Is Alkermes (ALKS) Fully Priced As Russell 2000 Index Inclusion Draws Fresh Attention?

Alkermes Public Limited Company ALKS | 0.00 |

What Alkermes’ Russell 2000 Dynamic Index Addition Signals for Investors

Alkermes (NasdaqGS:ALKS) was added to the Russell 2000 Dynamic Index on June 27, 2026, an inclusion that often brings the stock onto the radar of index funds, institutional investors, and rules based strategies.

For existing and prospective shareholders, index additions such as this can matter less for immediate price reaction and more for how they influence liquidity, trading volumes, and the breadth of the investor base over time.

The index inclusion comes after a strong run in Alkermes’ share price, with a 30 day share price return of 27.89% and year to date share price return of 92.11%. The 5 year total shareholder return of 130.28% points to meaningfully positive long term compounding.

If Alkermes’ momentum has caught your attention, it may be a good moment to see what else is moving in health focused AI, starting with the 40 healthcare AI stocks.

Bulls see Alkermes’ recent index inclusion and strong shareholder returns as proof the valuation can stretch further, while bears point to rich expectations already in the price. So what do the current earnings and cash flows actually imply?

Most Popular Narrative: 14% Overvalued

At a last close of $54.29 versus the narrative fair value of $47.69, Alkermes is framed as pricing in a premium that hinges on its sleep disorder and orexin pipeline story.

Analysts are assuming Alkermes's revenue will grow by 11.1% annually over the next 3 years. Analysts assume that profit margins will increase from 9.8% today to 12.4% in 3 years time.

Curious what justifies paying up for Alkermes today? The core narrative leans on faster earnings growth, fatter margins, and a richer future earnings multiple. Want to see how those moving parts connect to that $47.69 fair value and beyond?

Result: Fair Value of $47.69 (OVERVALUED)

However, there are still clear swing factors for Alkermes, including heavier R&D spend on orexin programs and the company’s reliance on a concentrated product portfolio.

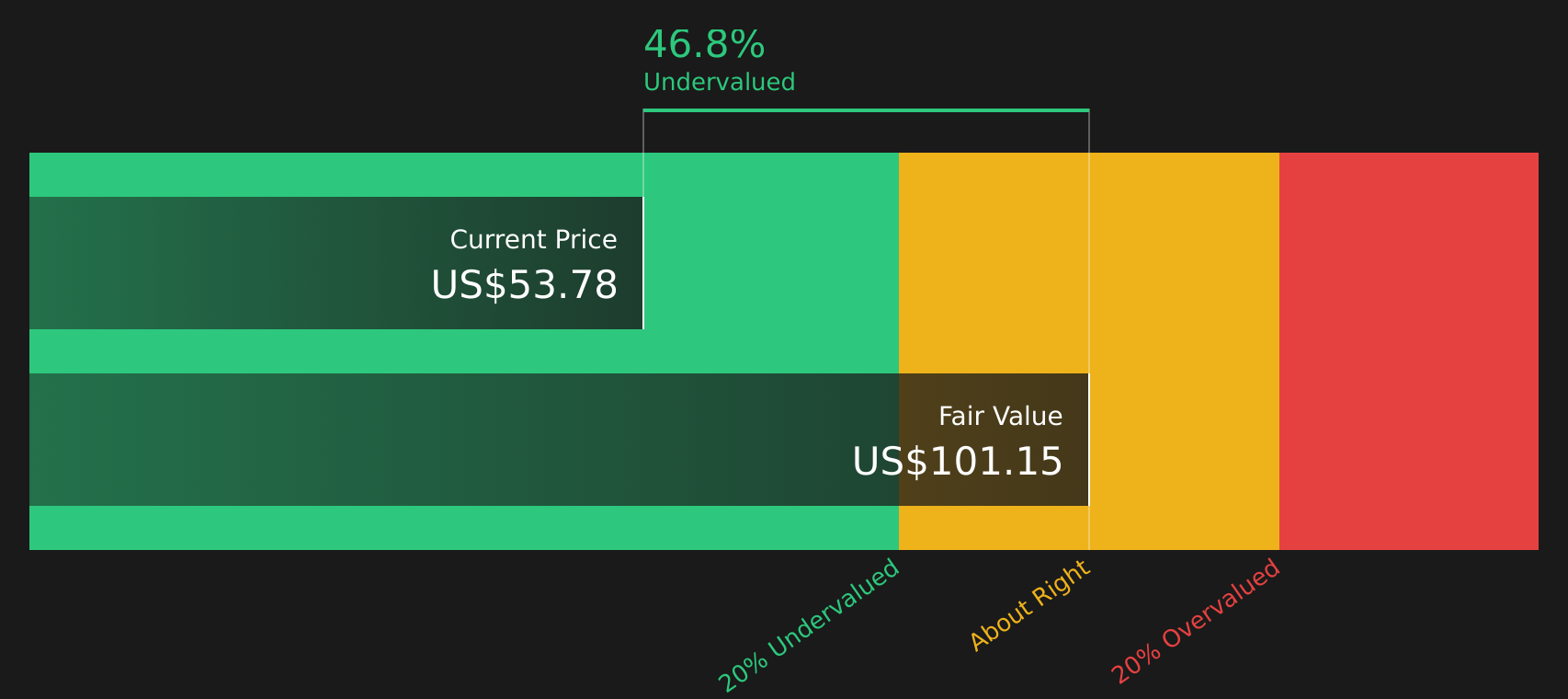

Another View: Alkermes Through a Cash Flow Lens

The earlier narrative framed Alkermes as 14% overvalued at $54.29 versus a $47.69 fair value built from analyst earnings and multiples. Our DCF model presents a different perspective, with Alkermes trading below an estimated future cash flow value of $101.48. This raises a simple question: which set of assumptions do you trust more for your own work?

To understand how those cash flow assumptions compare with both the narrative fair value and the current share price, take a closer look at the SWS DCF model, starting with the Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alkermes for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Alkermes leave you on the fence, now is a good time to weigh the data and form your own stance. A helpful way to frame that view is by comparing the 2 key rewards and 2 important warning signs.

Looking for more Alkermes style investment ideas?

Do not stop at Alkermes alone. Use Simply Wall Street's tools to scan the market now so you are not the one hearing about the ideas after everyone else.

- Target stronger upside potential by focusing on quality companies trading below their estimated value with the help of the 44 high quality undervalued stocks.

- Prioritize steadier returns by zeroing in on businesses with robust cash flows that support higher payouts using the 9 dividend fortresses.

- Guard your portfolio against shocks by concentrating on companies with healthier balance sheets and lower overall risk using the 72 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.