InterDigital (IDCC) Stock Could Be 36% Undervalued After Amazon License Agreement

InterDigital, Inc. IDCC | 0.00 |

Why InterDigital’s New Amazon Agreement Matters for Shareholders

InterDigital (IDCC) has drawn fresh investor attention after announcing a patent license agreement with Amazon that covers key services and devices, alongside plans to resolve all pending litigation through binding arbitration.

This development sits alongside a recently declared regular quarterly dividend and shareholder approval of bylaw changes related to officer exculpation. Together, these provide investors with several governance, income, and licensing factors to weigh when assessing the stock.

InterDigital’s recent Amazon agreement and bylaw update come against a mixed backdrop, with a 13.43% 1 month share price return and the share price still down 9.26% year to date. At the same time, the 5 year total shareholder return of 330.09% highlights substantial longer term gains.

If this kind of licensing news has you thinking about where else growth stories could emerge, it may be worth scanning the market using the 49 AI infrastructure stocks

With InterDigital’s share price up 13.43% over the past month but still down 9.26% year to date, and trading well below the average analyst price target, investors have to ask: is there real value left here or is the market already pricing in future growth?

Most Popular Narrative: 36% Undervalued

InterDigital’s most followed narrative pegs fair value at $462.67 per share versus a last close of $296.04. This frames the current price as a sizable discount built on detailed cash flow and earnings assumptions.

The recent 67% uplift in the Samsung license and an all-time high annualized recurring revenue, driven by multi-year agreements with major OEMs, have set highly optimistic expectations for continued outsized growth in future contract renewals, potentially inflating valuation multiples and overstating sustainable revenue trajectory.

Curious what justifies that valuation gap for InterDigital? The narrative leans heavily on recurring licensing income, margin resilience and a richer future earnings multiple than many software peers.

Result: Fair Value of $462.67 (UNDERVALUED)

However, investors still have to weigh the risk that InterDigital’s heavy reliance on smartphone royalties and ongoing regulatory scrutiny of patent licensing could weaken those long term cash flow assumptions.

Another View: InterDigital Through a Cash Flow Lens

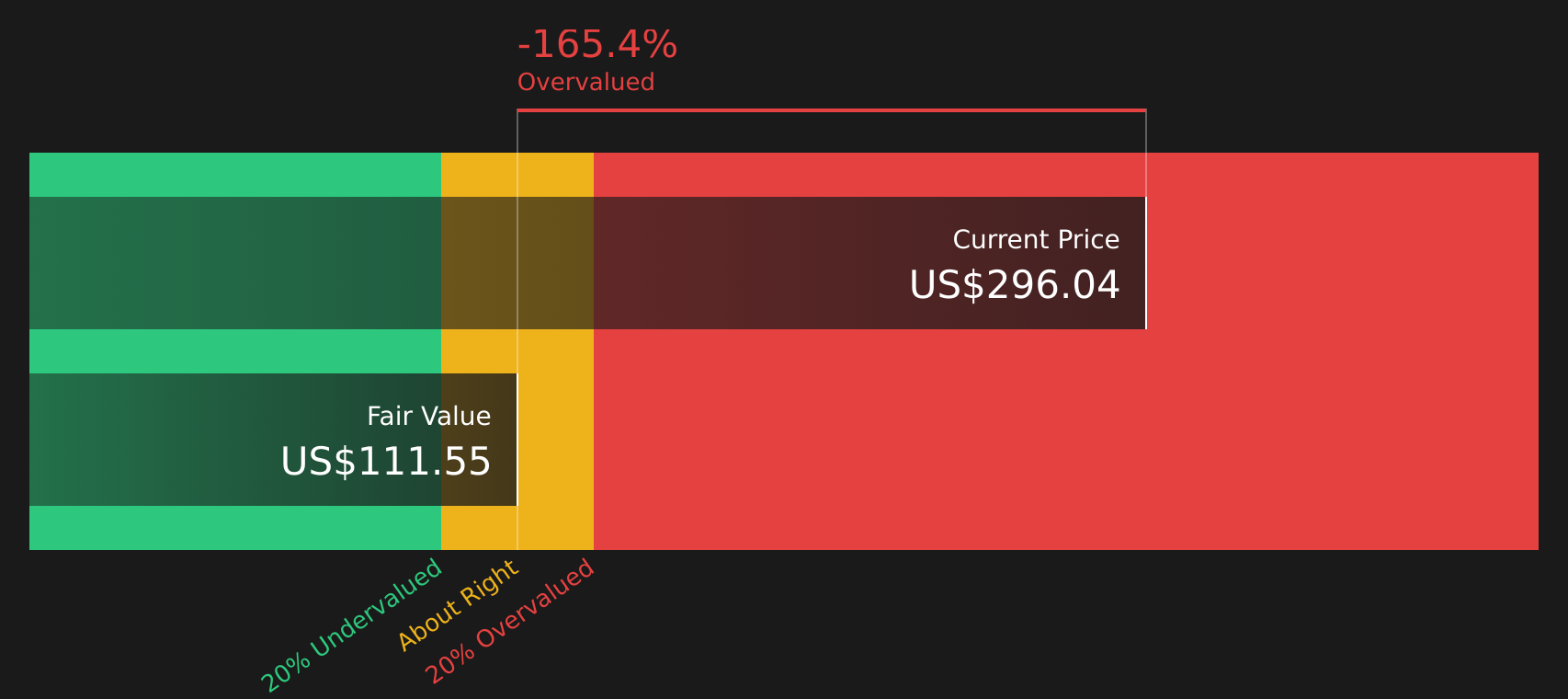

While the analyst narrative suggests InterDigital is 36% undervalued with a fair value of $462.67 per share, the Simply Wall St DCF model points the other way, with an estimate of $111.55 per share versus today’s $296.04 price. This implies the stock screens as overvalued on that basis. Which lens do you trust more for your own thesis?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of optimism and caution around InterDigital leaves you undecided, act while the data is fresh and form your own view by reviewing the 3 key rewards

Looking For More Investment Ideas Beyond InterDigital?

If InterDigital has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to surface other opportunities that fit your style.

- Target resilient cash generators by scanning companies in the 45 high quality undervalued stocks and see where market expectations look out of line with fundamentals.

- Prioritize stability by reviewing the 65 resilient stocks with low risk scores to find stocks that pair lower risk scores with more predictable business profiles.

- Hunt for tomorrow’s potential standouts with the screener containing 19 high quality undiscovered gems and spot quality ideas before they are widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.