Is Arteris (AIP) Quietly Becoming a Core Infrastructure Player in Automotive SoC Design?

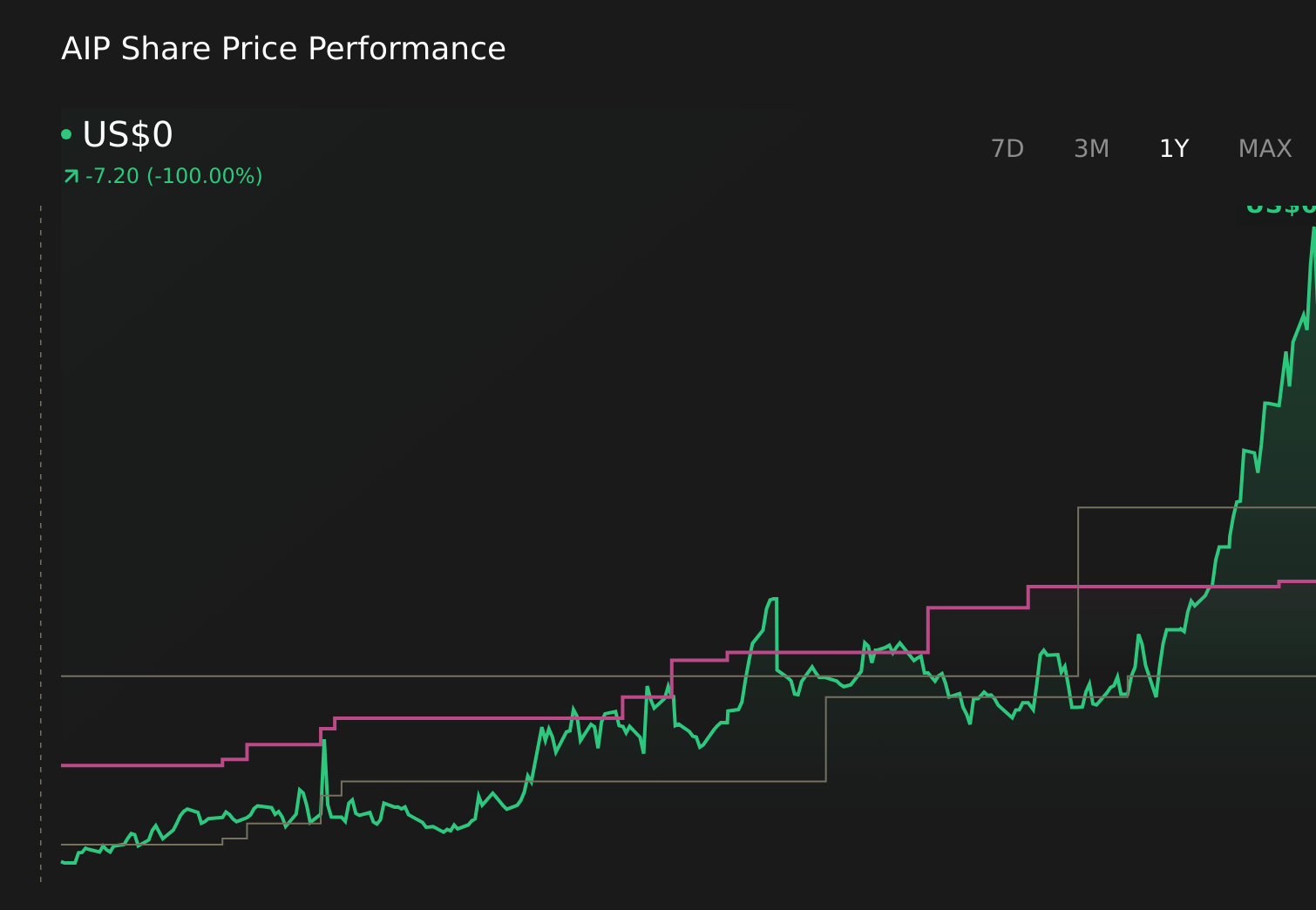

Arteris, Inc. AIP | 0.00 |

- In June 2026, Arteris, Inc. announced that SiEngine Technology licensed its FlexNoC 5 network-on-chip interconnect IP for next-generation automotive SoC platforms focused on intelligent cockpits, advanced driver assistance, and AI cockpit-drive fusion, aiming to meet stringent functional safety requirements.

- This renewed adoption across several generations of SiEngine automotive chips underscores how Arteris’ silicon-proven FlexNoC IP has become a communication backbone candidate for complex, safety-critical vehicle electronics.

- We’ll now examine how SiEngine’s expanded use of FlexNoC as an on-chip backbone could influence Arteris’ investment narrative in automotive.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Arteris Investment Narrative Recap

To own Arteris, you need to believe that outsourced network on chip IP can become a core enabler of increasingly complex AI centric automotive and compute designs, and that this will eventually support a path toward lower losses. The new SiEngine win reinforces Arteris’ relevance in safety critical automotive, but it does not, on its own, remove the near term risks around persistent net losses and dependence on large, concentrated customer relationships.

Among recent announcements, the February 2026 expansion with NXP across AI enabled MCUs, NPUs, and SoCs looks especially relevant. Together with the SiEngine deal, it shows Arteris’ NoC and integration tools being adopted across multiple major automotive silicon roadmaps, which ties directly into the key catalyst of growing AI and ADAS complexity, even as spending on R&D and field engineering continues to weigh on profitability.

Yet investors should also weigh how customer concentration risk could affect Arteris if even one large partner shifts direction...

Arteris' narrative projects $151.4 million revenue and $18.3 million earnings by 2029. This requires 25.3% yearly revenue growth and a $52.9 million earnings increase from -$34.6 million today.

Uncover how Arteris' forecasts yield a $37.75 fair value, a 20% downside to its current price.

Exploring Other Perspectives

Before this SiEngine announcement, the most optimistic analysts were already assuming about 24.5 percent annual revenue growth and a swing to US$15.5 million in earnings by 2029, so it is worth asking whether wins like this validate that upbeat view or if concentration and profitability risks could still pull the story in a very different direction.

Explore 5 other fair value estimates on Arteris - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Arteris research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Arteris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arteris' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 42 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.