How Stronger Q1 Results and UConn Partnership Could Shape Hartford (HIG) Investors’ Risk Narrative

Hartford Insurance Group, Inc. HIG | 0.00 |

- The Hartford Insurance Group, Inc. reported past first-quarter 2026 results showing revenue of US$7,226 million and net income of US$856 million, both higher than a year earlier, with basic earnings per share from continuing operations rising to US$3.08.

- A recent collaboration between The Hartford and the University of Connecticut on energy innovation and extreme heat research underscores the insurer’s focus on emerging risks, worker safety and evolving insurance needs for data centers and new energy technologies.

- Next, we’ll examine how this stronger quarterly profitability, alongside the UConn research collaboration, may influence The Hartford’s existing investment narrative.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Hartford Insurance Group Investment Narrative Recap

To own The Hartford, you generally need to believe in its ability to convert disciplined underwriting, technology investment and careful risk selection into resilient earnings, despite exposure to catastrophe losses and regulatory constraints. The stronger Q1 2026 results reinforce the company’s earnings narrative in the near term, but they do not materially change the key short term swing factor, which remains the potential impact of elevated catastrophe losses on margins and capital flexibility.

The new collaboration with the University of Connecticut on extreme heat and energy innovation fits closely with The Hartford’s focus on emerging risks and complex commercial customers. By deepening its understanding of worker heat exposure and the energy needs of data centers, the company may be better positioned to refine pricing and risk selection in lines where competition and loss costs are key catalysts for performance.

Yet the real concern investors should be aware of is how quickly elevated catastrophe losses could...

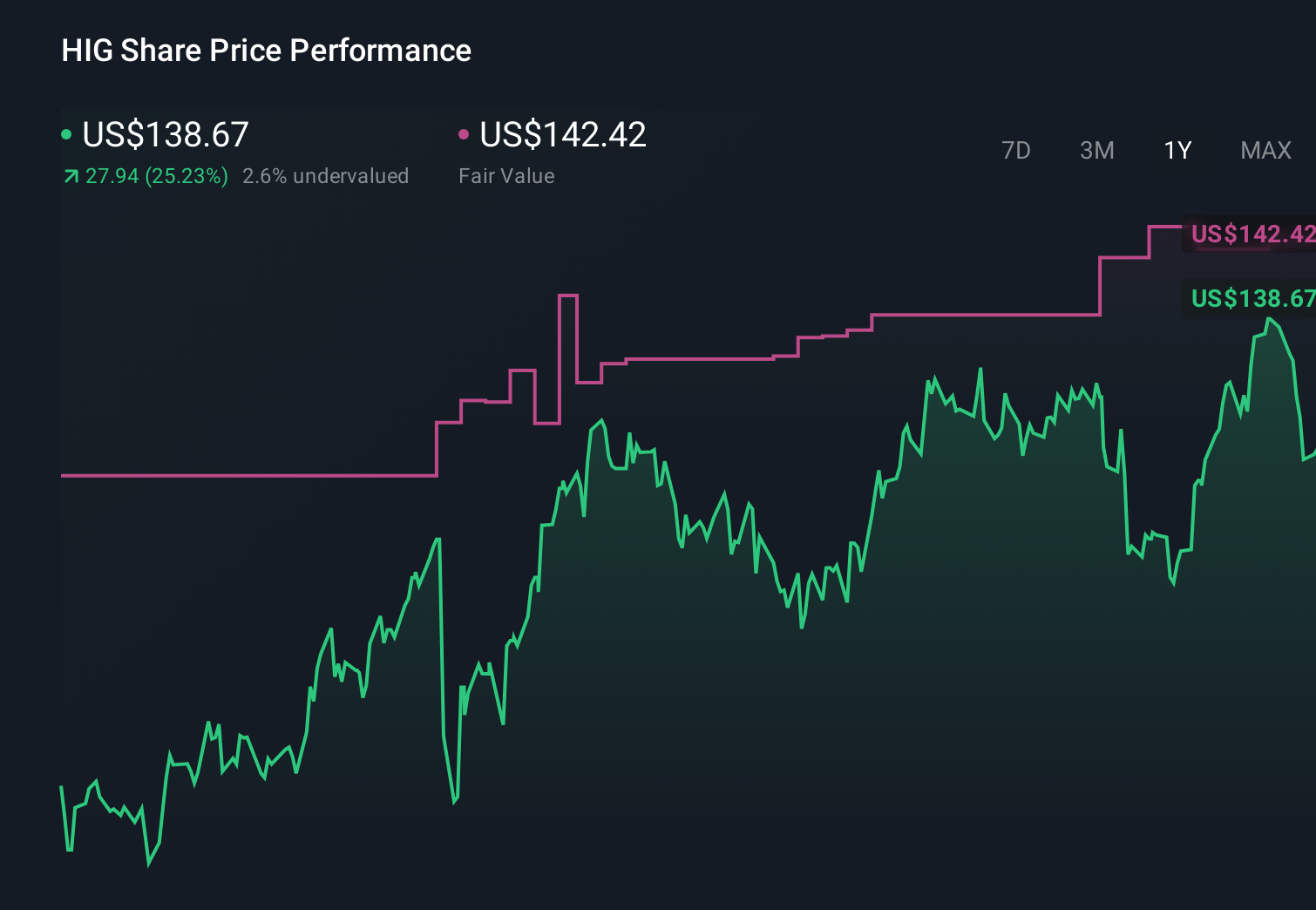

Hartford Insurance Group's narrative projects $32.1 billion revenue and $4.1 billion earnings by 2029. This requires 4.2% yearly revenue growth and about a $0.3 billion earnings increase from $3.8 billion today.

Uncover how Hartford Insurance Group's forecasts yield a $150.20 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently estimate The Hartford’s fair value between about US$141 and US$337, highlighting very different expectations. Set those views against The Hartford’s emphasis on technology and underwriting discipline, which many see as central to how its future performance could unfold.

Explore 4 other fair value estimates on Hartford Insurance Group - why the stock might be worth just $141.25!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hartford Insurance Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Hartford Insurance Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hartford Insurance Group's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.