Ingersoll Rand (IR) Could Be 15% Undervalued As Earnings Near

Ingersoll Rand Inc. IR | 0.00 |

Ingersoll Rand (IR) is drawing attention ahead of its upcoming second quarter earnings release, with analysts expecting diluted earnings of $0.80 per share, compared with $0.77 in the same quarter last year.

Ingersoll Rand’s share price is US$78.85, with a 1-month share price return of 6.55% after a recent 1-day gain of 2.34%. The 1-year total shareholder return has declined 11.34%, while the 5-year total shareholder return is 64.64%, indicating that shorter term momentum has softened compared with longer term results.

If this earnings setup has you looking beyond Ingersoll Rand, it could be a good moment to check out 34 power grid technology and infrastructure stocks

After a strong recent bounce but a weaker 1-year return, Ingersoll Rand is trading below both analyst targets and one intrinsic value estimate. The key issue now is where fair value sits within that range.

Most Popular Narrative: 15.4% Undervalued

The most followed narrative puts Ingersoll Rand’s fair value at $93.20, compared with the last close at $78.85, framing the stock as trading at a discount before earnings.

The company continues building recurring, high-margin revenue streams through expansion of aftermarket services and value-added lifecycle solutions (aftermarket revenue grew to 37% of total), which increases the stability of net margins and supports long-term earnings resilience even if new equipment demand remains variable.

Want to understand why this narrative still supports a premium earnings multiple at a lower discount rate? The answer sits in the mix of steady revenue growth, a step change in margins, and fewer shares outstanding that all feed into that $93.20 fair value.

Result: Fair Value of $93.20 (UNDERVALUED)

However, Ingersoll Rand’s heavy use of acquisitions and exposure to shifting trade policies and tariffs could pressure margins and disrupt the earnings path behind that $93.20 fair value.

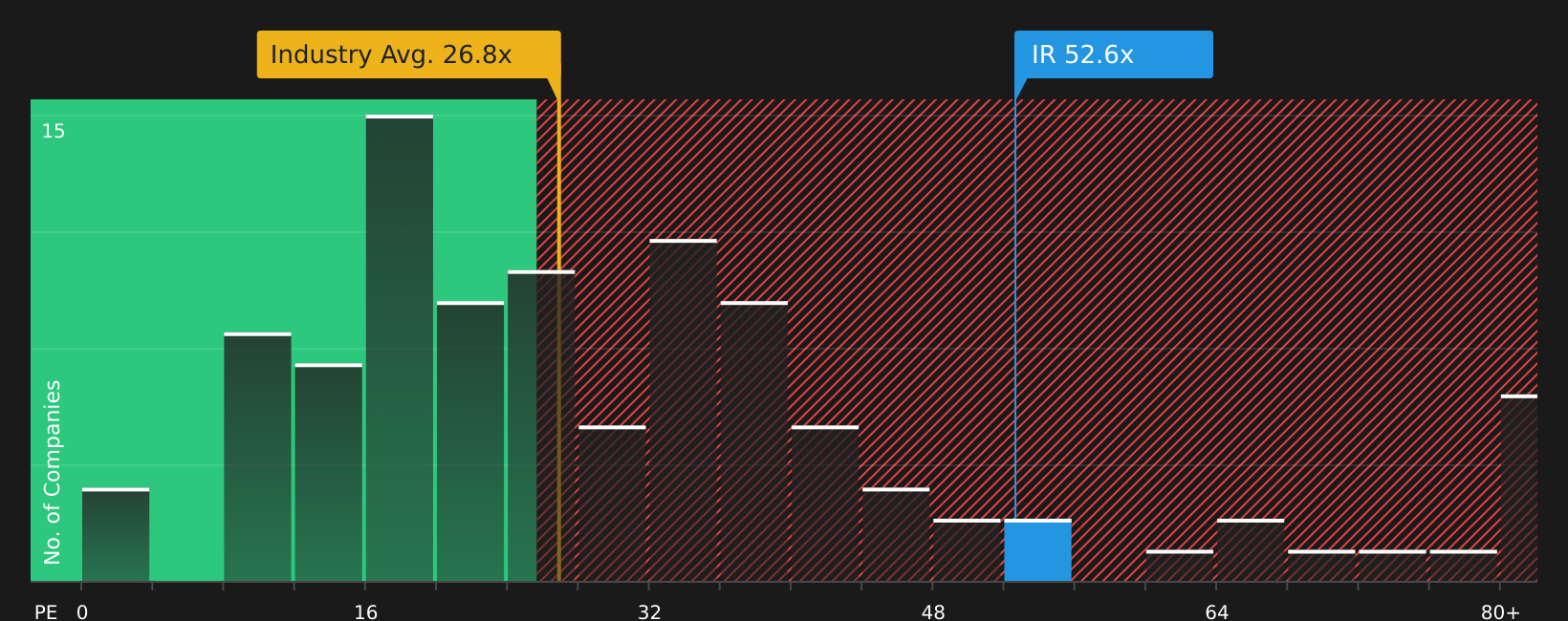

Another View: Ingersoll Rand Looks Expensive On P/E

That $93.20 fair value narrative uses detailed forecasts, but the P/E snapshot tells a tougher story. Ingersoll Rand trades on 52.6x earnings versus 26.8x for the US Machinery industry, 35x for peers, and a fair ratio of 38.4x, which points to clear valuation risk if sentiment cools.

For a closer look at how this pricing gap compares with what the numbers suggest the ratio could move toward, take a moment to See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With both optimism and caution running through this Ingersoll Rand story, take a moment to review the key charts, forecasts, and commentary yourself, then weigh the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Ingersoll Rand?

If Ingersoll Rand has you thinking more broadly about opportunities, do not stop here, fresh ideas in other areas could help round out your watchlist.

- Target high potential opportunities in smaller companies by scanning 20 elite penny stocks with strong financials that already show stronger financial underpinnings.

- Zero in on quality at a sensible price by reviewing the 45 high quality undervalued stocks that line up strong fundamentals with appealing valuations.

- Prioritize stability and capital strength by checking the solid balance sheet and fundamentals stocks screener (47 results) that combine resilient finances with sound business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.