Is 10x Genomics (TXG) Price Reflecting Its Mixed Valuation Signals After Strong 1-Year Run

10x Genomics TXG | 0.00 |

- Wondering whether 10x Genomics is genuinely good value or just riding hype? This article explores what the current share price might be indicating.

- The stock last closed at US$21.42, with returns of 28.9% year to date and 157.8% over the past year. The 3 year and 5 year returns are 58.3% and 89.1% in the red, respectively.

- Short term price moves have been mixed, with a 15.1% decline over the past 7 days but an 8.1% gain across the last 30 days. This pattern can often reflect shifting sentiment as investors reassess long term prospects and risk.

- The Simply Wall St valuation model currently gives 10x Genomics a valuation score of 3 out of 6. Next up is a closer look at how different valuation methods compare for this stock and why a broader framework later in the article could be even more useful to you.

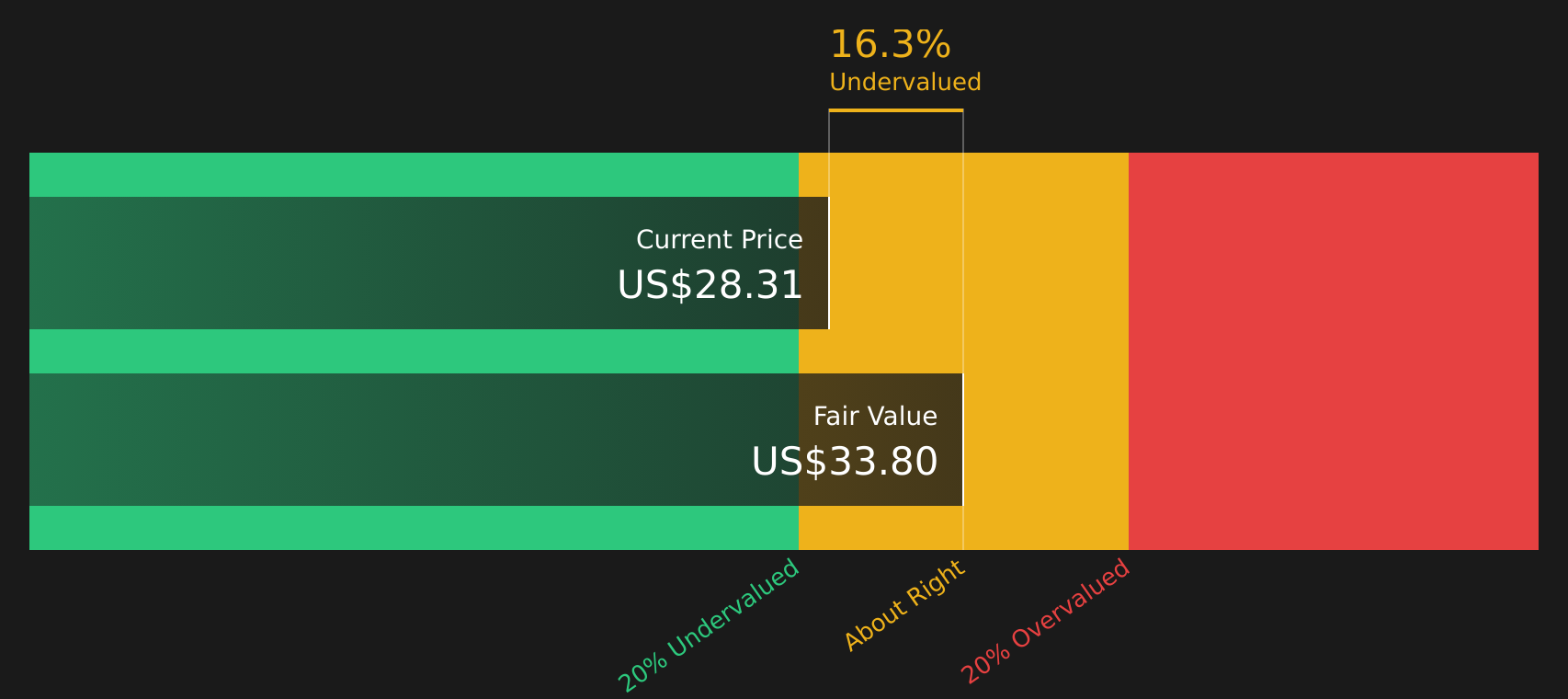

Approach 1: 10x Genomics Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth by projecting its future cash flows and then discounting them back to today’s value using a required rate of return.

For 10x Genomics, the model in use is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is reported at $112.4 million. Analysts provide specific free cash flow estimates for the next few years, and Simply Wall St then extends these projections further. In this case, the ten year projections range from a free cash flow loss of $36 million in 2026 through to a positive $315.2 million in 2035, with $66 million projected for 2029. All these future values are discounted back to today in dollar terms.

Aggregating those discounted cash flows produces an estimated intrinsic value of about $32.55 per share. Compared with the recent share price of $21.42, the DCF output suggests the stock trades at a 34.2% discount to this intrinsic estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests 10x Genomics is undervalued by 34.2%. Track this in your watchlist or portfolio, or discover 54 more high quality undervalued stocks.

Approach 2: 10x Genomics Price vs Sales

For companies where earnings are not the main focus or are still developing, the P/S ratio is often more useful because it compares what investors are paying to the revenue the business is already generating.

What counts as a reasonable P/S ratio usually reflects how fast revenue is expected to grow and how risky those future sales are. Higher growth and lower perceived risk tend to justify a higher P/S multiple, while slower growth or higher uncertainty usually point to a lower multiple.

10x Genomics currently trades on a P/S of 4.26x, compared with the Life Sciences industry average of 3.20x and a peer average of 9.24x. Simply Wall St’s Fair Ratio for 10x Genomics is 3.80x, which is a proprietary estimate of what the P/S might be given factors such as growth outlook, profit margins, risk profile, market value and industry characteristics.

Because the Fair Ratio adjusts for these company specific factors, it can be more informative than relying only on broad industry or peer comparisons. With the current P/S of 4.26x sitting above the Fair Ratio of 3.80x, the shares screen as overvalued on this measure.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 17 top founder-led companies.

Upgrade Your Decision Making: Choose your 10x Genomics Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as your chance to attach a clear story to the numbers by linking your view of 10x Genomics' future revenue, earnings and margins to a fair value and then comparing that to the current price.

On Simply Wall St's Community page, Narratives are an accessible tool used by millions of investors, allowing you to set out your own assumptions, see how they translate into a financial forecast, and then quickly check whether your fair value suggests the stock looks expensive or cheap relative to where it trades today.

Because Narratives update automatically when fresh information arrives, such as new product announcements or earnings releases, your fair value view stays aligned with the latest data instead of being frozen at the moment you first ran the numbers.

For 10x Genomics, for example, one investor might align with a bullish Narrative that arrives at a fair value of US$32.00 using assumptions like revenue of US$749.8 million, earnings of US$115.9 million and a P/E of 49.4x by 2029. Another investor might lean toward a more cautious Narrative closer to US$17.00 or US$20.14 based on lower revenue and earnings assumptions and a lower future P/E. The gap between those views highlights how your own story about the company can drive your decision making.

For 10x Genomics, however, we will make it really easy for you with previews of two leading 10x Genomics Narratives:

Fair value: US$32.00 per share

Implied upside vs last close: about 33% below this fair value

Assumed revenue growth: 5.3% a year

- Expects faster take up of spatial and consumables products to support higher revenue and better mix over time.

- Sees biopharma customers, global research programs and new AI driven applications as key sources of more diversified, recurring income.

- Assumes profit margins eventually line up with the wider US Life Sciences industry and support a P/E of 49.4x on 2029 earnings to justify a US$32.00 price.

Fair value: US$20.14 per share

Implied downside vs last close: about 6% above this fair value

Assumed revenue growth: 3.4% a year

- Highlights that new products and acquisitions broaden the toolkit but also bring pricing and product mix questions at the same time as the company is still loss making.

- Points to pressures on research budgets, lower average selling prices and instrument discounting as risks for revenue growth and margins.

- Builds to a fair value of US$20.14 on the view that earnings could reach US$110.2 million by 2029, with the shares trading on a P/E of 32.7x at that point.

If you want to go further than these previews and test which story best matches your own expectations for growth, margins and risk, the full set of Narratives on Simply Wall St lets you plug in your assumptions and see how your fair value stacks up against the current market price.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for 10x Genomics on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for 10x Genomics? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.