How WTW’s New DFSA Licence in Dubai Will Impact Willis Towers Watson (WTW) Investors

Willis Towers Watson WTW | 0.00 |

- In early June 2026, WTW Investments (DIFC) Limited received approval from the Dubai Financial Services Authority to operate within the Dubai International Financial Centre, enabling the firm to locally provide its full range of regulated investment capabilities across expanding segments such as wealth management, family offices and workplace savings.

- This DFSA licence gives WTW a locally anchored platform in a major global financial hub, potentially deepening client relationships in the Middle East through on-the-ground advisory and fund access.

- Against this backdrop, we’ll examine how WTW’s new DFSA licence in Dubai could influence the company’s existing investment narrative.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe in its ability to grow fee-based broking and advisory income while managing technology, regulatory and competitive pressures. The new DFSA licence strengthens its on-the-ground presence in a key region but does not fundamentally change the near term focus on execution in core broking and wealth, or the risk that AI-enabled commoditization could pressure pricing over time.

Among recent developments, the launch of WTW’s AI Workforce Transformation solution is especially relevant. It shows the firm working to stay ahead of automation by embedding its own AI and data tools into client offerings, which could support its case for differentiated advice and help offset some of the pricing and fee compression concerns tied to broader AI adoption.

Yet beneath the expansion headlines, investors should still be watching how quickly AI could compress fees and dilute WTW’s differentiation...

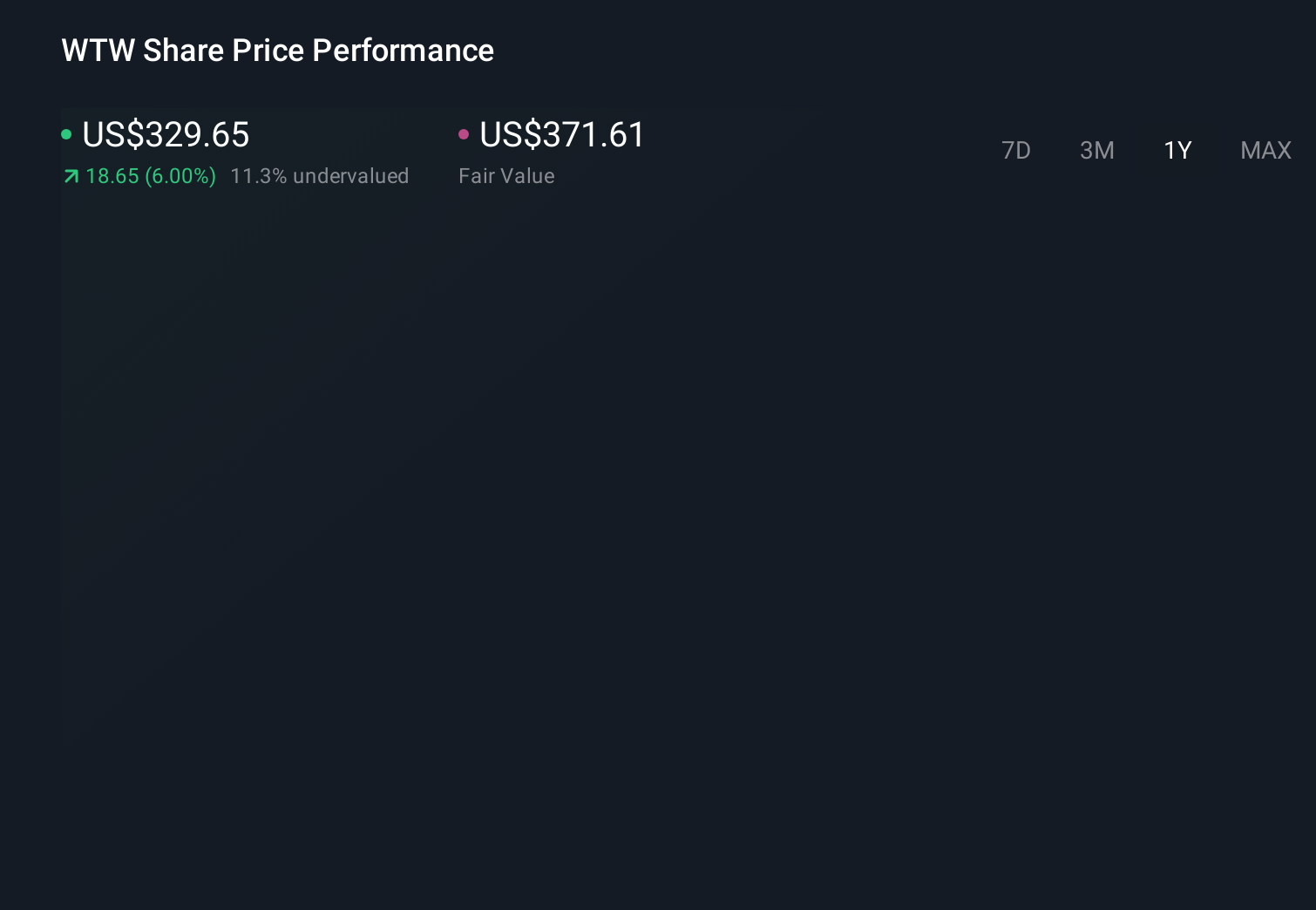

Willis Towers Watson's narrative projects $11.8 billion revenue and $1.9 billion earnings by 2029. This requires 6.1% yearly revenue growth and roughly a $0.2 billion earnings increase from $1.7 billion today.

Uncover how Willis Towers Watson's forecasts yield a $334.32 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$334 to US$446 per share, underscoring how far opinions can spread. As you weigh these views, remember that AI driven commoditization of broking and consulting remains a key issue for WTW’s long term pricing power and warrants comparing several alternative assumptions about the business.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth just $334.32!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

No Opportunity In Willis Towers Watson?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.