Ingersoll Rand (IR) Valuation Check After Recent Share Price Weakness

Ingersoll Rand Inc. IR | 0.00 |

Ingersoll Rand (IR) shares have faced recent pressure, with the stock down about 7% over the past month and about 23% over the past 3 months. This has prompted investors to reassess the company’s current valuation.

The recent weakness adds to a softer trend, with the share price down 12.15% year to date and the 1 year total shareholder return declining 14.34%. In contrast, the 3 and 5 year total shareholder returns of 12.10% and 47.81% highlight a more resilient longer term picture. This suggests that momentum has been fading in the short run despite healthier long run outcomes.

If this pullback has you reviewing other opportunities in industrial and infrastructure related themes, it could be a useful moment to scan 33 power grid technology and infrastructure stocks

So, with earnings and revenue still growing but recent returns turning weaker and the stock trading below some valuation estimates, should you view IR as temporarily out of favor, or are markets already pricing in all the future growth?

Most Popular Narrative: 40.1% Undervalued

At a last close of $70.07 against a fair value narrative of $117, the current price sits well below what this widely followed framework implies.

The bullish analysts are assuming Ingersoll Rand's revenue will grow by 6.7% annually over the next 3 years.

The bullish analysts assume that profit margins will increase from 11.6% today to 17.3% in 3 years time.

Want to see what kind of earnings profile those revenue and margin targets point to? The narrative leans on ambitious profit growth and a premium future P/E multiple that is reflected in the $117 fair value estimate.

Result: Fair Value of $117 (UNDERVALUED)

However, that upbeat fair value story can quickly crack if acquisitions underperform or expansion in regions like India and Latin America fails to deliver the expected uplift.

Another View On Valuation

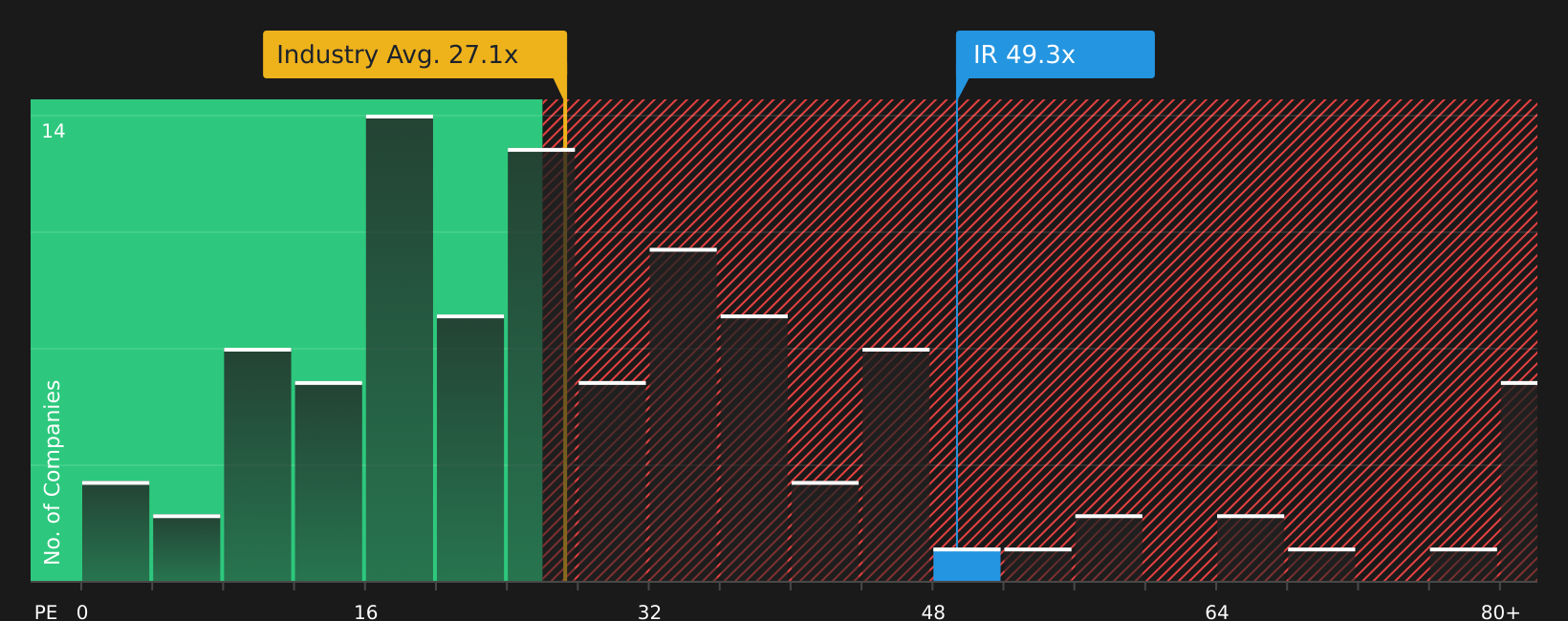

The bullish fair value narrative points to upside, but the current P/E of 46.7x tells a different story. That multiple sits well above the US Machinery industry at 27.5x, the peer average at 33.7x, and even the 35.9x fair ratio. This spread signals meaningful valuation risk if sentiment cools.

To see how those earnings multiples stack up in more detail, take a closer look at the valuation breakdown. This includes how the current P/E compares with the fair ratio and sector peers in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Does the mixed tone of this story match how you see IR right now, or not at all? Take a moment to weigh both sides by checking the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If IR does not quite fit your watchlist right now, use this moment of market reset to line up other stocks that better match your goals.

- Target potential upside by scanning 47 high quality undervalued stocks that pair compressed valuations with stronger fundamentals.

- Strengthen your income stream by reviewing 10 dividend fortresses that focus on higher yields with an emphasis on resilience.

- Build staying power into your portfolio by searching 63 resilient stocks with low risk scores that screen for more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.