Illinois Tool Works Stock And 3 Dividend Growers For Rate Hikes

Illinois Tool Works Inc. ITW | 0.00 |

With the Federal Reserve edging closer to a rate hike, dividend growth stocks are back in focus as investors reassess how reliable cash flows and disciplined payout policies might hold up if borrowing costs rise again. This article looks at three U.S. Dividend Growth Screener stocks that appear well positioned for this kind of backdrop, with a history of growing dividends and keeping payout ratios in check. All three are exposed to the current interest rate debate and inflation backdrop in ways that could matter for your portfolio, whether you prioritize income, stability, or a mix of both.

Illinois Tool Works (ITW)

Overview: Illinois Tool Works is a diversified industrial company that supplies specialized equipment, components, and consumables to markets ranging from automotive and construction to food service, welding, and electronics across multiple regions worldwide.

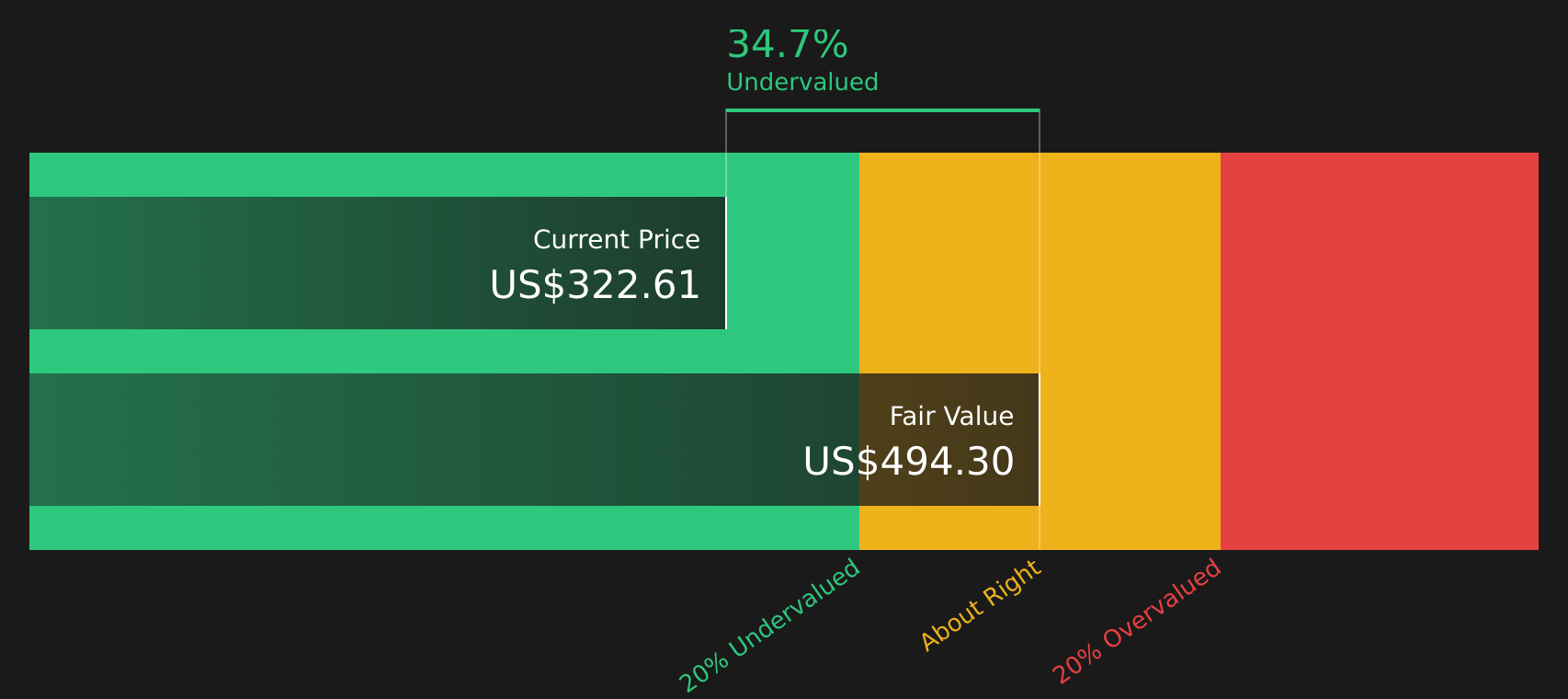

Operations: Illinois Tool Works generates most of its revenue from Automotive OEM (US$3.3b), Test & Measurement and Electronics (US$2.9b), Food Equipment (US$2.7b), Welding (US$1.9b), Construction Products (US$1.8b), Polymers & Fluids (US$1.8b), and Specialty Products (US$1.8b), with a small intersegment offset.

Market Cap: US$75.5b

Illinois Tool Works stands out in a potential rate hike setting because it pairs more than four decades of dividend growth with strong free cash flows and a broad industrial portfolio that touches autos, construction, and factory automation. The company is working on margin expansion through enterprise initiatives and tight cost control, while product launches like Miller Electric’s new Copilot welding solutions show it is still investing in its core franchises. At the same time, high debt, softer organic growth in some segments, and recent revenue and margin pressure mean investors cannot ignore balance sheet risk or the chance that slower demand and higher rates could bite. That mix of quality, income and real trade offs is what makes Illinois Tool Works worth a closer look.

Illinois Tool Works’ long dividend record and broad industrial reach can make it look like a simple quality story, but the real tension is how free cash flow stacks up against leverage and slower segments. This is why the 4 key rewards and 1 important warning sign could change how you see the balance between its strengths and the pressure points that might matter most next.

Carlisle Companies (CSL)

Overview: Carlisle Companies is a manufacturer of building envelope products, supplying roofing systems, insulation, waterproofing, and moisture protection solutions for commercial and residential buildings across the United States, Europe, North America, and other international markets.

Operations: Carlisle Companies generates most of its revenue from Carlisle Construction Materials at US$3.7b and Carlisle Weatherproofing Technologies at US$1.3b, with sales heavily concentrated in the United States at US$4.5b and smaller contributions from Europe and other regions.

Market Cap: US$14.3b

Investors watching how a potential Federal Reserve rate hike could affect building related stocks may find Carlisle Companies interesting because it sits at the center of commercial reroofing, energy efficient insulation, and weatherproofing solutions that many property owners view as non discretionary maintenance. The company combines a long history of dividend growth with solid cash generation, but pairs that with a high debt load and all liabilities coming from external borrowings, which raises funding risk if financing costs rise further. Earnings growth is expected to be modest and recent results showed lower revenue and net income, yet Carlisle trades below some estimates of fair value and maintains high reported returns on equity. This sets up a useful tension between quality cash flows, leverage, and what investors might be paying for that mix today.

Carlisle Companies looks like a rerating story in the making, with cash generation, dividends, and a P/E that some see as too low for its roofing and insulation footprint. Before you decide what that gap really means, go through the 3 key rewards and 1 important warning sign

Donaldson Company (DCI)

Overview: Donaldson Company is a filtration specialist that supplies air, liquid, and gas filtration systems and replacement parts for equipment used in construction, mining, agriculture, transportation, factories, data centers, and life sciences applications worldwide.

Operations: Donaldson Company generates most of its revenue from Mobile Solutions at US$2.4b, followed by Industrial Solutions at US$1.1b and Life Sciences at US$325.3m, with sales spread across the United States and Canada, EMEA, Asia Pacific, and Latin America.

Market Cap: US$10.0b

Donaldson Company is often categorized in the income and quality segment of the market, pairing a 38 year streak of dividend increases and a 1.47% yield with returns on equity around 25.9% and an improving net margin. Its filtration focus creates a large aftermarket that can support recurring cash flows, while acquisitions such as Facet Filtration expand exposure to higher margin aerospace and defense segments. At the same time, heavy reliance on legacy internal combustion engine filtration, sensitivity to raw material costs, and new debt facilities introduce risk if demand or input costs move against it in a higher rate environment. With a P/E below the Machinery industry average and analysts divided on potential upside, the full picture of how durable Donaldson’s growth and margins are can be more nuanced than headline numbers suggest.

Donaldson’s filtration cash engine and 38 year dividend streak suggest a sturdier story than many give it credit for, yet the real twist may lie in the gap between those cash flows and the analysis report for Donaldson Company

The three dividend growth stocks here are just a starting point. The full U.S. Dividend Growth Stocks screener surfaces 22 more large and mid cap U.S. companies that combine growing payouts with balanced cash flows and payout ratios. Use Simply Wall St to identify, filter, and analyze the specific catalysts and narratives that matter most to you so you can focus on the highest conviction dividend growth ideas.

Take Control of Your Investment Journey

If Illinois Tool Works or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Dividends?

Fresh stock ideas can move from quiet to breakout quicker than headlines catch up. Use these under the radar screeners now, before the crowd reacts, and look for opportunities to get in early.

- Spot under the radar strength by zeroing in on companies with resilient balance sheets using the curated list of solid balance sheet and fundamentals (48 results).

- Explore structural power grid momentum by scanning the infrastructure focused 34 power grid technology and infrastructure stocks.

- Track potential AI infrastructure candidates while they are still flying below broad indexes with the focused 48 AI infrastructure stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.