Huntsman (HUN) Stock Valuation Check After Recent Rally And Conflicting Fair Value Estimates

Huntsman Corporation HUN | 0.00 |

Recent performance snapshot

Huntsman (HUN) has attracted fresh attention after a period of strong share price moves, with the stock up 4.4% on the day, about 11% over the past week, and roughly 15% over the past month.

Those gains come against a mixed fundamental picture, with revenue of US$5,693 million alongside a reported net loss of US$323 million, and a market value of about US$2.8b that reflects investor expectations for its specialty chemicals portfolio.

At a share price of US$15.74, Huntsman has seen strong short term momentum, with a 1-year total shareholder return of 51.02% contrasting with declining 3 and 5 year total shareholder returns of 28.95% and 25.55% respectively. This suggests sentiment has recently improved following a weaker longer term experience.

If Huntsman’s rebound has you looking for other opportunities in materials and related sectors, this may be a moment to scan 8 top copper producer stocks

With Huntsman shares rallying while the company reports a net loss and trades slightly above analyst price targets, it is worth asking whether the stock is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 10% Overvalued

Huntsman’s most followed narrative puts fair value at about $14.31 per share, compared with the recent close at $15.74, setting up a cautious valuation gap.

Demand for Huntsman's advanced materials and polyurethane-based products is expected to benefit from accelerating global trends in sustainability, energy efficiency, and lightweighting, especially as infrastructure and construction activity resumes, and the EV/clean tech markets expand. This supports potential for higher long-term revenue growth and greater market share.

Want to see what underpins that fair value call? The narrative leans heavily on revenue compounding, margin repair, and a future earnings multiple that sits well below sector norms.

Result: Fair Value of $14.31 (OVERVALUED)

However, the story could change quickly if prolonged overcapacity in polyurethanes or weak construction demand keeps pricing under pressure and delays any earnings recovery that investors are banking on.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

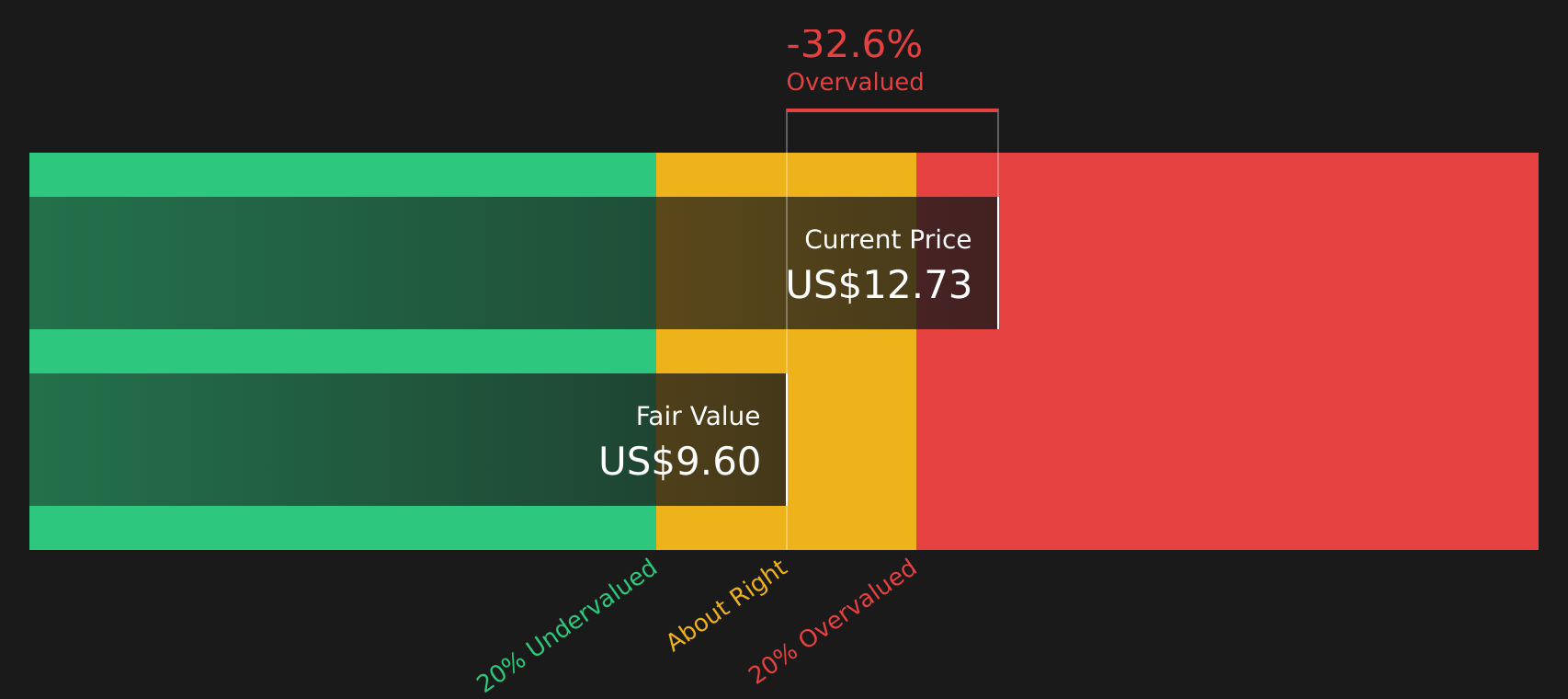

Another View: Cash Flows Paint A Different Picture

While the analyst narrative suggests Huntsman is about 10% overvalued versus a fair value of $14.31, the Simply Wall St DCF model is more conservative, putting fair value at $8.81. That implies the recent $15.74 price sits well above modeled future cash flows. This raises the question: which lens do you trust more?

Next Steps

With sentiment clearly split between recent share price strength and the underlying fundamentals, this is a moment to move quickly and test the data for yourself. To weigh up what the market might be getting right or wrong, it is worth starting with the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If Huntsman has sparked your interest, do not stop here, a broader watchlist can help you spot opportunities you might otherwise miss in today’s market.

- Target steadier compounding potential by scanning companies filtered as 70 resilient stocks with low risk scores, so you can focus on businesses with lower risk scores instead of chasing every sharp move.

- Hunt for quality at a reasonable price by checking screener containing 20 high quality undiscovered gems, where quieter stocks with solid fundamentals may be waiting for market attention.

- Build a more resilient core by reviewing solid balance sheet and fundamentals stocks screener (48 results), highlighting companies with stronger financial footing that can help anchor your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.