Is AdaptHealth (AHCO) Pricing Reflect A Potential Turn After Prolonged Share Price Weakness

ADAPTHEALTH CORP AHCO | 12.03 | +1.43% |

- If you are wondering whether AdaptHealth's share price lines up with its underlying worth, you are not alone. This article focuses squarely on what the current price might be implying about value.

- The stock last closed at US$10.61, with returns of 1.1% over 7 days, 1.2% over 30 days, 9.7% year to date and 0.9% over 1 year. These figures are set against much weaker 3 year and 5 year returns of 49.5% and 72.1% declines.

- Recent coverage has focused on AdaptHealth's position in the home healthcare equipment space and how the business model fits into long term demand for at home care. This helps frame how investors interpret these mixed return figures. This context matters if you are trying to decide whether the recent stabilisation in shorter term returns is a turning point or just another pause in a longer weak stretch.

- Our valuation model currently gives AdaptHealth a value score of 5/6. Next we will walk through the main valuation approaches that feed into that score, before finishing with a more holistic way to think about what the market might be missing.

Approach 1: AdaptHealth Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company’s future cash flows, then discounts them back to today to see what those future streams might be worth in present terms.

For AdaptHealth, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $209.4 million, and Simply Wall St projects free cash flow of $194.68 million in 2026. Beyond the near term, cash flows out to 2035 are extrapolated, with each year’s figure discounted back to today using the model’s assumptions.

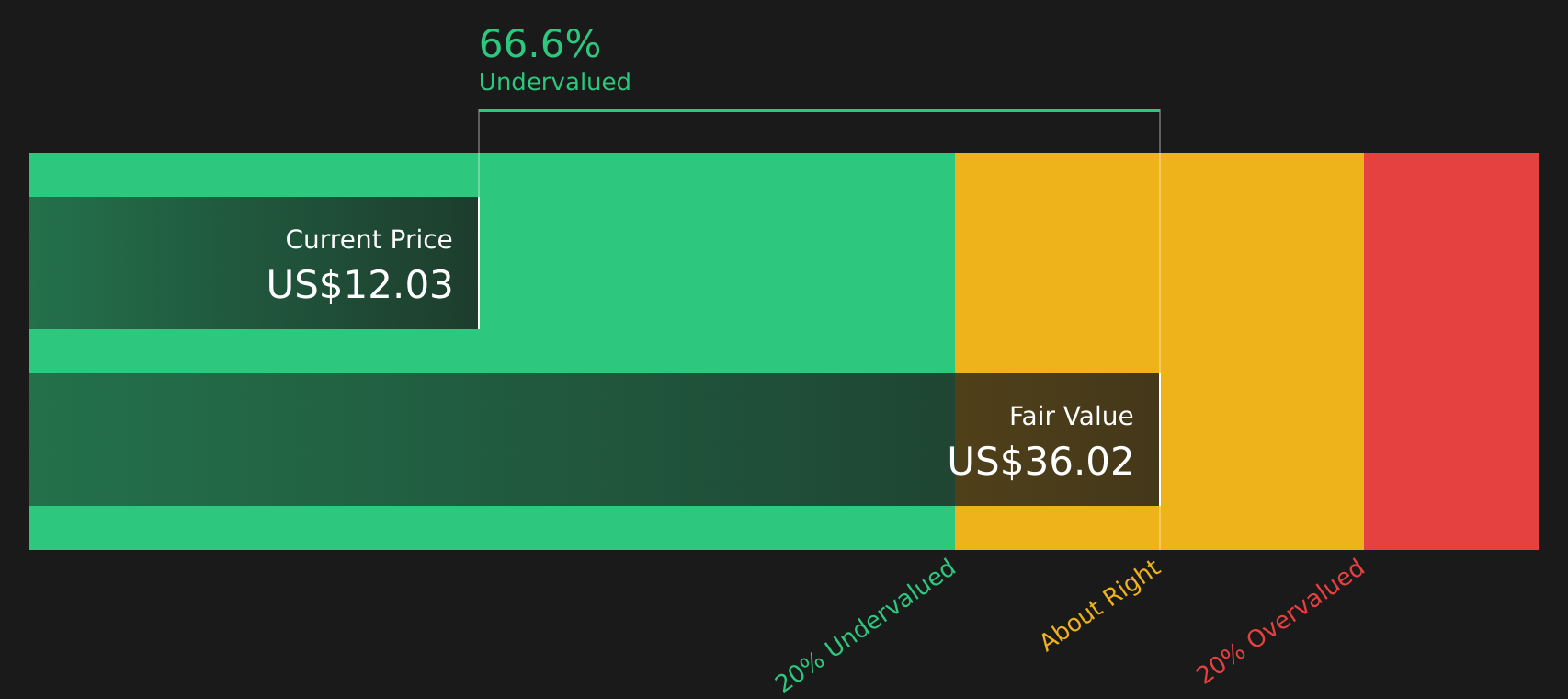

Putting these cash flows together produces an estimated intrinsic value of about $26.87 per share. Compared with the recent share price of $10.61, the model implies a discount of roughly 60.5%, which indicates that the stock is trading materially below this estimate of fair value.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AdaptHealth is undervalued by 60.5%. Track this in your watchlist or portfolio, or discover 863 more undervalued stocks based on cash flows.

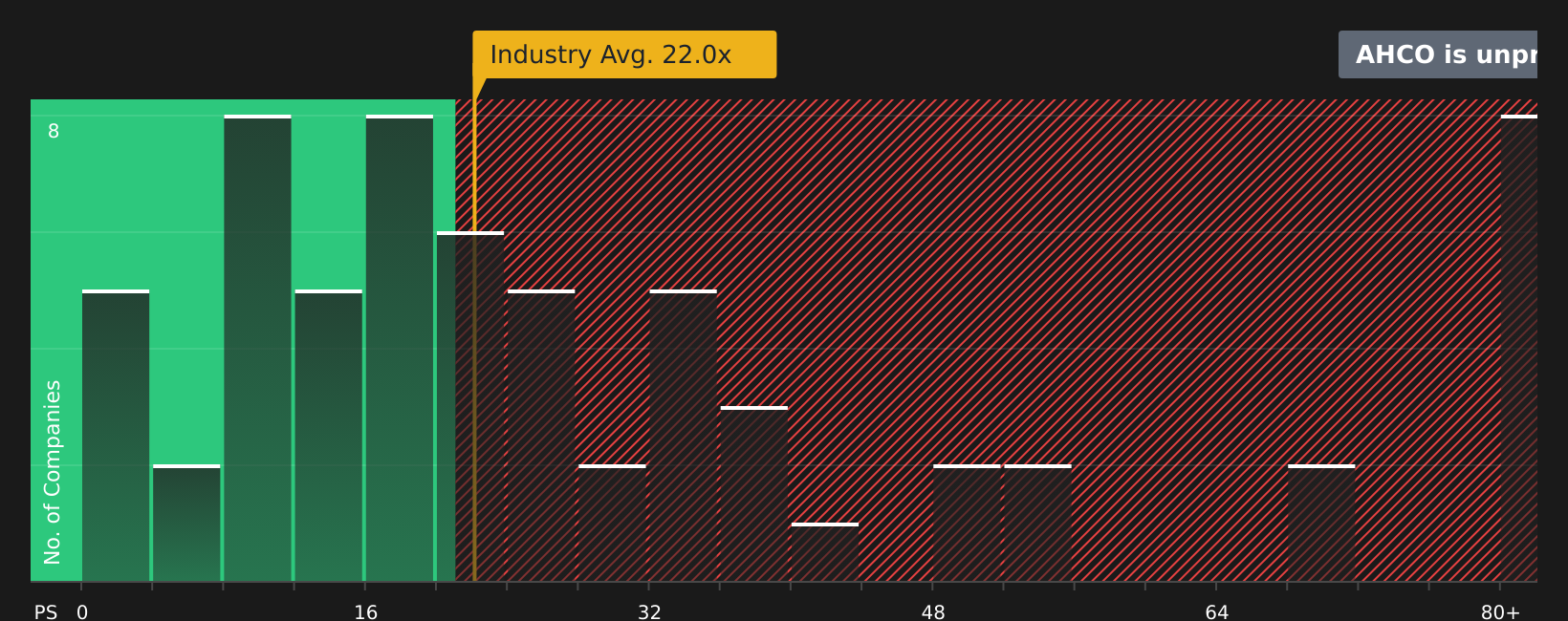

Approach 2: AdaptHealth Price vs Earnings

The P/E ratio is a useful cross check for companies that are generating profits, because it links what you pay for each share to the earnings that the business is already producing.

In general, higher growth expectations and lower perceived risk can justify a higher P/E, while slower expected growth or higher risk tend to pull a “normal” or “fair” P/E lower. That is why it helps to compare a company’s P/E with relevant benchmarks rather than in isolation.

AdaptHealth currently trades on a P/E of 18.67x. That sits below the Healthcare industry average of 23.44x and also below the peer group average of 26.98x. Simply Wall St’s Fair Ratio for AdaptHealth is 26.62x, which is a proprietary estimate of what the P/E could be given factors such as earnings growth profile, industry, profit margins, market capitalization and company specific risks.

Because the Fair Ratio is tailored to AdaptHealth’s own characteristics rather than just broad sector numbers, it can be more informative than a simple industry or peer comparison. With the current P/E of 18.67x sitting meaningfully under the Fair Ratio of 26.62x, this approach suggests the shares are trading below that implied fair multiple.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AdaptHealth Narrative

Earlier we mentioned that there is an even better way to think about valuation, and on Simply Wall St that comes through Narratives, where you set out your story for AdaptHealth, plug in your own assumptions for future revenue, earnings, margins and fair value, then see that story live on the Community page, update automatically when fresh news or earnings arrive, and help you compare your fair value against the current price so you can decide if it feels more like a buy, hold or sell moment. For example, one AdaptHealth Narrative might lean on the five year, US$1b plus capitated contract, digital automation projects and analyst expectations that earnings reach about US$157.7m by 2028 and support a fair value near US$16.00. A more cautious Narrative might focus on reimbursement and execution risks and land closer to US$10.50. Both can sit side by side so you can see how different assumptions lead to different fair values.

Do you think there's more to the story for AdaptHealth? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.