ICF International (ICFI) Margin Expansion Reinforces Bullish Valuation Narrative Despite Slower Growth Forecasts

ICF International, Inc. ICFI | 0.00 |

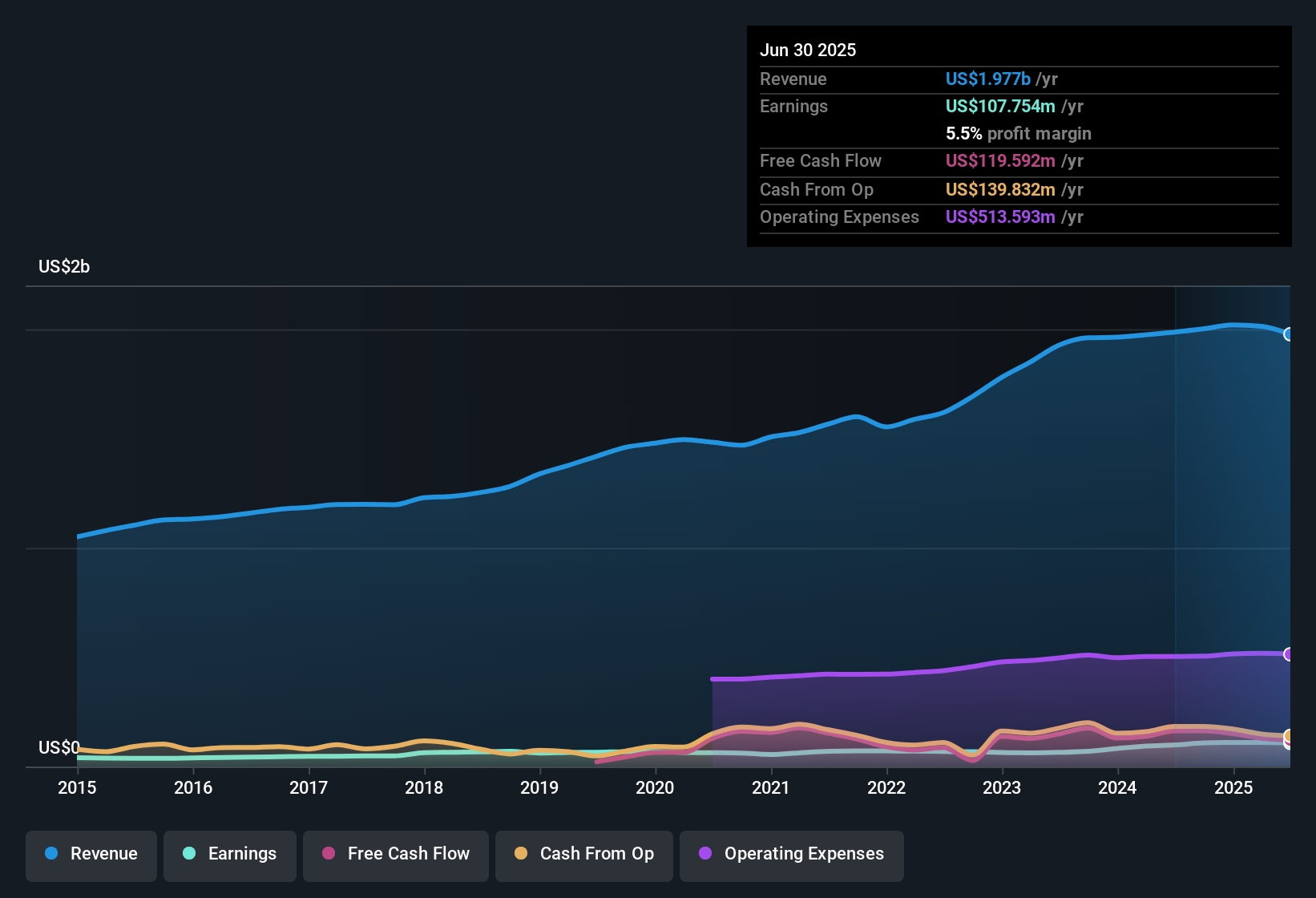

ICF International (ICFI) reported a net profit margin of 5.5%, up from 5% a year ago, with earnings expanding at a 13.8% annual pace over the past five years. Recent growth clocked in at 9%, which runs below its longer-term average. Analysts now expect annual earnings to rise 7.3%, with revenue growth projected at 2.8%, both trailing the broader US market. Despite more modest growth expectations, the company’s shares recently closed at $80.28, noticeably below an estimated fair value of $157.13, while profit margins and overall earnings quality remain solid.

See our full analysis for ICF International.The next section puts these headline numbers head-to-head with the market narratives, pinpointing where reality and expectations converge and where surprises emerge.

Margins Benefit from Higher-Margin Contracts

- ICF International’s net profit margin currently stands at 5.5%, reflecting not just margin expansion from last year but also a healthy mix of higher-margin commercial contracts now making up a greater share of revenue.

- Analysts' consensus view notes that demand for energy and IT modernization services is boosting high-margin contract wins and revenue stability.

- Wider margins and a ramp-up in international projects are working together to offset some uncertainties in the federal market.

- A disciplined focus on cost management and a larger allocation toward fixed-price and time-and-materials agreements is supporting this profitability trend, even as overall growth expectations moderate.

Want to know how analysts see the story playing out and where the biggest surprises might lie for ICF International? 📊 Read the full ICF International Consensus Narrative.

Growth Trends Slow but Remain Durable

- Earnings increased 9% recently, which is below ICF’s five-year growth average of 13.8%. Forward estimates project annual earnings growth of 7.3% and revenue growth of 2.8%, both trailing US market expectations.

- Consensus narrative highlights that while top-line growth is expected to lag the broader US market, recurring revenue streams from energy efficiency and modernization contracts continue to provide a stable foundation.

- A 25.2% year-over-year decline in federal contract revenues signals near-term pressure. However, sequential improvements in procurement activity and a strong book-to-bill ratio hint that backlog conversion may accelerate over the coming 12 to 24 months.

- The company’s investments in AI and fixed-price contract models, together with resilient commercial demand, are expected to help smooth out slower federal contract flows and keep earnings growth positive, albeit at a lower clip.

Attractive Valuation Compared to Peers and Fair Value

- ICF International’s price-to-earnings ratio of 13.7x stands well below peer averages (37.1x) and the wider US Professional Services industry (25.9x). Its share price of $80.28 trades at a significant discount to the estimated DCF fair value of $157.13.

- Analysts' consensus view points out that, despite modest earnings expectations, current valuation multiples and a consensus analyst price target of $101.75 suggest the market may be underestimating the company’s long-term earning power.

- The 12.2% upside to the consensus price target, paired with improving profit margins and earnings quality, stands out versus the declining outlook for many industry peers.

- This gap between today’s trading price, analyst targets, and DCF fair value could create opportunity if profit durability and cost discipline persist going forward.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for ICF International on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a fresh take on the numbers? Share your own perspective and shape the story in just a few minutes. Do it your way

A great starting point for your ICF International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

ICF International’s recent earnings growth has slowed and is expected to remain below broader market averages. This may indicate that future expansion could be less robust than hoped.

Seek out companies with stronger, reliable progress by using stable growth stocks screener (2103 results) that highlight consistent earnings and revenue growth, helping you sidestep potential slowdowns like this one.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.