How Stronger Backlog and Raised Guidance May Impact nVent Electric’s (NVT) Data Center‑Driven Story

nVent Electric plc NVT | 0.00 |

- In recent weeks, nVent Electric reported earnings that exceeded expectations, raised its multi‑year revenue growth guidance, and highlighted a much larger backlog supported by strong demand from data centers and power utilities.

- Analysts responded by reaffirming confidence in nVent’s earnings outlook, pointing to the company’s capacity expansion and investment in electrical and cooling solutions to meet infrastructure‑driven demand.

- Next, we’ll explore how this stronger guidance, underpinned by data center and utility demand, may influence nVent Electric’s existing investment narrative.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

nVent Electric Investment Narrative Recap

To own nVent Electric, you need to believe that electrification and data center buildouts can support sustained demand for its electrical and cooling solutions, and that management can execute on capacity expansion and acquisitions without eroding margins. The recent earnings beat and raised multi year revenue guidance reinforce the near term demand story, but they also heighten the key risk that a concentrated AI and utility backlog could reverse quickly if infrastructure spending cools.

Among recent announcements, the decision to authorize a new US$500,000,000 share repurchase plan sits squarely in this context. It signals that nVent is comfortable committing additional capital while it invests heavily in new facilities and higher CapEx to support data center and utility demand, effectively tying shareholder returns more closely to the same infrastructure cycle that underpins its upgraded multi year outlook.

Yet beneath the strong guidance, investors should be aware that concentration in AI led data center demand could quickly become a weakness if ...

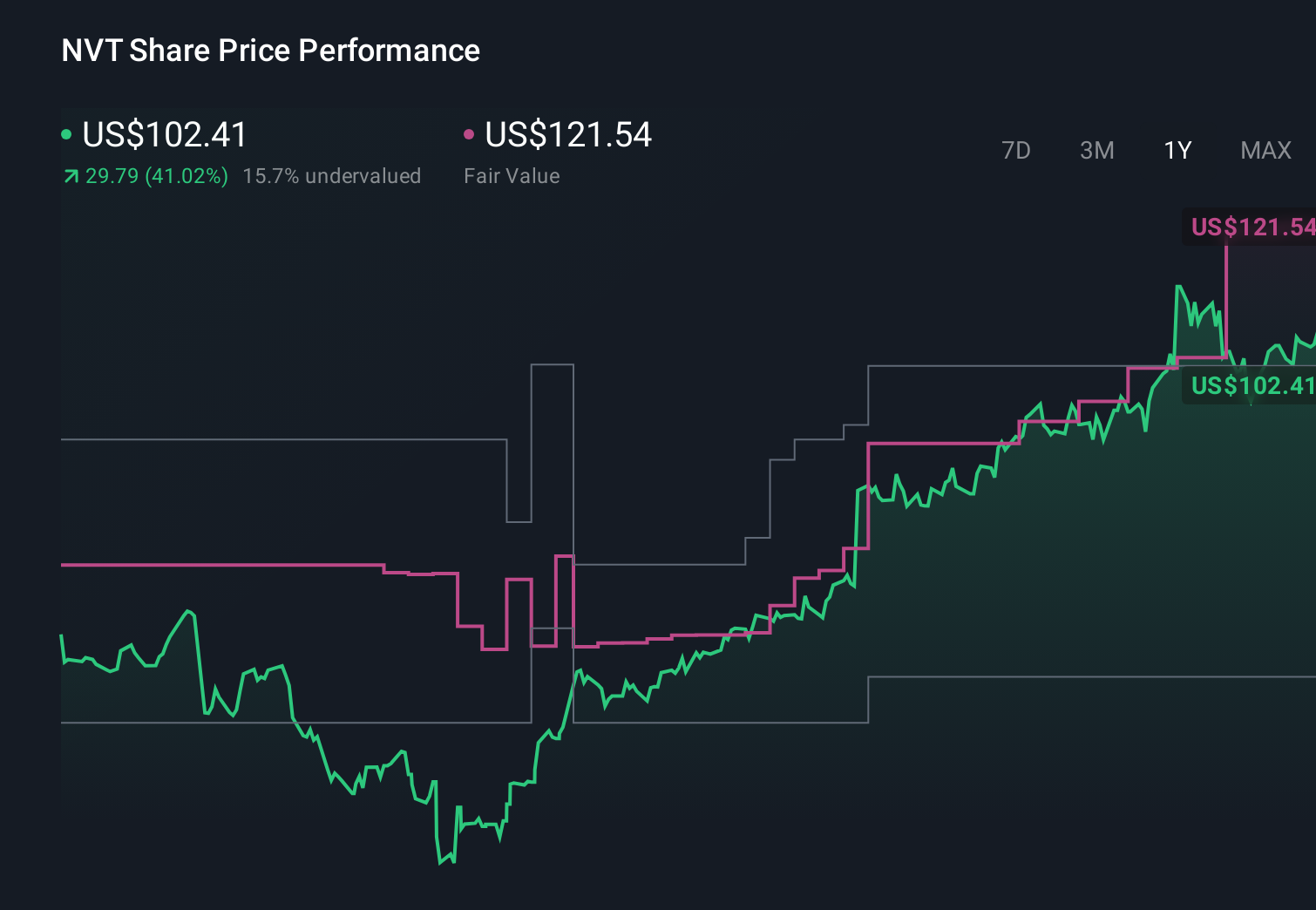

nVent Electric's narrative projects $6.5 billion revenue and $952.5 million earnings by 2029.

Uncover how nVent Electric's forecasts yield a $183.31 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much more cautious picture, assuming revenue of about US$5.8 billion and earnings near US$842 million by 2029, and warning that heavy reliance on AI and cloud cycles could still leave nVent exposed if those investment patterns shift, so it is worth comparing their view with more optimistic takes before deciding how this new guidance might reshape your own expectations.

Explore 5 other fair value estimates on nVent Electric - why the stock might be worth 40% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your nVent Electric research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free nVent Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nVent Electric's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.