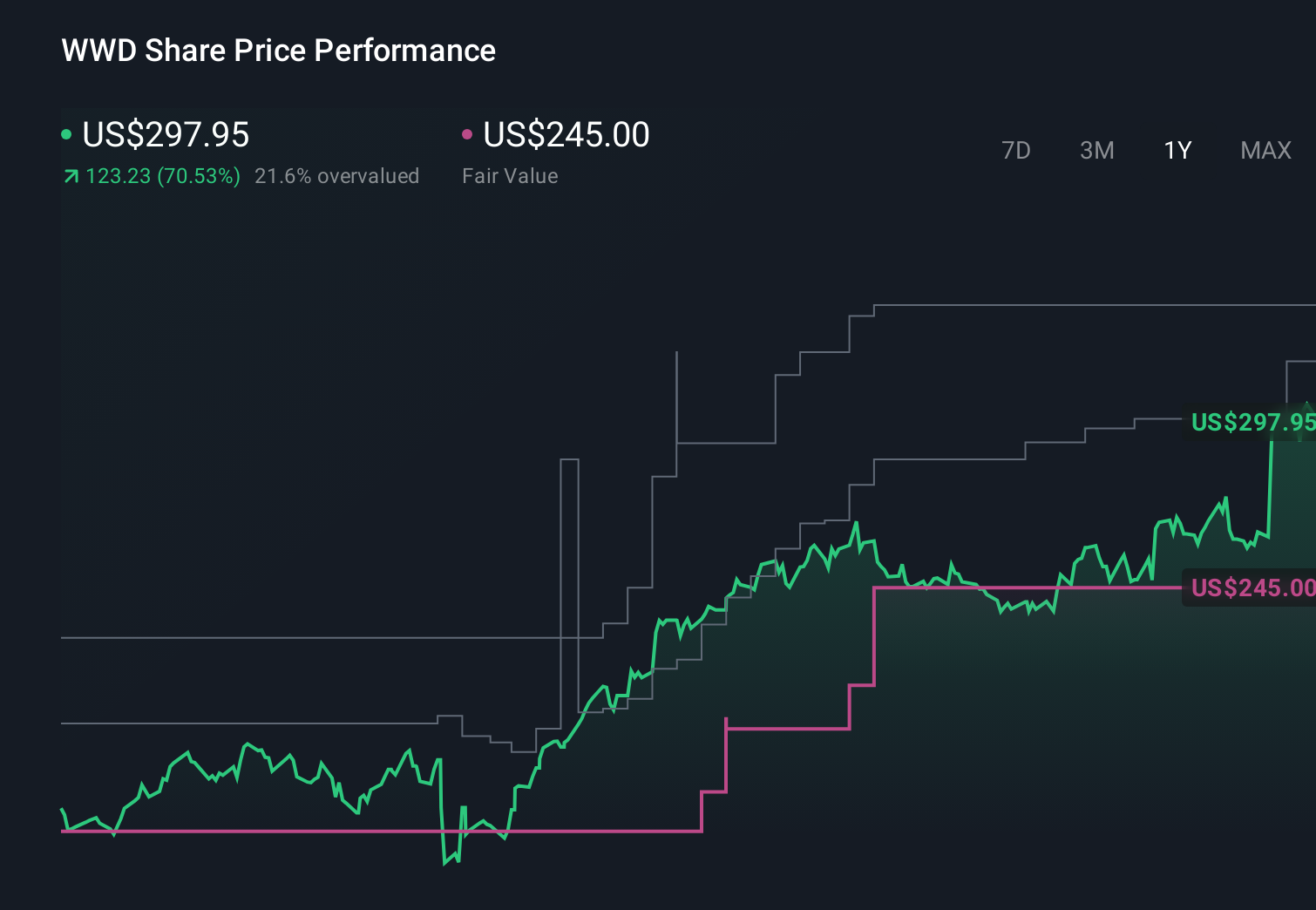

Woodward's narrative projects $4.9 billion revenue and $719.4 million earnings by 2029.

Uncover how Woodward's forecasts yield a $421.33 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already assuming about US$5.0 billion of revenue and US$724.2 million of earnings by 2029, yet you can see they frame Woodward far more pessimistically than consensus, particularly around customer concentration and technological change, and this new guidance and M&A activity may eventually push those expectations in a different direction.

Explore 6 other fair value estimates on Woodward - why the stock might be worth as much as 18% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Woodward research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Woodward research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Woodward's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 33 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.