Is Align Technology (ALGN) Now Offering Value After Recent Share Price Rebound

Align Technology, Inc. ALGN | 0.00 |

- Wondering whether Align Technology at US$173.25 is starting to look like value, or if the stock still carries more hype than fundamentals.

- The share price is up 6.3% over the last 7 days and 11.0% year to date, but is still down 2.3% over 30 days and has declined 5.4% over 1 year, 41.7% over 3 years and 69.4% over 5 years.

- These swings have kept Align on many investors' watchlists, as the company continues to be a reference point in clear aligner dentistry and digital orthodontics. Recent coverage has focused on how investors are reassessing the stock after a long period of weaker returns, with attention shifting back to what a fair price might look like.

- On Simply Wall St's valuation model, Align scores 4 out of 6 on the undervaluation checks. This sets up a closer look at methods like DCFs, multiples, and peer comparisons, followed by a more holistic way to think about what this valuation really means for you.

Approach 1: Align Technology Discounted Cash Flow (DCF) Analysis

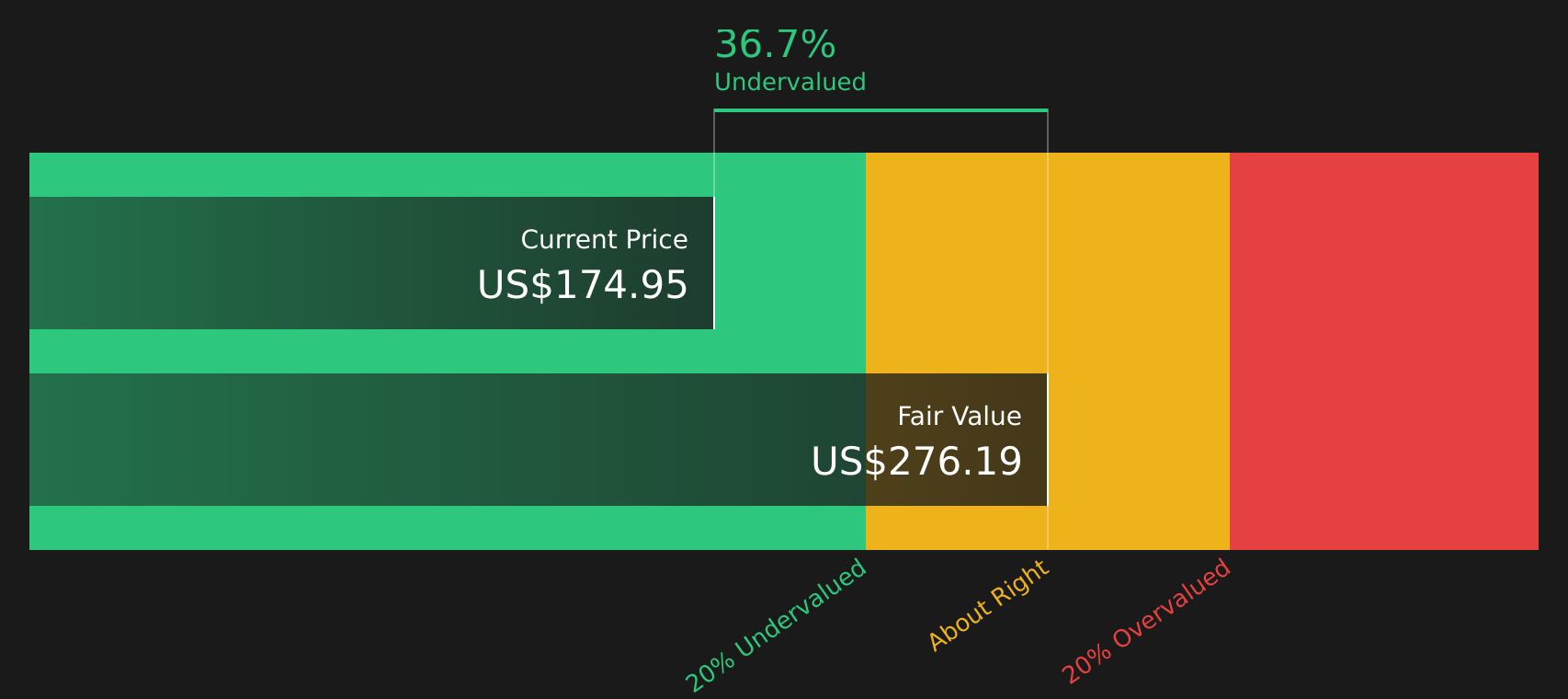

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts them back to today using a required rate of return. The goal is to estimate what those cash flows are worth in $ right now, then compare that figure with the current share price.

For Align Technology, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow sits at about $567.8 million. Analyst and extrapolated projections suggest free cash flow reaches about $931.9 million by 2030, with intermediate yearly figures between roughly $627.9 million and $1,087.5 million over the next decade, all in $ terms.

After discounting those projected cash flows back to today, Simply Wall St’s model arrives at an estimated intrinsic value of about $277.14 per share. Compared with the recent share price of $173.25, this implies the stock trades at roughly a 37.5% discount, which indicates potential undervaluation within this DCF framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Align Technology is undervalued by 37.5%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Align Technology Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand for what investors are currently willing to pay for each dollar of earnings. It reflects both what the business is earning today and how investors feel about its prospects and risks.

In general, higher expected growth and lower perceived risk can support a higher P/E that investors may see as "normal" or "fair," while slower growth or higher risk often line up with a lower P/E. Align Technology currently trades on a P/E of 28.9x. That sits above the Medical Equipment industry average of 24.3x and above the peer average of 22.3x, suggesting the stock is priced at a premium to many sector peers.

Simply Wall St’s Fair Ratio for Align is 29.7x. This is a proprietary estimate of what P/E might be reasonable given factors such as earnings growth, industry, profit margins, market cap and company specific risks. Because it incorporates those company level drivers rather than relying only on peer or industry averages, it can give a more tailored reference point for valuation. With the current P/E of 28.9x sitting slightly below the Fair Ratio of 29.7x, the stock screens as modestly undervalued on this measure.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Align Technology Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in, giving you a simple way to tell a story about Align Technology that connects your view of its business to a forecast and then to a fair value.

On Simply Wall St, a Narrative is your own explanation for the numbers you are using, such as how you think Align’s revenue, earnings and margins may develop, and what P/E or discount rate feels reasonable based on that story.

Each Narrative links that story to a full financial forecast, then to a Fair Value estimate that you can compare directly with the current share price to help you decide whether you see the stock as expensive or cheap against your assumptions.

These Narratives sit inside the Community section of Simply Wall St, where millions of investors share and review different views, and each one updates automatically when new information like earnings, guidance or major news is added to the platform.

For Align Technology, one investor might align with a more cautious view that points to a Fair Value of about US$175 per share, while another may side with a more optimistic view closer to US$240, and seeing those side by side makes it easier for you to choose which story feels closer to your own.

For Align Technology, however, we will make it really easy for you with previews of two leading Align Technology Narratives:

Each Narrative ties together growth assumptions, margins, risks and a fair value estimate, so you can quickly see which story feels closer to how you view the stock today.

Fair Value: US$201.69

Current price vs this Fair Value: trading at about 13.9% below this estimate, so it screens as cheaper than this Narrative suggests.

Revenue growth used in this Narrative: 4.94% a year.

- Analysts in this view see Align expanding into more clinical segments and geographies, with investments in digital workflow and automation supporting higher margins over time.

- The Narrative assumes revenue of about US$4.7b and earnings of US$726.5m by 2029, with a future P/E of 23.6x and a discount rate of 7.77% feeding into the Fair Value of US$201.69.

- Key risks flagged include pressure on orthodontic case starts, a shift toward lower priced products and regions, softer scanner demand, and tougher competition that could weigh on volumes and margins.

Fair Value: US$154.62

Current price vs this Fair Value: trading at about 12.1% above this estimate, so it screens as more expensive than this Narrative suggests.

Revenue growth used in this Narrative: 4.80% a year.

- This view focuses on Align as a premium orthodontics provider in a cost sensitive world, where pricing power is tested by inflation, tighter discretionary spending and more competition.

- The Narrative highlights that Invisalign, iTero scanners and AI driven planning still anchor clinical trust, but the bar for returns on technology and global expansion is higher as markets become more value conscious.

- Here, the fair value of US$154.62 reflects concerns that maintaining margins, brand strength and clinical credibility may require ongoing investment, with less room for valuation to stretch without clear evidence on durability of demand.

If you want to see these stories with the full numbers, forecasts and supporting charts, jump into the community views for Align, compare the Narratives side by side and decide which assumptions feel closest to your own.

Do you think there's more to the story for Align Technology? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.