Hubbell (HUBB) Could Be 13% Undervalued As Russell Index Removal Hits Shares

Hubbell Incorporated HUBB | 0.00 |

Hubbell stock reaction to Russell index removal

Hubbell (HUBB) has come into focus after being dropped from the Russell 1000 Dynamic Index. This type of index change can trigger portfolio adjustments and affect short term trading activity in the stock.

The stock last closed at US$478.89, with the move around the index removal coinciding with a 3.4% decline over the past day and an 8.5% drop over the past week. Over the past month, the share price was roughly flat, while over the past 3 months it fell about 9.2%.

Beyond the index news, Hubbell’s recent share price weakness, including the 7 day decline of 8.5% and 3 month share price return of 9.2% down, contrasts with a 1 year total shareholder return of 17.5%. This suggests fading short term momentum against a still positive long term record.

If this kind of index driven volatility has you thinking about where else capital could work, it might be a good time to review 35 power grid technology and infrastructure stocks.

Hubbell now trades below the average analyst price target, but at a premium to some intrinsic estimates. The key issue is whether the recent index driven drop reflects overdone caution or justified restraint on valuation.

Most Popular Narrative: 13.1% Undervalued

Based on the most followed narrative, Hubbell’s fair value of $550.77 sits meaningfully above the last close of $478.89, putting the recent index driven weakness in a different light.

The analysts have a consensus price target of $550.77 for Hubbell based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $600.0, and the most bearish reporting a price target of just $479.0.

Want to see what is really driving that gap between price and fair value? The narrative hinges on a specific earnings path, margin profile and future valuation multiple that are anything but conservative.

The narrative framework uses a 10.07% discount rate, detailed revenue and earnings paths and explicit assumptions on future profit margins and share count to reach its $550.77 fair value. These inputs are all laid out in the full narrative for investors who want to pressure test whether Hubbell’s current Russell index noise lines up with those long term expectations.

Result: Fair Value of $550.77 (UNDERVALUED)

However, the Hubbell narrative could be knocked off course if tariff and raw material cost inflation squeeze margins, or if grid automation weakness persists longer than analysts expect.

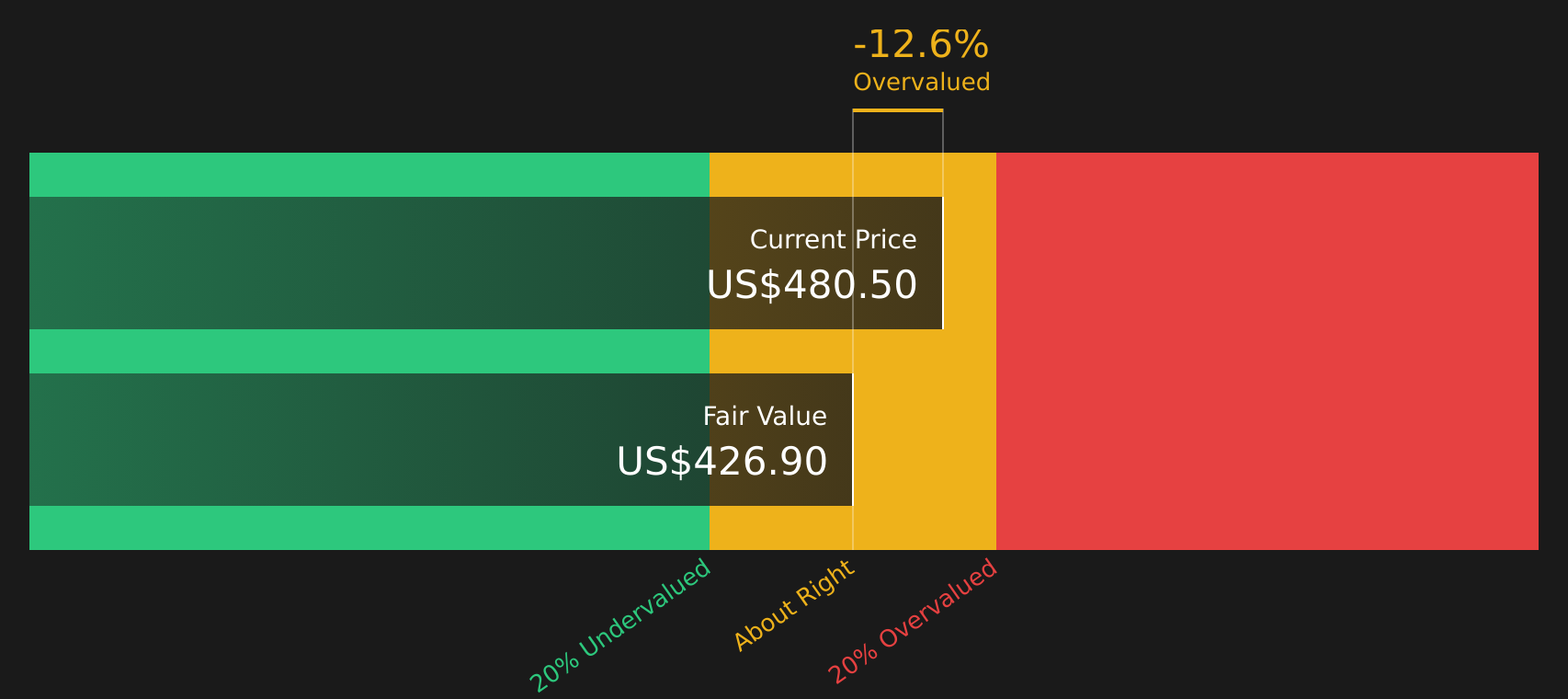

Another View: Hubbell Through a Cash Flow Lens

While analyst targets suggest Hubbell is undervalued, the SWS DCF model sends a cooler signal. On this approach, Hubbell at $478.89 trades above an estimated future cash flow value of $425.32, which points to an overvalued reading instead of a discount. Which story seems more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hubbell for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With the mix of concern and optimism around Hubbell in mind, move quickly to review the full picture and weigh both sides through the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Hubbell?

If you are reassessing Hubbell alongside other opportunities, now is the moment to line up fresh stock ideas before the next wave of market moves passes you by.

- Target dependable cash generators by scanning companies that show up in the solid balance sheet and fundamentals stocks screener (47 results) for stronger fundamentals and cleaner balance sheets.

- Hunt for potential bargains using the screener containing 18 high quality undiscovered gems so you are early to high quality businesses before they sit on everyone else's radar.

- Strengthen your long term income stream by reviewing the 9 dividend fortresses and focus on companies built around hefty, recurring payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.