Is Analyst Upgrade And Workplace Accolade Altering The Investment Case For W.W. Grainger (GWW)?

W.W. Grainger, Inc. GWW | 0.00 |

- In recent days, W.W. Grainger was upgraded to a Zacks Rank #2 and recognized by Newsweek as a 5-star winner in America’s Greatest Workplaces 2026, reflecting improving analyst earnings estimates and strong employee satisfaction.

- Together, the enhanced earnings outlook and workplace accolade highlight how financial expectations and culture are working in tandem to reinforce confidence in Grainger’s business model.

- Now we’ll examine how this analyst upgrade, underpinned by rising earnings estimates, may reshape W.W. Grainger’s existing investment narrative.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

W.W. Grainger Investment Narrative Recap

To own W.W. Grainger, you need to believe its scale, service, and digital capabilities can keep it a preferred MRO partner despite pricing, tariff, and demand headwinds. The Zacks Rank upgrade and Newsweek workplace recognition support confidence in execution, but they do not materially change near term risks around margin pressure from tariffs, supply chain complexity, or a muted MRO backdrop.

The most relevant update here is Grainger’s recent guidance raise, with 2026 net sales now expected at US$19.2 billion to US$19.6 billion and diluted EPS at US$44.25 to US$46.25. This firmer outlook is consistent with rising analyst earnings estimates that underpinned the Zacks Rank change, and it reinforces how the current catalyst is about Grainger delivering on higher profit expectations while managing cost inflation and capital spending.

Yet investors also need to consider how rising digital disintermediation could challenge Grainger’s traditional model and margin resilience if customers increasingly bypass distributors and...

W.W. Grainger's narrative projects $22.5 billion revenue and $2.5 billion earnings by 2029. This requires 6.9% yearly revenue growth and a roughly $0.7 billion earnings increase from $1.8 billion today.

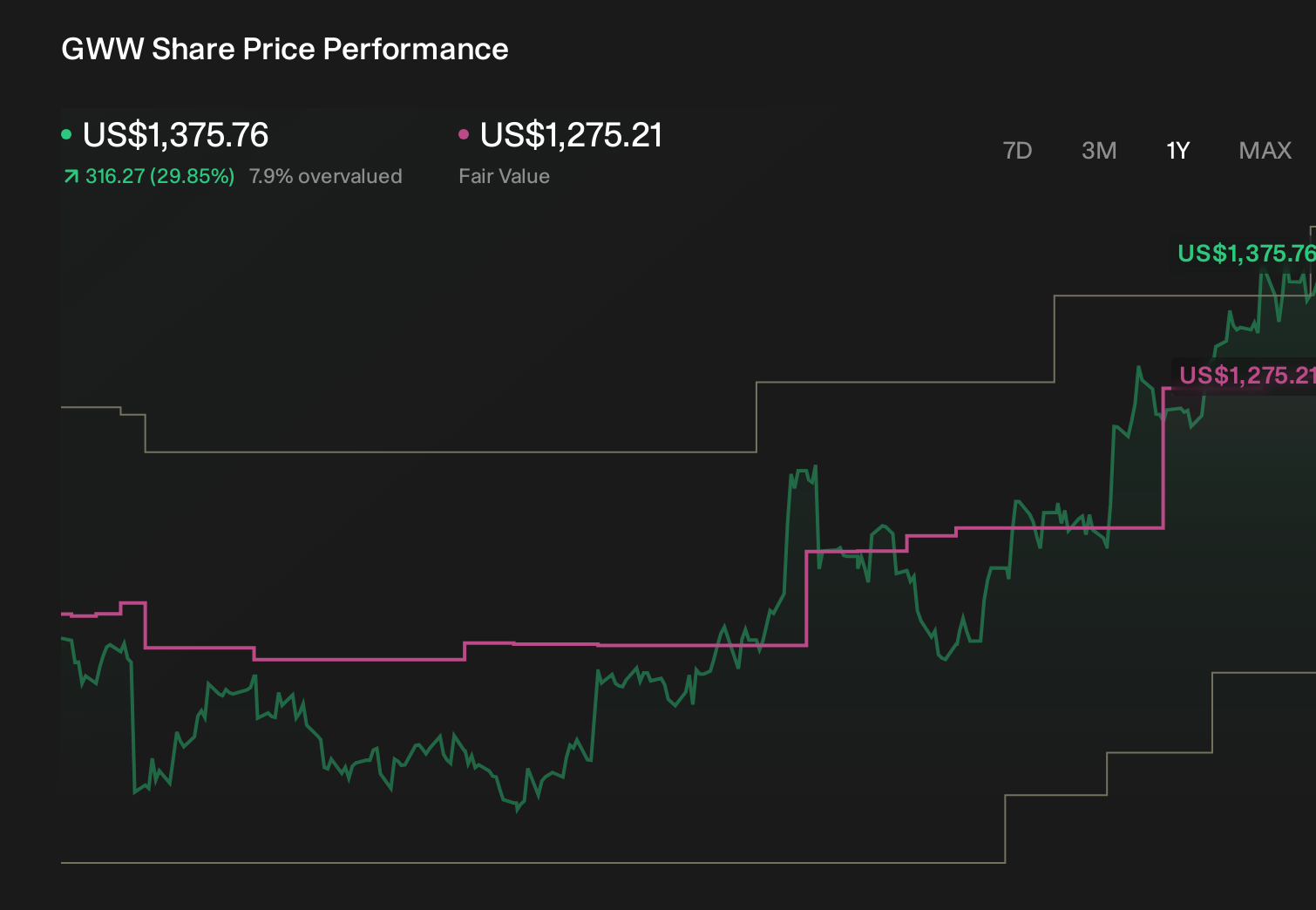

Uncover how W.W. Grainger's forecasts yield a $1266 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Some analysts are far more optimistic, expecting revenue of about US$22.5 billion and earnings of US$2.6 billion by 2029, but the latest upgrades and workplace accolades may prompt you to compare that bullish view with fresh digital disruption risks and see how your own assumptions stack up.

Explore 3 other fair value estimates on W.W. Grainger - why the stock might be worth 15% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your W.W. Grainger research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free W.W. Grainger research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W.W. Grainger's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.