Insperity Stock And 2 US Upskilling Plays Tied To AI Productivity

Udemy UDMY | 0.00 |

AI is rapidly reshaping how work gets done, with top adopters reporting productivity growth of 163% and turning that into both higher wages and more hiring. That shift is raising the bar for human skills, especially in roles that rely on judgment, leadership, and creativity, and it is forcing companies to rethink how they train and develop talent. For investors, that puts Human Capital Development & Training Providers under the spotlight, as their services sit close to this skills transformation story. This article looks at 3 stocks exposed to these AI driven trends and how the news may be influencing their investment case.

Insperity (NSP)

Overview: Insperity is a US based HR services company that helps small and mid sized businesses handle payroll, benefits, compliance, and workforce management, while also offering people focused solutions like talent acquisition, training, and performance management.

Operations: Insperity generates US$6.8b in revenue entirely from its HR Solutions segment in the United States.

Market Cap: US$1.4b

Insperity stands out in the Human Capital Development & Training space because it sits at the intersection of AI driven productivity and the rising need for better trained employees. Its HR360, HRCore, and HRScale offerings combine outsourced HR with tools that can support AI assisted workflows and workforce reskilling, and management is already talking about AI agents that act as copilots for clients. At the same time, investors need to weigh several pressure points, including healthcare cost inflation, current unprofitability, a high dividend that is not well covered, and heavy reliance on small and mid sized business clients. For investors who want to understand how this mix of AI opportunity, recurring HR revenue, and margin risk compares, there is more to unpack beneath the headlines.

Insperity’s AI assisted HR platform could be masking an even bigger story about how recurring HR revenue, healthcare cost pressure, and dividend coverage fit together, and the 3 key rewards and 1 important major warning sign hints at where that tension really sits

Udemy (UDMY)

Overview: Udemy is a global learning platform that connects individuals and organizations with a wide range of online courses, from coding and cloud certifications to leadership and communication, with a strong focus on corporate training and professional upskilling.

Market Cap: US$677.3m

Udemy sits in the middle of the AI skills race, offering enterprises and workers courses, certifications, and AI focused learning tools at a time when many employers expect a large share of existing skills to become outdated. Its shift toward subscriptions, AI assisted learning experiences, and partnerships such as cloud native and Microsoft certification programs aligns with companies that want ongoing, measurable workforce development rather than one off training. At the same time, investors may consider the move away from smaller customers, slower revenue growth than the broader market, and reliance on external borrowing, as well as the fact that Udemy has been absorbed into Coursera, which changes how future value may accrue to shareholders.

Udemy’s shift toward subscriptions and corporate upskilling could be masking how much value its AI focus and enterprise push really add. To see how that balance looks in full, review the analysis report for Udemy

Paycor HCM (PYCR)

Overview: Paycor HCM is a US based software company that provides a cloud native human capital management platform, helping small and mid sized businesses handle HR, payroll, hiring, performance, benefits, and workforce scheduling from a single system.

Operations: Paycor HCM generates about US$699.7m in revenue from Internet Software & Services, all from customers in the United States.

Market Cap: US$4.1b

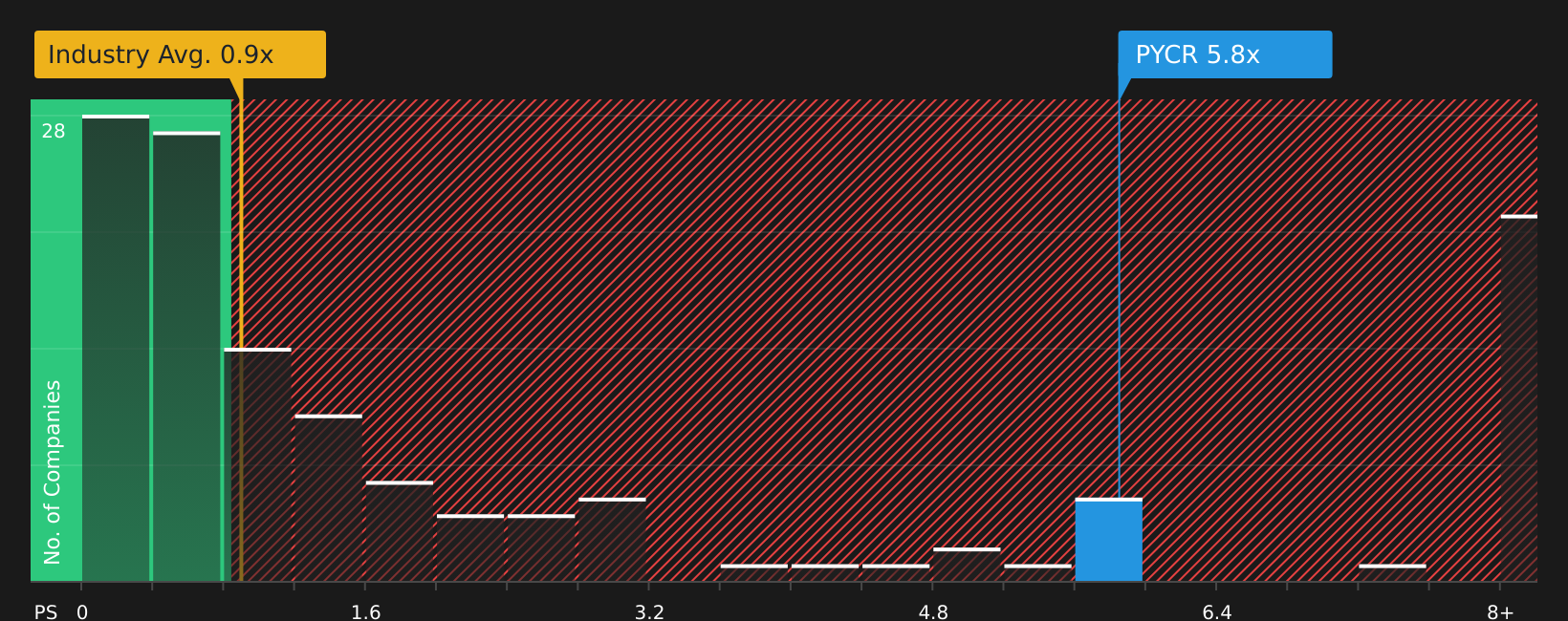

Paycor HCM sits squarely in the sweet spot of the AI driven skills shift, since its platform is built to help small and mid sized employers manage payroll, hiring, performance and employee development as roles become more complex. The company has reduced losses over the past five years and revenue growth is expected to outpace the wider US market, yet it is still unprofitable, relies entirely on higher risk external funding sources, and trades on a P/S that is well above industry averages while also being flagged as well below one estimated fair value. For investors, the real question is how that mix of high expectations, funding risk, and strong HCM positioning lines up with the productivity gains AI is driving across the workforce.

Paycor HCM’s high expectations and rich P/S ratio may be masking a sharper growth story than the headline valuation suggests. See how the analyst forecasts for Paycor HCM reshapes the risk reward trade off before the market fully joins the dots.

The three Human Capital Development & Training Providers in this article are just a starting point. The full Human Capital Development & Training Providers screener reveals 3 more companies whose workforce development and upskilling stories could be just as compelling. Use Simply Wall St to identify, filter, and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction opportunities in this theme.

Take Control of Your Investment Journey

If Paycor HCM or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies?

Fresh stock ideas rarely stay under the radar for long. As momentum builds and ideal entry points risk getting caught by the crowd, consider moving earlier while it may matter and acting with a clear plan.

- Spot emerging trends by reviewing the curated 45 high quality undervalued stocks, built to highlight companies where cash flows and balance sheets may not align with current market sentiment.

- Explore potential income opportunities with the hand picked 8 dividend fortresses that focuses on higher yield candidates backed by businesses aiming to sustain payouts.

- Follow the AI infrastructure theme by scanning the focused 49 AI infrastructure stocks and reviewing which companies could be positioned to participate if demand for compute and data capacity changes over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.