Ingersoll Rand (IR) Stock Could Be 16.4% Undervalued After Strong First Quarter Results

Ingersoll Rand Inc. IR | 0.00 |

Recent attention on Ingersoll Rand (IR) follows its solid first quarter 2026 report, where revenue and orders grew and the book to bill ratio stayed above one for the full year since 2022.

Ingersoll Rand’s recent first quarter report and continued positive book to bill ratio seem to have supported a 9.87% 1 month share price return, even though the 1 year total shareholder return is slightly down and the 3 year figure remains clearly positive. This suggests that momentum has firmed up again after a softer patch.

If strong industrial order trends have caught your attention, it can be useful to see what else is moving in related areas and check out 31 robotics and automation stocks

With Ingersoll Rand’s shares rising over the past month while the 1-year return remains slightly negative, is the stock quietly undervalued after a pause, or is the market already pricing in the next phase of growth?

Most Popular Narrative: 16.4% Undervalued

Ingersoll Rand last closed at $77.91, compared with a widely followed narrative fair value of $93.20 that is built around earnings expansion and capital allocation.

The company continues building recurring, high-margin revenue streams through expansion of aftermarket services and value-added lifecycle solutions (aftermarket revenue grew to 37% of total), which increases the stability of net margins and supports long-term earnings resilience even if new equipment demand remains variable.

Want to see what sits behind that confidence in future cash generation and margins? The narrative focuses on compounding earnings, rising profitability and a richer mix of recurring revenue. Curious which specific assumptions pull that fair value up to $93.20 and keep the thesis intact even after a target trim?

Result: Fair Value of $93.20 (UNDERVALUED)

However, the Ingersoll Rand narrative could be challenged if acquisition integration issues lead to further impairments, or if prolonged tariff and trade uncertainty continues to delay customer orders.

Another View: Is Ingersoll Rand Already Pricing In Too Much?

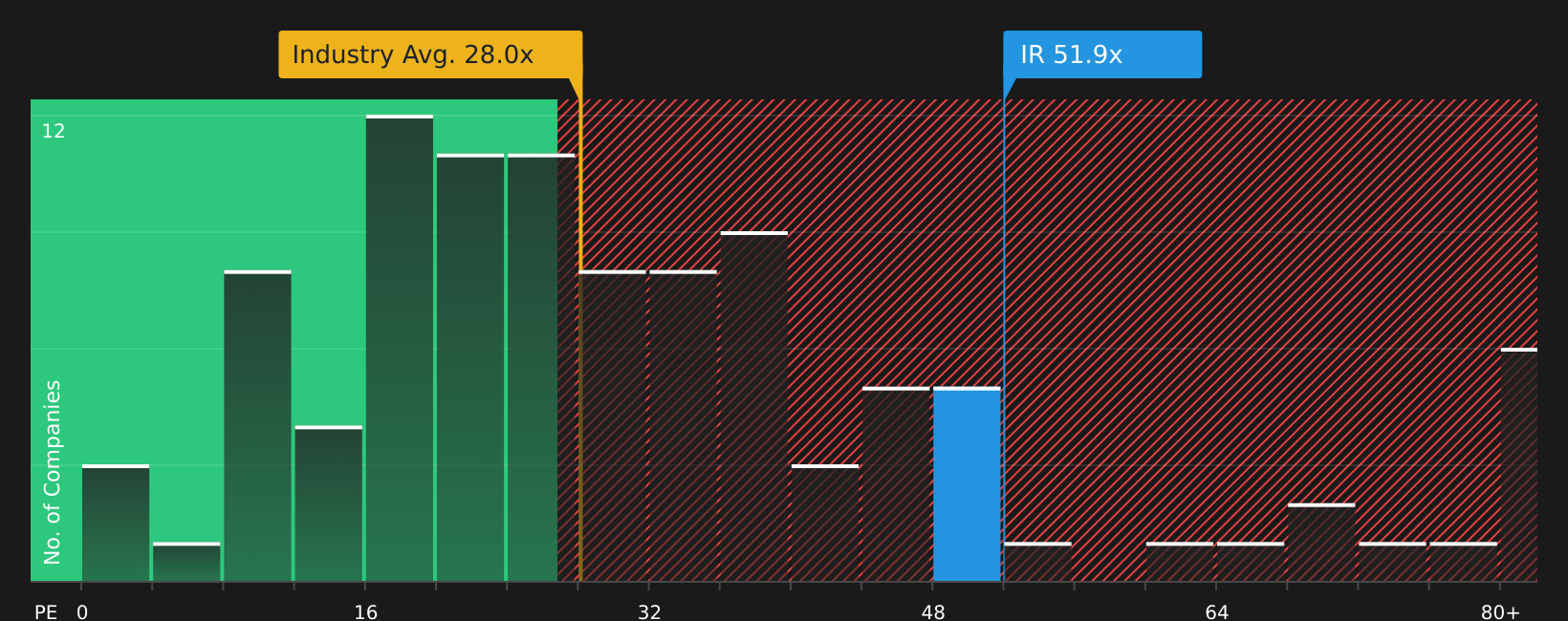

The narrative suggests Ingersoll Rand looks about 16.4% undervalued, yet the current P/E of 51.9x sits well above both the US Machinery industry at 28x and an estimated fair ratio of 36.6x. That gap points to meaningful valuation risk if sentiment or earnings expectations cool from here.

Before leaning on a single P/E driven story, it can help to see how that ratio could shift if earnings or sector sentiment change. It can also be useful to consider how much of today's price is tied to longer term optimism rather than current fundamentals, so it is worth weighing how comfortable you are with that premium.

Next Steps

With mixed signals around Ingersoll Rand’s recent momentum and valuation premium, why not move quickly to weigh the full picture of risks and rewards before opinions harden, starting with the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Ingersoll Rand?

Do not stop with Ingersoll Rand. Broaden your watchlist with targeted stock ideas built around quality, income and resilience using the Simply Wall Street Screener.

- Target consistent compounding opportunities by scanning companies that look attractively priced on fundamentals through the 45 high quality undervalued stocks.

- Strengthen your income stream by reviewing higher yielding opportunities using the 8 dividend fortresses.

- Focus on resilience and capital preservation by filtering companies with steadier profiles via the 65 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.